General Liability Insurance Coverage: Understanding What Shields Your Business

General liability insurance coverage protects your business from financial losses when someone gets hurt on your property or you accidentally damage their belongings. Without it, a single lawsuit could drain your savings and force you to close your doors.

At Aurora National Insurance, we’ve helped thousands of business owners understand exactly what their policies cover and where the gaps hide. This guide walks you through the protection you actually have and how to pick the right limits for your situation.

What Your General Liability Policy Actually Covers

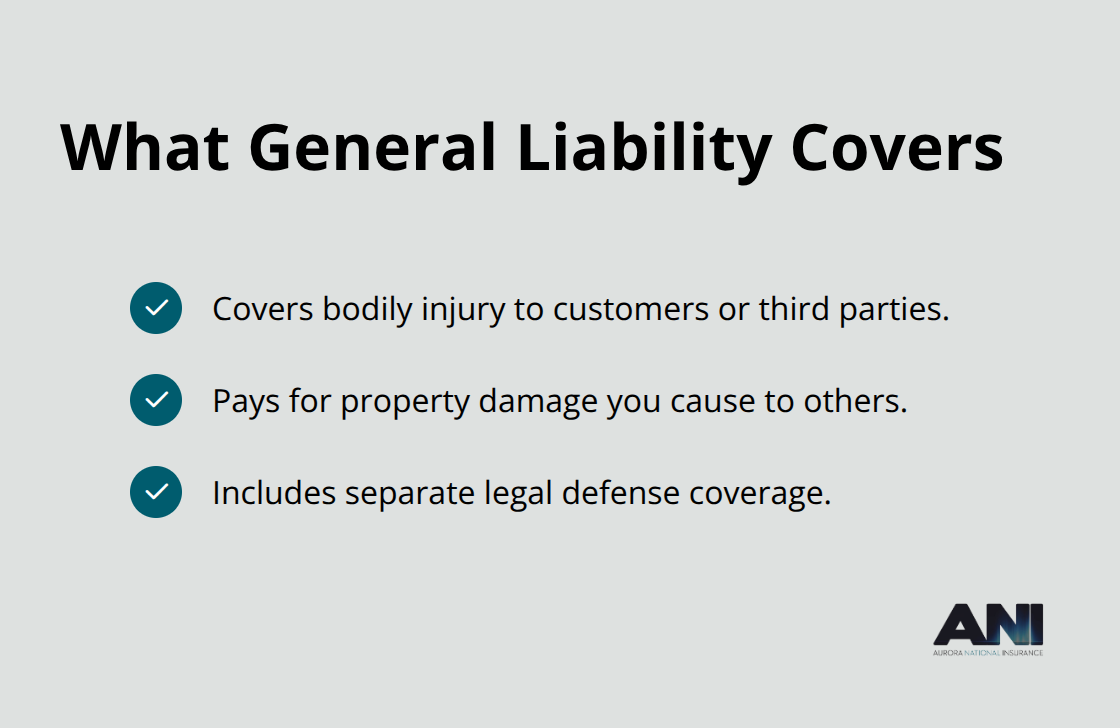

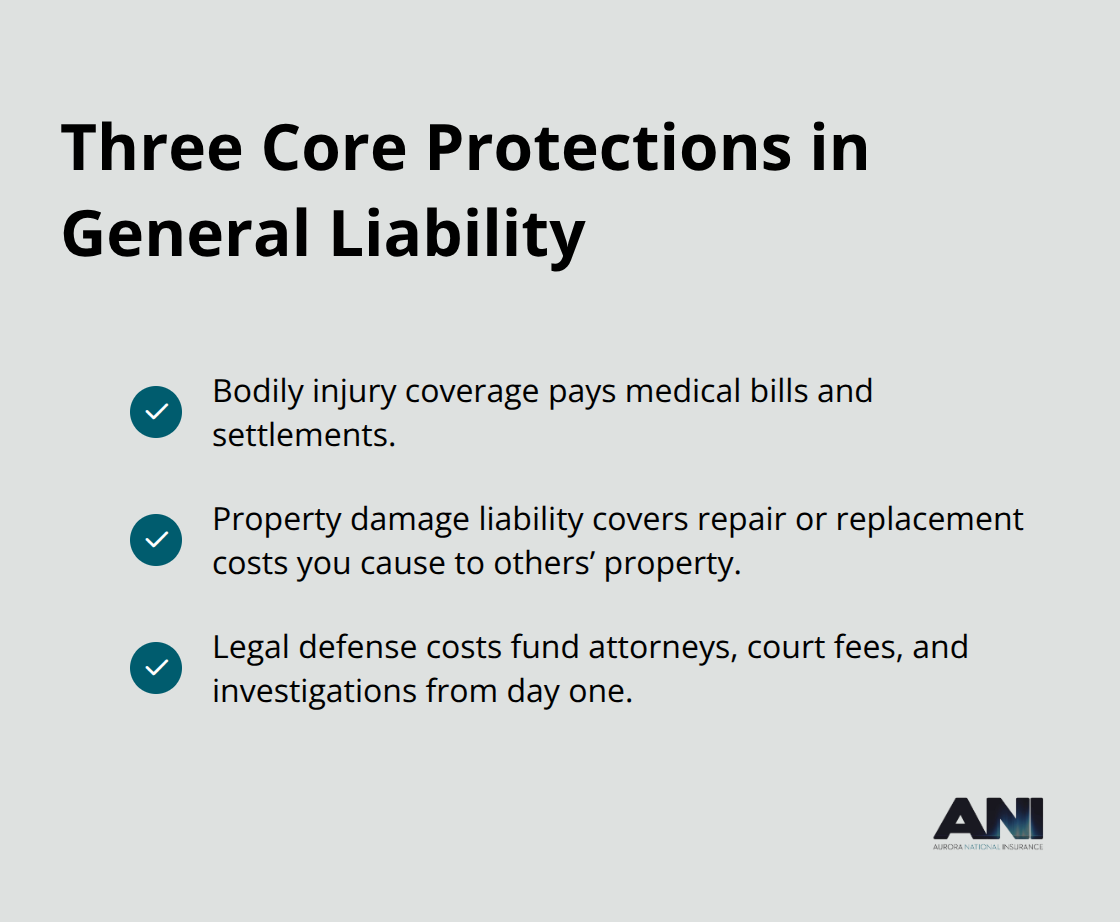

General liability insurance covers three main categories of claims that most businesses face regularly. When a customer slips on your floor and breaks their arm, when you accidentally damage a client’s equipment during a service call, or when your advertisement unintentionally uses someone else’s trademarked slogan, your general liability policy steps in to pay medical bills, repair costs, and legal fees.

The Hartford reports that typical coverage costs around $810 per year for small businesses, which works out to roughly $67 monthly. This relatively low cost becomes a bargain the moment you face a legitimate claim, since a single serious injury or property damage incident can easily exceed $100,000 in medical expenses and legal defense costs combined.

Bodily Injury Claims on Your Premises

