General Liability for Startups: Building a Safe Foundation

Starting a business means taking on new responsibilities-and new risks. One of the smartest moves you can make is securing general liability for startups before problems arise.

At Aurora National Insurance, we’ve seen firsthand how the right coverage protects young companies from unexpected financial damage. A single lawsuit or accident can derail your growth, but proper insurance keeps you moving forward.

What General Liability Actually Protects Your Startup From

Bodily Injury Claims That Can Drain Your Cash

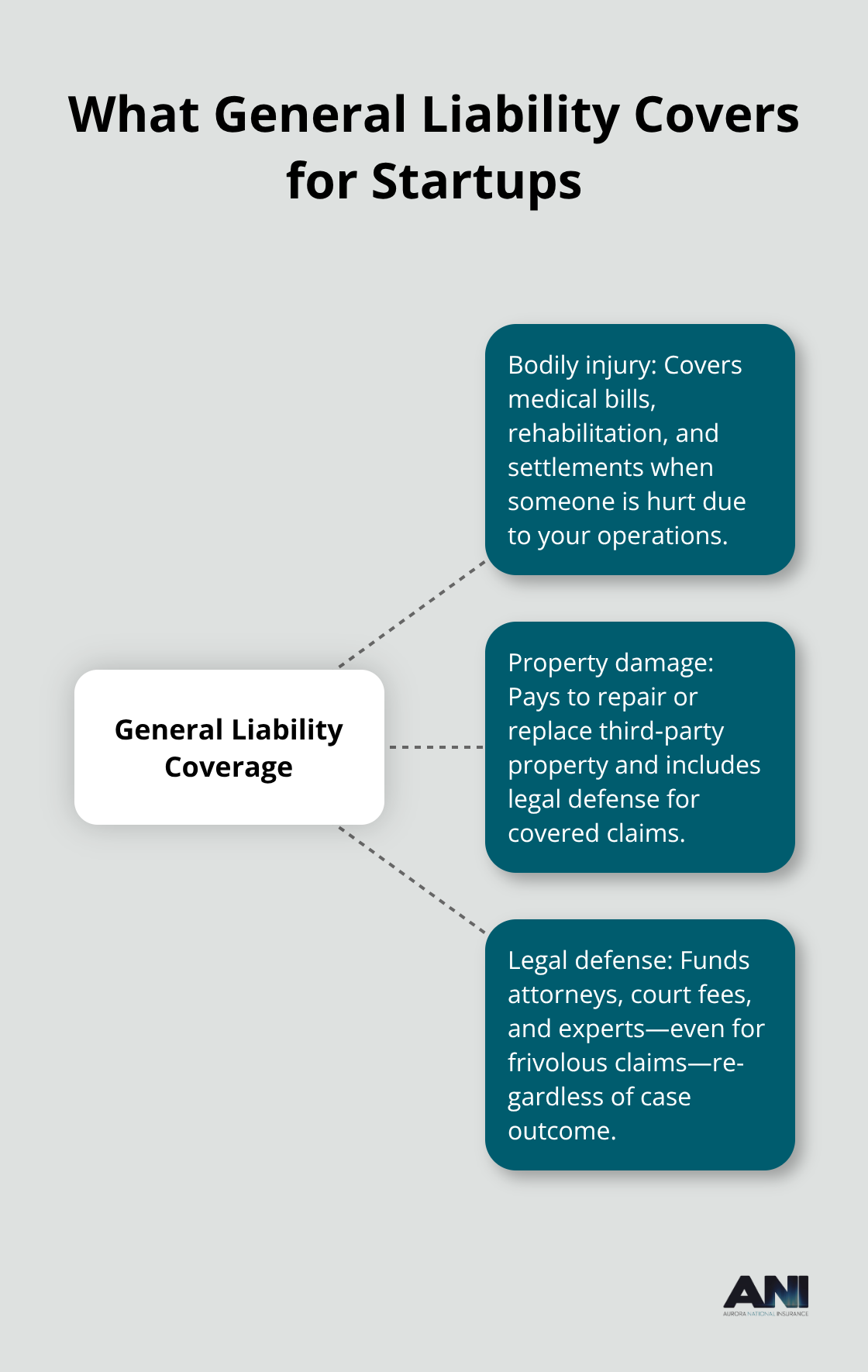

General liability insurance covers three categories of financial exposure that can bankrupt an early-stage company. First, it protects against bodily injury claims when someone gets hurt because of your business operations. A customer slips in your office, a client is injured during a service delivery, or a visitor to your premises files a lawsuit-general liability covers medical expenses, rehabilitation costs, and settlements.

Without coverage, you pay this directly from company funds.

