General Liability Insurance Quotes: Quick Comparisons From Local Experts

General liability insurance protects your business from costly lawsuits and medical bills when someone gets hurt on your property or your work damages their belongings. Getting general liability insurance quotes from multiple carriers helps you find the right coverage at the best price.

At Aurora National Insurance, we know that comparing quotes can feel overwhelming. That’s why we’ve put together this guide to help you understand what’s covered, how to get quotes quickly, and what factors affect your premium.

What General Liability Insurance Really Covers

How Bodily Injury Claims Work

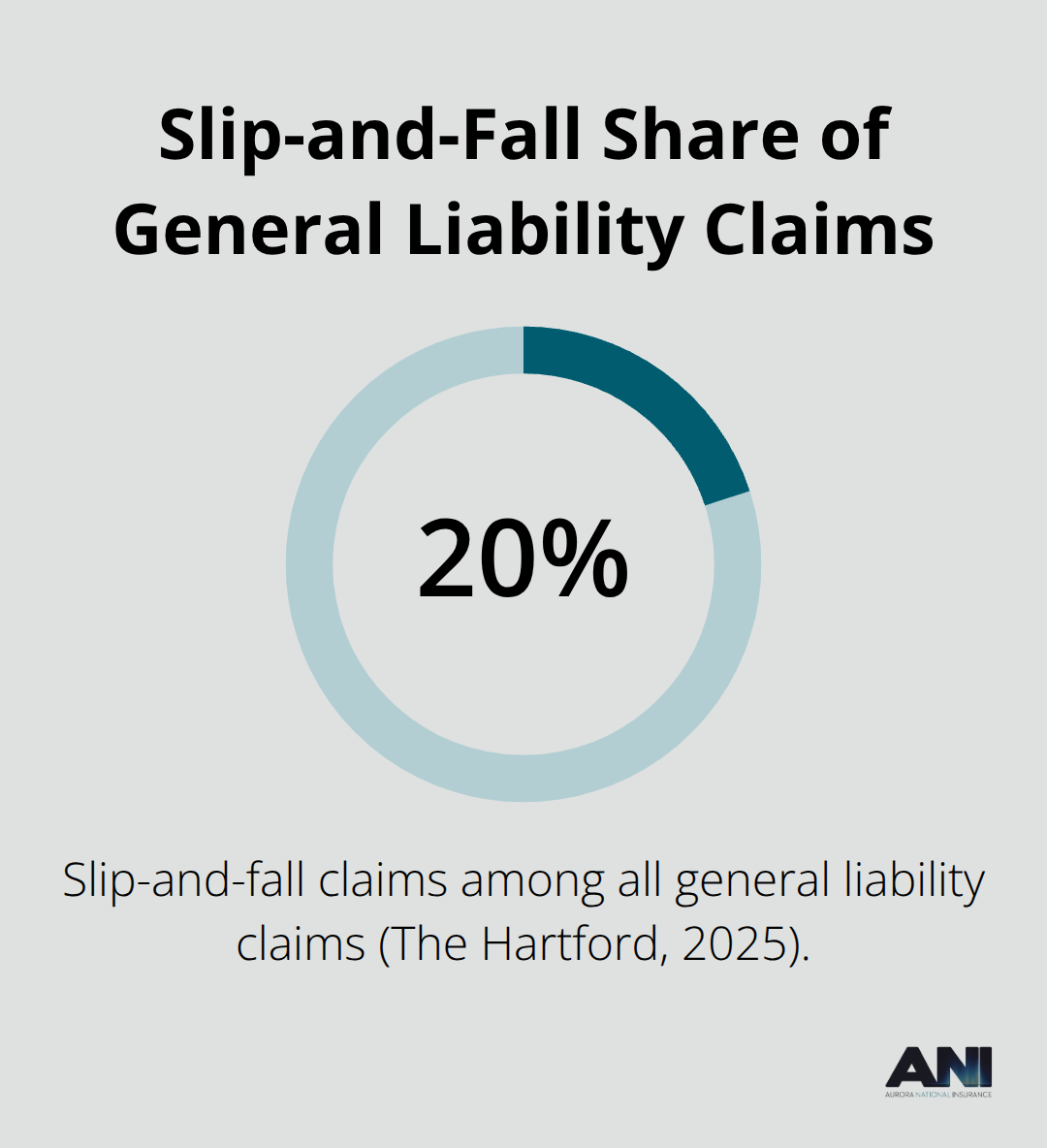

General liability insurance protects your business when someone gets hurt because of your operations. A customer slips in your retail store, a client sustains an injury at your office, or a contractor gets hurt on a job site you manage-your policy covers the medical bills and legal costs. According to The Hartford’s 2025 Small-Business Claims study, slip-and-fall claims represent about 20% of all general liability claims. This coverage pays for medical expenses and attorney fees if you face a lawsuit, protecting your business from financial ruin over a single accident.