Medical expenses and bodily injury claims represent the most common type of general liability claim across industries. If a client suffers an injury at your location or because of your business operations, your policy covers their medical treatment regardless of who was technically at fault. This medical payments coverage applies whether the injury occurred in your office, at a client’s location, or even at a trade show where you represented your business. The coverage pays directly to the injured party’s medical providers, which often resolves minor incidents without ever escalating to a lawsuit. For serious injuries where the injured party pursues legal action, your policy’s bodily injury coverage kicks in to cover settlement amounts and court judgments up to your policy limits.

Damage to Client Property and Equipment

Property damage claims work similarly but address physical damage you cause to someone else’s belongings rather than injuries to their body. If you accidentally damage a client’s expensive equipment, destroy inventory during a service call, or cause structural damage to a rental property, your general liability policy covers the repair or replacement costs. Your policy protects you against these financial hits without requiring you to negotiate directly with the damaged party.

Legal Defense Costs That Protect Your Cash Flow

What makes general liability genuinely valuable is the legal defense costs component included in virtually all policies. When someone sues your business, your insurer pays for your lawyer, court costs, and investigation expenses from day one, even before the claim is determined to be covered. This defense cost protection means you do not drain your business cash flow fighting a lawsuit out of pocket. A claim worth $1.1 million with a $1 million per-occurrence limit means your insurer covers the full $1 million plus all defense costs, while you would be responsible for only the $100,000 overage.