Property Damage You Cause to Others

Second, the policy covers property damage you cause to someone else’s assets. If your equipment damages a client’s office, your delivery truck hits a parked car, or your operations destroy a third party’s inventory, general liability handles repair or replacement costs plus legal defense. These incidents happen more often than startups expect, and the repair bills add up fast.

Legal Defense Costs That Exceed Settlements

Third, the policy pays for legal defense costs and settlements even if a claim is frivolous. Defense attorneys, court fees, and expert witnesses cost thousands of dollars before any settlement is paid. Many startups underestimate this expense-a single lawsuit can drain $50,000 in legal fees alone. The policy covers these costs regardless of whether you win or lose the case.

Why Coverage Matters Before You Need It

The real value of general liability emerges when you face an actual incident. Many landlords, clients, and contractors won’t work with you without proof of coverage. A claim that should have been covered becomes a personal liability if your policy lapsed or limits were too low. The cost is minimal-around $42 per month for many startups-compared to the financial devastation of uninsured liability.

Your business grows when you eliminate the constant worry that one accident will wipe out months of revenue. Securing coverage before your first customer walks through the door protects your startup from the moment operations begin. This foundation allows you to focus on growth rather than catastrophic risk.

Common Risks Startups Face Without Coverage

Slip-and-Fall Incidents Cost More Than You Expect

Slip-and-fall incidents on your premises represent one of the most common liability exposures startups overlook. The National Safety Council reports that slip-and-fall incidents cost an average of $25,000 per claim, yet many founders assume their landlord’s insurance covers injuries that occur in their leased office or workspace. It does not. If a client trips over a cable in your office, a vendor slips on a wet floor, or a customer sustains an injury during a service you provide on their site, you face the bill for medical treatment, lost wages, and legal defense. These costs accumulate quickly. Even minor incidents create liability exposure. A startup without general liability coverage must either negotiate with the injured party or face a lawsuit where legal fees alone drain company cash before any damages are determined.

Third-Party Property Damage Claims Add Up Fast

Damage to third-party property happens more frequently than startups anticipate, and the financial impact varies wildly depending on what gets damaged. If your equipment damages a client’s machinery, your delivery truck hits someone’s vehicle, or your operations destroy inventory in a shared workspace, you become responsible for full repair or replacement costs. Beyond physical damage, product liability claims arise when something you sold or delivered causes harm-a defective component injures someone, a software error costs a client money, or a completed project fails and damages a customer’s business. These claims do not disappear because you did not intend harm; they exist because your product or service caused financial or physical loss.

Legal Battles Drain Resources and Attention

Without coverage, you pay reconstruction costs, replacement expenses, and legal defense from operating capital. Startups in software, manufacturing, construction, and service industries face particularly high exposure in this category. The real danger emerges when a third party’s insurance company pursues you for damages, creating a legal battle where your startup must hire attorneys and fight claims that an insurance carrier could have handled. This scenario forces you to choose between settling expensive claims or spending months in litigation that diverts management attention from business operations. The financial and operational toll of uninsured liability extends far beyond the initial claim amount-it threatens your ability to execute your business strategy and retain focus on growth.

How to Choose the Right General Liability Policy

Match Coverage Limits to Your Industry’s Real Risks

Your industry determines what general liability coverage you actually need, and selecting the wrong limits creates two problems: you either pay for protection you do not use, or you face a catastrophic claim that exceeds your policy limits. A software startup handling client data faces different risks than a consulting firm that visits client offices, which faces different risks than a product manufacturer. Start by mapping your specific operations to real liability scenarios. If you deliver services on-site at client locations, premises liability exposure is high because you control the work environment and client injuries fall directly on you. If you manufacture or sell products, product liability claims become your primary concern because defects or failures can cause widespread damage. If you operate from a leased office where clients visit, slip-and-fall incidents represent your biggest exposure.

Once you identify your primary risk category, research actual claim costs in your industry rather than accepting generic numbers. The National Safety Council reports slip-and-fall claims average $25,000, but your industry may see higher or lower costs depending on what gets damaged and who typically files claims. A construction startup faces higher bodily injury exposure than a marketing agency, so coverage limits should reflect that reality.

Set Limits That Protect Against Realistic Worst-Case Scenarios

Many startups select the lowest available limits to minimize premiums, but inadequate limits create uninsured liability that destroys the entire point of buying insurance. If you choose $300,000 in general liability coverage and face a $500,000 claim, you absorb the $200,000 gap from company funds. Industry standards exist for good reason: a $1 million aggregate limit represents the minimum floor for most startups because that coverage costs only slightly more than lower limits while protecting against realistic worst-case scenarios.

Your lease agreements and client contracts often dictate minimum coverage requirements anyway, so check those documents before selecting limits. Many landlords and clients will not work with you without proof of adequate coverage, making this step essential before you sign any agreements.