Property Damage Liability Protection

Your business operations can damage someone else’s property, and general liability covers those costs. You back a company vehicle into a client’s fence, or your equipment damages a landlord’s building-the policy pays for repairs. This protection matters especially if you lease space or work on client premises, since landlords often require proof of this coverage before you occupy their property. Property damage liability keeps you from absorbing repair costs that could otherwise drain your cash flow.

Legal Defense and Medical Payments

General liability covers your legal defense costs and medical payments separately from any settlement or judgment. If someone sues your business, the insurer pays for your attorney and court costs without reducing your coverage limits. Medical payments coverage handles immediate medical expenses for injuries on your property, even if you’re not legally at fault-this approach often prevents small injuries from escalating into costly lawsuits.

What General Liability Does Not Cover

Understanding exclusions prevents dangerous coverage gaps. The policy excludes employee injuries (workers’ compensation handles those), vehicle accidents (commercial auto insurance covers those), professional mistakes or errors in your work, and intentional harmful acts. If you run a consulting firm, construction company, or any service business where your advice or workmanship is the core product, general liability alone won’t protect you-you need professional liability or errors and omissions coverage. Most policies also exclude punitive damages, though this varies by state.

Standard Limits and Premium Costs

A typical general liability policy carries limits of $1 million per occurrence and $2 million in aggregate, meaning you receive coverage up to $1 million for any single incident and $2 million total across all claims in a year. If your business operates in a higher-risk industry like construction, these standard limits may prove insufficient, and you should explore umbrella or excess liability coverage to raise your overall protection. The median general liability premium runs about $45 per month, but industry costs vary dramatically-retail businesses typically pay $700 to $1,500 annually, while construction can reach $5,000 or more depending on the scope of work and claims history. Understanding your industry’s typical premium range helps you evaluate whether a quote represents fair pricing or signals hidden exclusions that reduce actual protection.