Understanding what your policy covers sets the foundation for smart risk management, but knowing where coverage stops matters just as much. The gaps in general liability protection can expose your business to unexpected costs that no business owner anticipates.

Common Gaps in General Liability Coverage

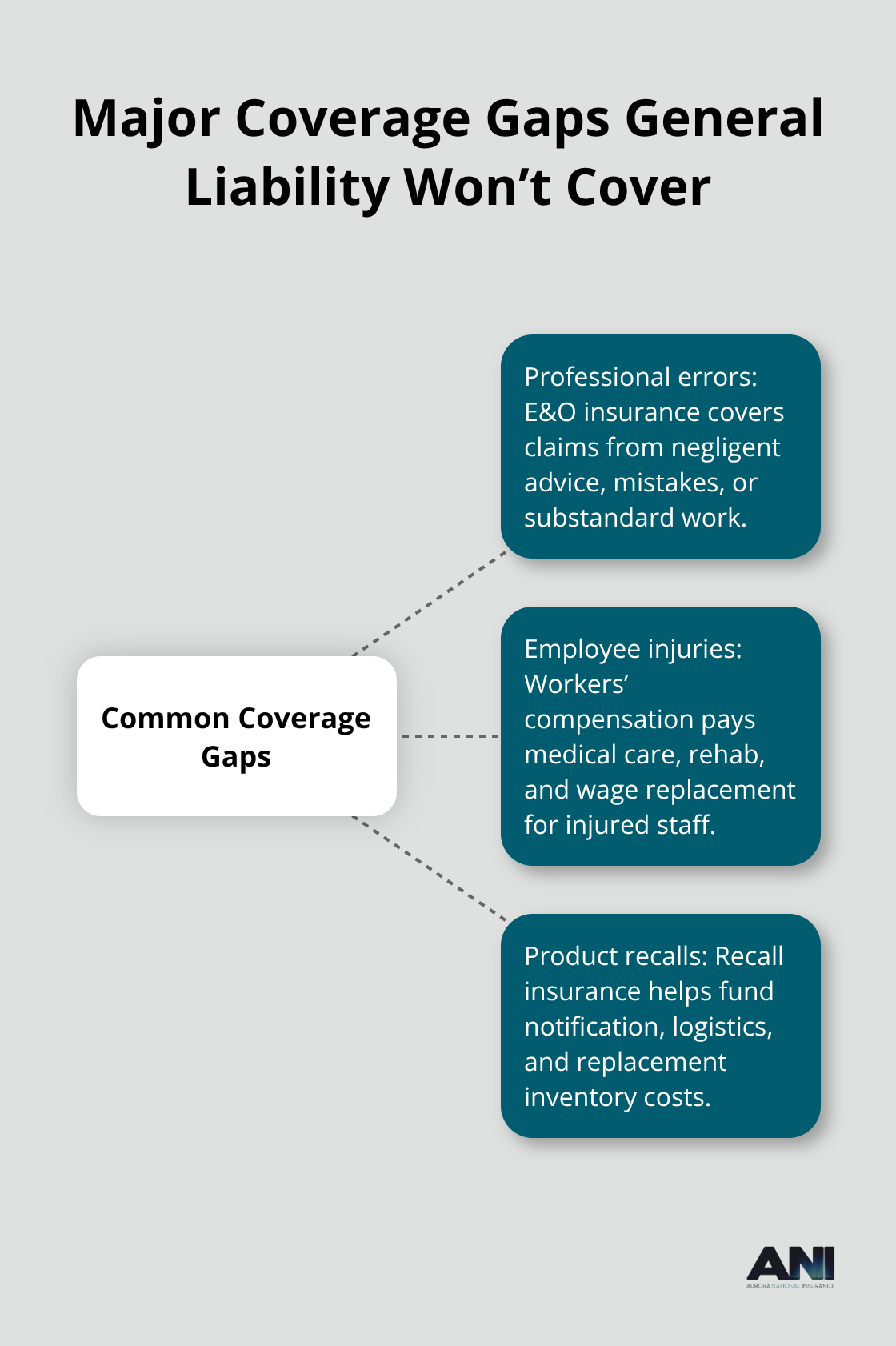

General liability insurance creates a safety net for many business risks, but it has strict boundaries that leave significant exposures unprotected. Understanding these gaps prevents costly surprises when you assume a claim will be covered only to discover your policy excludes it entirely. The most dangerous gaps affect service providers, businesses with employees, and companies that manufacture or sell products.