Compare Quotes Across Multiple Carriers

Comparing quotes from multiple carriers reveals dramatic price differences for identical coverage, and shopping around saves thousands of dollars over three years. Request quotes from at least three different insurers using identical coverage specifications so you can directly compare apples to apples. Premium variation reflects different underwriting approaches, risk assessment methodologies, and carrier appetite for your specific industry. One carrier might specialize in tech startups and offer competitive rates while another focuses on manufacturing and prices tech clients higher.

When comparing quotes, examine deductibles carefully because higher deductibles lower premiums but increase your out-of-pocket costs when claims occur. A startup with strong cash reserves can afford a $5,000 deductible to save premium dollars, while a bootstrapped startup should stick with $1,000 deductibles even if premiums cost more. Do not let premium price alone drive your decision because the cheapest quote often comes from a carrier with poor claims service or financial instability. Verify carrier financial ratings through A.M. Best or the National Association of Insurance Commissioners before committing.

Evaluate Bundled Policies Against Standalone Coverage

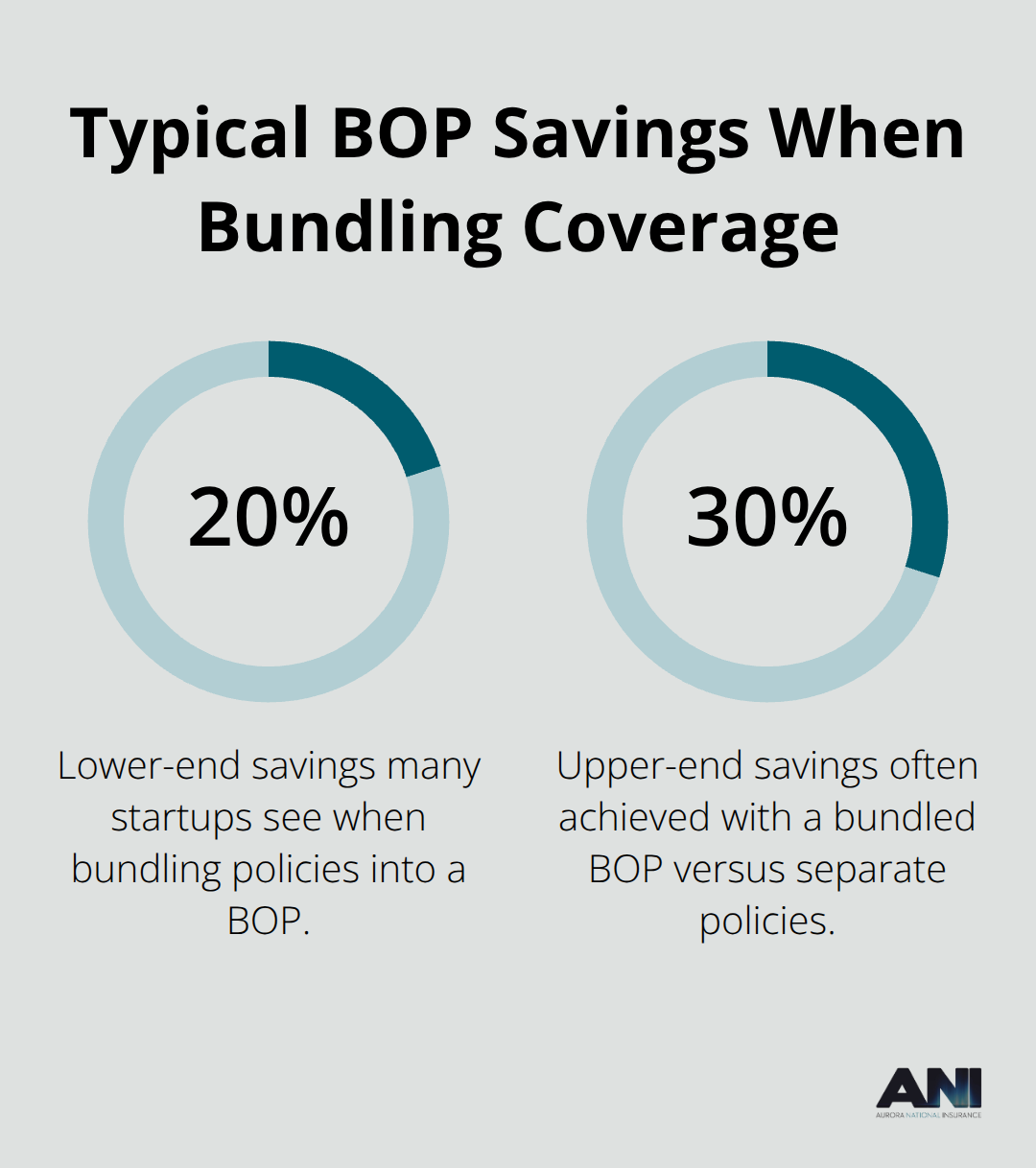

Some startups benefit from bundling general liability with commercial property coverage into a Business Owner’s Policy because bundled policies typically cost 20 to 30 percent less than purchasing policies separately. A BOP combines general liability and property coverage into one package, which works well for startups occupying leased office space, but does not work for all business types.