Getting Quotes Online Without Wasting Time

Prepare Your Business Information First

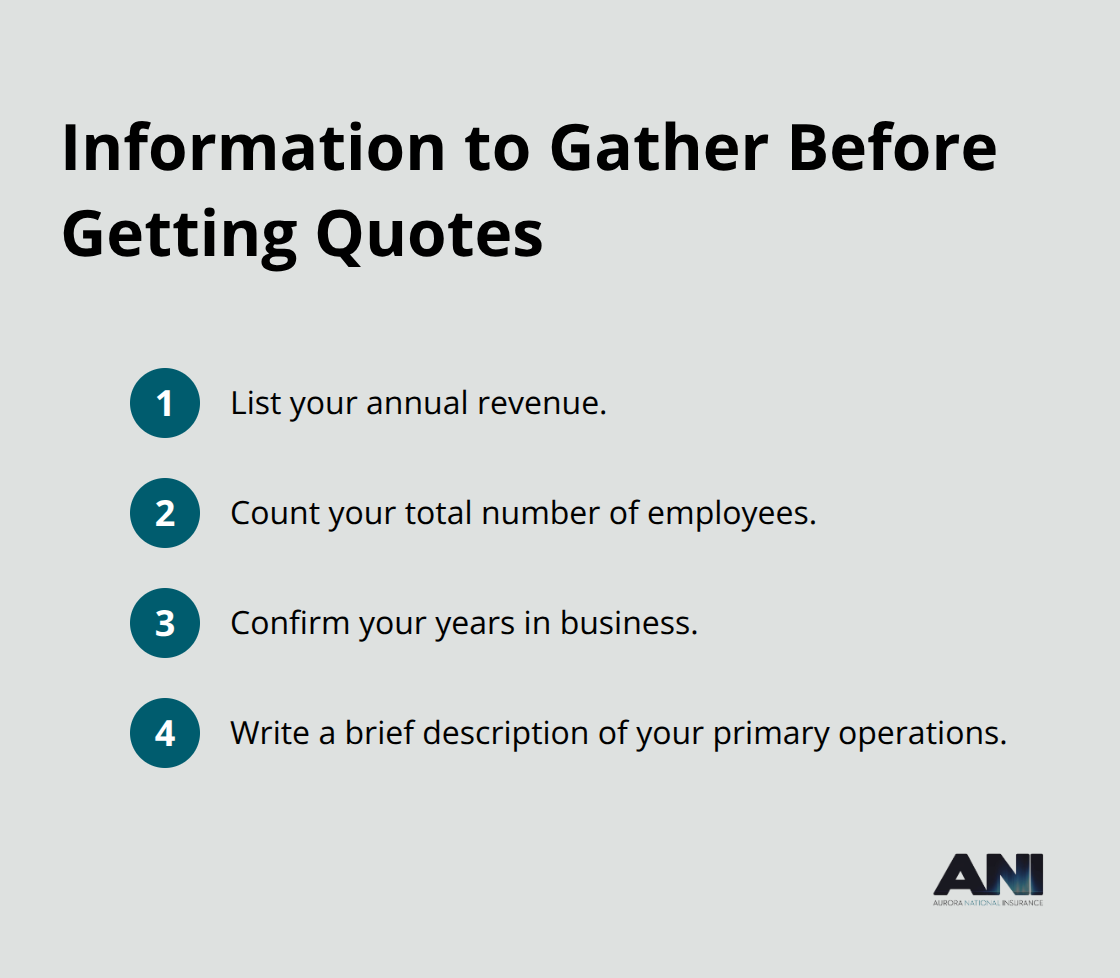

Obtaining general liability quotes online takes minutes, not hours, and most carriers let you start coverage the same day you receive your quote. The process works best when you prepare specific business details upfront rather than searching for answers mid-application. Collect your annual revenue, number of employees, years in business, and a brief description of your main operations before you open the quote tool. Preparing accurate information upfront prevents quote rejections that delay your coverage start date. Most online platforms ask three to five straightforward questions, then pull quotes from multiple insurers automatically, so you compare actual rates side by side instead of calling ten agents separately.

Compare Limits and Deductibles Carefully

Resist the temptation to pick the cheapest option without reading what’s actually covered. Two policies at different prices often differ because one excludes landlord property damage or carries a higher deductible, meaning you absorb more costs when a claim happens. Check the per-occurrence and aggregate limits carefully-a $1 million per-occurrence limit handles most incidents, but construction and high-risk trades should verify this covers their typical exposure. Deductibles typically range from $500 to $2,500, and choosing a higher deductible lowers your premium but means you pay more out of pocket when you file a claim.

Request Identical Quotes for True Comparisons

Request quotes with identical limits and deductibles from different carriers so you’re truly comparing apples to apples. Read the exclusions section in each quote-look specifically for whether the policy covers landlord property damage, third-party legal fees, and whether professional errors are excluded. If you work in a specialized field like consulting or contracting, standard general liability won’t protect you from mistakes in your work, so professional liability or errors and omissions coverage becomes necessary alongside it.