Professional Errors Fall Outside Your Coverage

Service-based businesses face the biggest coverage blind spot: general liability explicitly excludes professional errors and negligence. If you work as an accountant and miscalculate a client’s taxes, an architect whose design has structural flaws, or a consultant whose advice costs a client money, general liability will not pay for the resulting damages. Many service providers operate under the false assumption that their general liability policy protects them from professional liability claims, then face devastating out-of-pocket costs when a client sues. Professional liability insurance, also called errors and omissions coverage, protects businesses that provide expert advice and services against claims of negligence or substandard work. Service providers who work under contracts frequently discover that clients require proof of professional liability coverage before signing agreements, so this gap affects your ability to win business, not just your protection after a claim occurs.

Employee Injuries Require Workers’ Compensation

General liability explicitly excludes injuries to your own employees, which is where workers’ compensation insurance takes over. If an employee gets hurt on the job, your general liability policy will deny the claim outright, leaving you personally liable for medical bills and lost wages. Workers’ compensation is mandatory in most states and covers medical treatment, rehabilitation costs, and wage replacement for injured workers. Many small business owners bundle workers’ compensation with their general liability through a Business Owner’s Policy to simplify administration and often receive modest cost savings.

Product Defects and Recall Costs Need Separate Protection

Product defects and product recalls represent another significant gap that many manufacturers and retailers overlook. If a product you sell causes injury or property damage, general liability covers the injury claim itself, but product recall expenses, notification costs, and replacement inventory fall outside your policy. Product recall insurance can be added as an endorsement to address these costs. These three coverage gaps-professional errors, employee injuries, and product recalls-account for the majority of claims that business owners mistakenly believe their general liability policy will cover. Identifying which gaps apply to your specific business model determines what additional policies you actually need to protect your assets and operations.

How to Choose the Right Coverage Limits

Most business owners select coverage limits based on what competitors use or what sounds reasonable, rather than analyzing their actual financial exposure. A standard $1 million per-occurrence and $2 million aggregate limit works fine for some businesses but leaves others dangerously underprotected. The Hartford’s data shows small businesses typically pay around $810 annually for general liability, yet many spend that same amount on inadequate limits that could bankrupt them if a serious claim hits.