If you operate from home or do not own significant equipment or inventory, a standalone general liability policy makes more financial sense than paying for property coverage you do not need. Request quotes for both scenarios and compare total annual costs rather than comparing individual policy prices.

Final Thoughts

General liability for startups protects your business from the financial devastation that one accident can cause. The incidents covered throughout this article happen regularly, and the costs are real-a single slip-and-fall claim, property damage incident, or product liability lawsuit consumes months of revenue and forces difficult decisions about your company’s survival. Insurance transfers that risk to a carrier equipped to handle claims professionally, eliminating the constant anxiety that one accident will destroy everything you built.

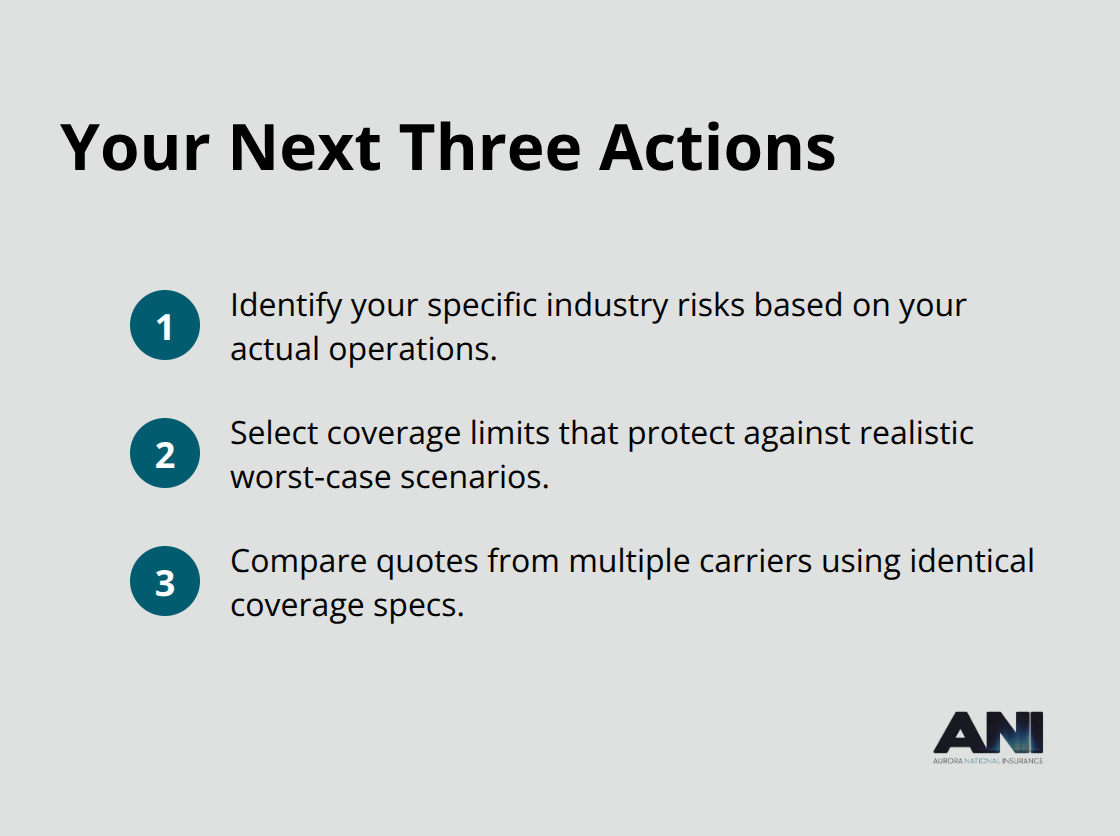

Three actions move you forward immediately. First, identify your specific industry risks by mapping your actual operations to liability scenarios rather than accepting generic coverage recommendations. Second, select coverage limits that protect against realistic worst-case scenarios in your industry, not the lowest available limits that create dangerous gaps in protection.

Third, compare quotes from multiple carriers using identical coverage specifications so you identify the best combination of price and financial stability for your startup.

Landlords, clients, and contractors increasingly require proof of general liability for startups before they work with you, making insurance a practical requirement for business operations rather than an optional safeguard. Investors and lenders view comprehensive coverage as a sign of mature risk management, which strengthens your credibility during funding conversations. Get started with a free quote at Aurora National Insurance and take the first step toward building a safe foundation for your startup’s growth.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.