Understand What Affects Your Quote Results

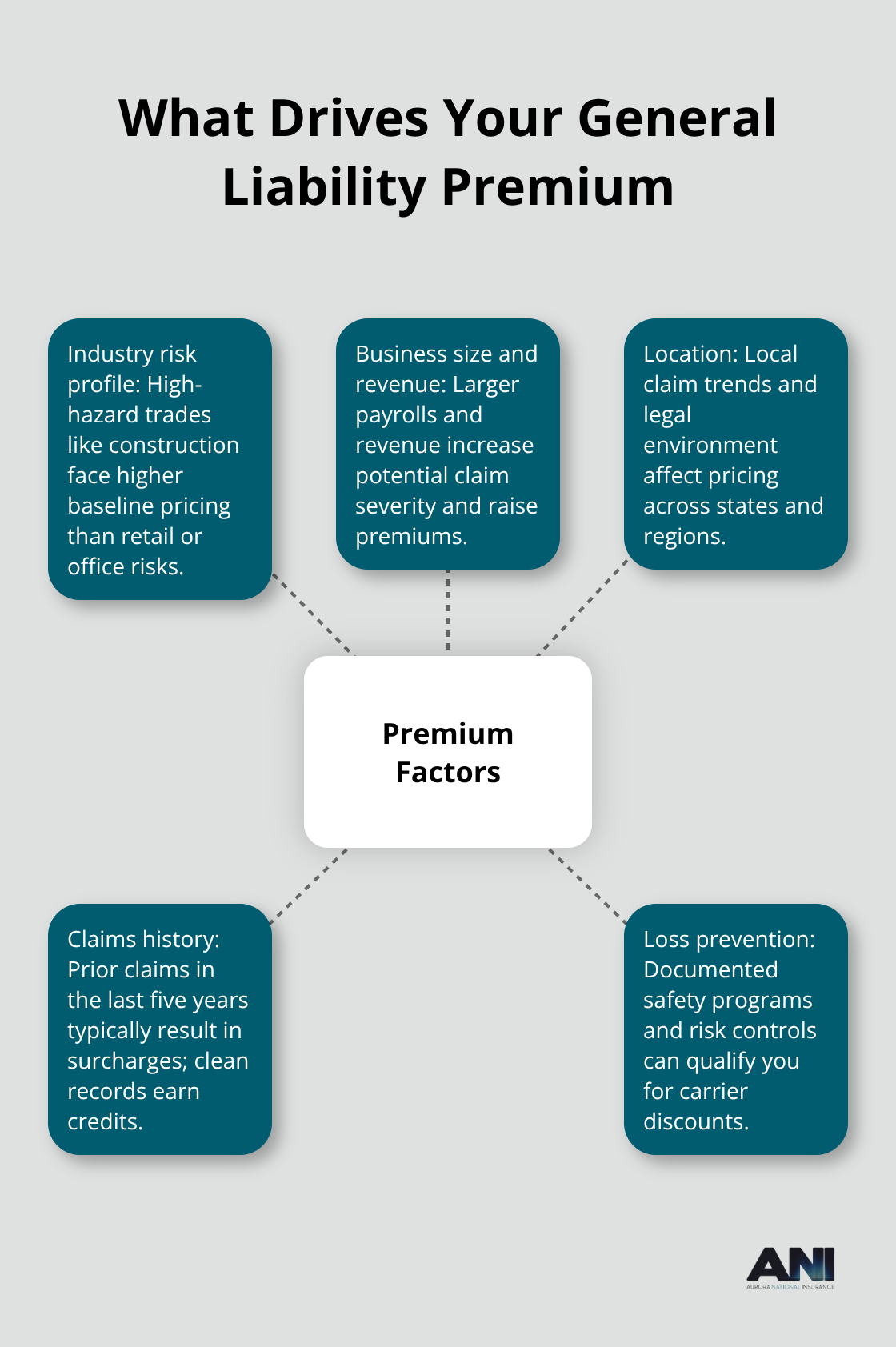

The quotes you receive reflect your industry’s risk profile, your business size, and your location. A retail store in a low-risk area pays far less than a construction company in the same region because slip-and-fall claims carry lower average costs than job-site injuries. Your claims history matters too-carriers charge more if you’ve filed claims in the past five years, while businesses with clean records qualify for better rates.

Once you’ve gathered quotes from multiple carriers and identified the coverage that fits your actual exposure, you’re ready to examine the specific factors that determine whether your premium falls at the low or high end of your industry’s range.

Key Factors That Affect Your General Liability Premium

How Your Industry Shapes Your Baseline Cost

Your industry determines your baseline risk, and insurers price accordingly. Construction companies face the highest premiums because job-site injuries, property damage claims, and equipment exposure create genuine financial hazards. Retail stores pay significantly less because slip-and-fall claims, while common, typically cost less to resolve. According to The Hartford’s 2025 Small-Business Claims study, the average slip-and-fall claim costs around $45,000, whereas construction-related bodily injury claims often exceed this substantially. Wholesale trade businesses typically pay $700 to $2,500 annually for general liability, while accommodation and food services range from $1,000 to $3,000, and construction can reach $5,000 or more.

Your specific operations within your industry matter too. A contractor who works exclusively indoors faces lower premiums than one managing exposed job sites with heavy equipment. When you request quotes, carriers ask detailed questions about your daily operations because a retail store that serves food carries different risk than one selling clothing. The more accurately you describe what your business actually does, the more precise your quote becomes.

Business Size and Revenue Impact on Premiums

Business size and revenue directly affect your premium because larger operations expose insurers to bigger potential claims. A consulting firm with one employee and $100,000 annual revenue qualifies for different pricing than one with ten employees and $1 million in revenue. Carriers examine your claims history over the past five years-if you filed claims previously, expect higher premiums because past claims predict future risk. A business with zero claims in five years qualifies for better rates than one with even a single claim.

How Loss Prevention Measures Lower Your Costs

Loss prevention measures actively reduce your premium if you document them properly. Installing security cameras, maintaining detailed safety protocols, requiring employee safety training, or implementing slip-and-fall prevention measures in retail spaces all demonstrate to insurers that you take risk seriously. Some carriers offer premium discounts for documented safety programs, so investing in prevention pays off directly in lower insurance costs. When comparing quotes from different carriers, ask explicitly whether they offer safety discounts and what documentation they require to qualify. This conversation often reveals which insurers actively reward risk management versus those who simply charge standard rates.

Final Thoughts

An independent insurance agent handles the heavy lifting of comparing general liability insurance quotes across multiple carriers, saving you hours of research and phone calls. We at Aurora National Insurance represent top-rated insurers and pull quotes from multiple sources simultaneously, so you see actual rates side by side without the legwork. Our licensed agents understand your state’s specific requirements and your industry’s typical exposures, which means we uncover coverage options and discounts you might miss on your own.

Starting your quote process today prevents the financial devastation that a single lawsuit can inflict on your business. Contact Aurora National Insurance to receive personalized comparisons from carriers aligned with your industry’s risk profile, or use online tools if you prefer handling the process independently. The cost of general liability insurance remains minimal compared to the potential damage of operating uninsured or underinsured.

Your business deserves protection that matches your actual exposure, and the fastest way to find it is requesting quotes from multiple sources right now. Whether you operate in Alaska, Washington, Oregon, or other states we serve, our agents deliver tailored comparisons that fit your real business needs. Move forward with coverage before you need it.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.