Calculate Your Real Financial Exposure

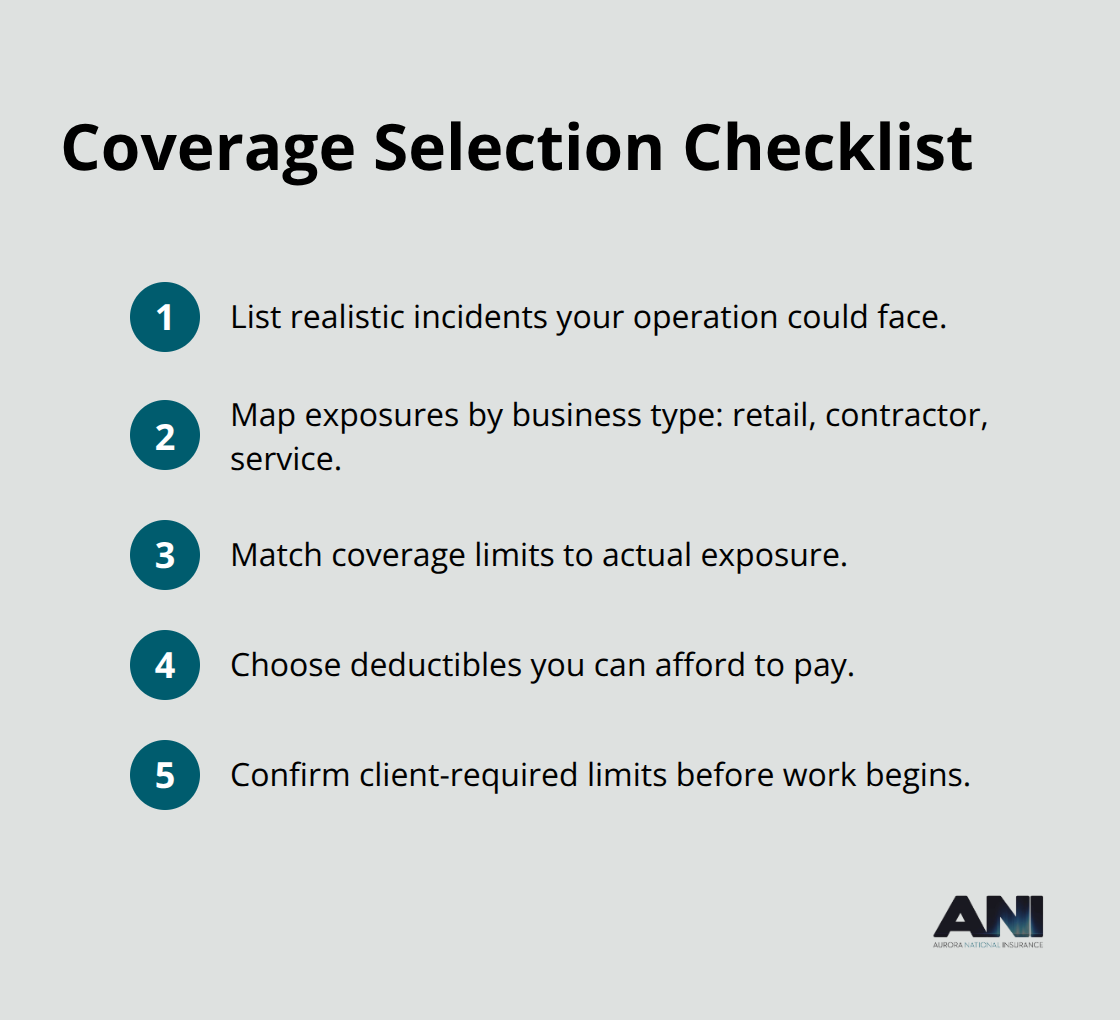

Your coverage limits should reflect three concrete factors: what you stand to lose if someone sues, what your clients contractually require, and what assets you need to protect. A landscaping company with $500,000 in annual revenue and minimal equipment needs different limits than a consulting firm managing $5 million in client projects. Start by calculating your total business assets, then add your annual revenue to understand your maximum financial exposure. If a lawsuit awards damages exceeding your per-occurrence limit, you personally cover the overage, so underestimating your exposure creates real financial risk.

Industry Risk Determines Your Baseline Limits

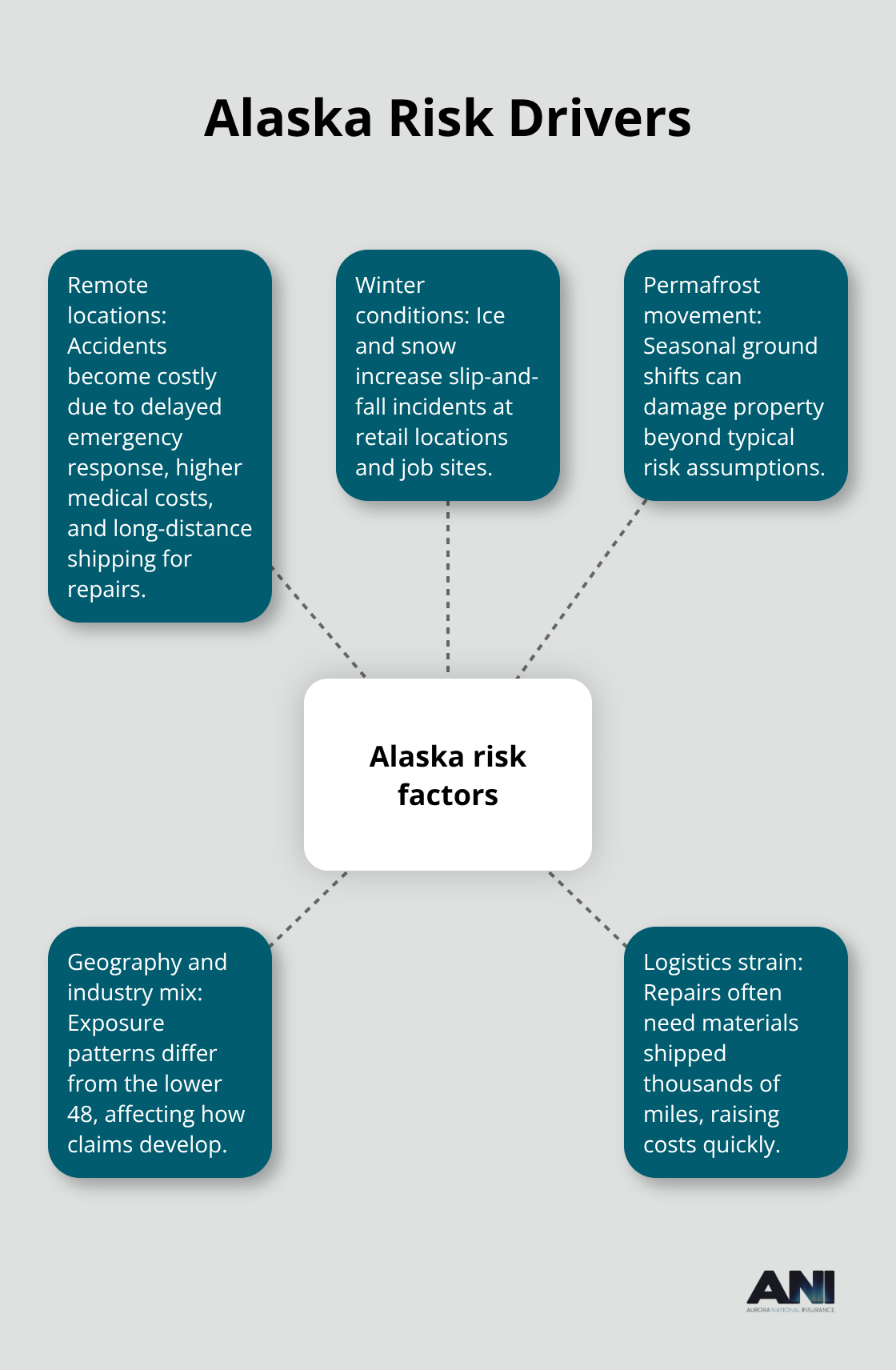

Your industry determines baseline exposure more reliably than company size alone. Contractors and service providers working on client sites face higher bodily injury risk than online retailers, which affects what limits clients will accept in contracts. Alaska-based businesses working in high-risk industries should seriously consider $2 million minimum limits, while service providers in lower-risk fields might adequately protect themselves at $1 million.

Compare Multiple Quotes at Different Limit Levels

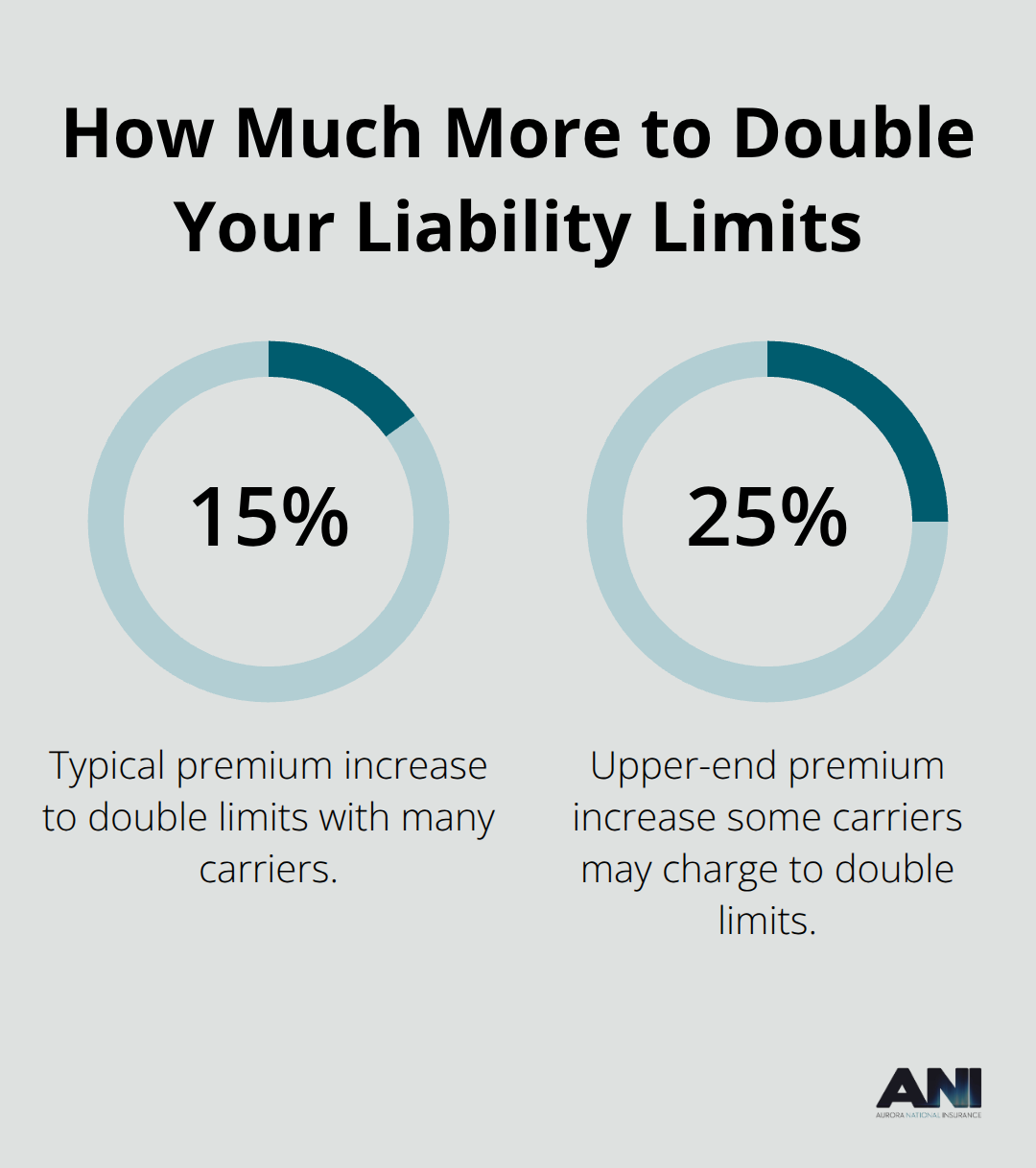

Before finalizing limits, request quotes at multiple levels-typically $500,000, $1 million, $2 million, and $3 million per-occurrence-so you see exactly how much additional premium you pay for increased protection. Most carriers charge only 15 to 25 percent more for doubling your limits, making higher protection surprisingly affordable. Review your existing contracts and leases for specific coverage requirements; many clients demand $2 million per-occurrence or higher before signing agreements with you.

Try different limit combinations with multiple carriers to compare not just prices but how different insurers rate your specific industry and risk profile, since underwriting standards vary significantly between companies.

Final Thoughts

General liability insurance coverage protects your business from the financial devastation that comes with unexpected lawsuits and injury claims. The three core protections-bodily injury coverage, property damage liability, and legal defense costs-form the foundation of responsible business risk management. Yet this protection has real boundaries, and professional errors, employee injuries, and product defects fall outside standard policies, which means you need to assess your specific business model to identify which gaps require additional coverage.

Choosing the right coverage limits matters far more than most business owners realize. A $1 million per-occurrence limit sounds substantial until you face a serious injury claim that exceeds it, leaving you personally responsible for the overage. Your industry, annual revenue, and contractual requirements should drive your limit decisions, not industry averages or what competitors carry. Most carriers charge only 15 to 25 percent more for doubled limits, making higher coverage surprisingly affordable when you compare the cost against potential financial exposure.

Start by calculating your total business assets and annual revenue to understand your maximum loss exposure. Review any existing contracts, leases, or client agreements for specific coverage requirements, since many businesses demand $2 million minimum limits before signing with you. Then get quotes from multiple carriers at your target limit levels to see exactly how different insurers evaluate your specific industry and risk profile.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.