General Liability Coverage Alaska: Custom Plans for Remote Worksites

Running a business in Alaska’s remote worksites exposes you to risks that standard policies simply don’t cover. Extreme weather, isolation, and difficult terrain create liability scenarios most insurers don’t anticipate.

General liability coverage in Alaska needs to reflect your actual operations, not generic templates. We at Aurora National Insurance build custom plans that protect you where you work.

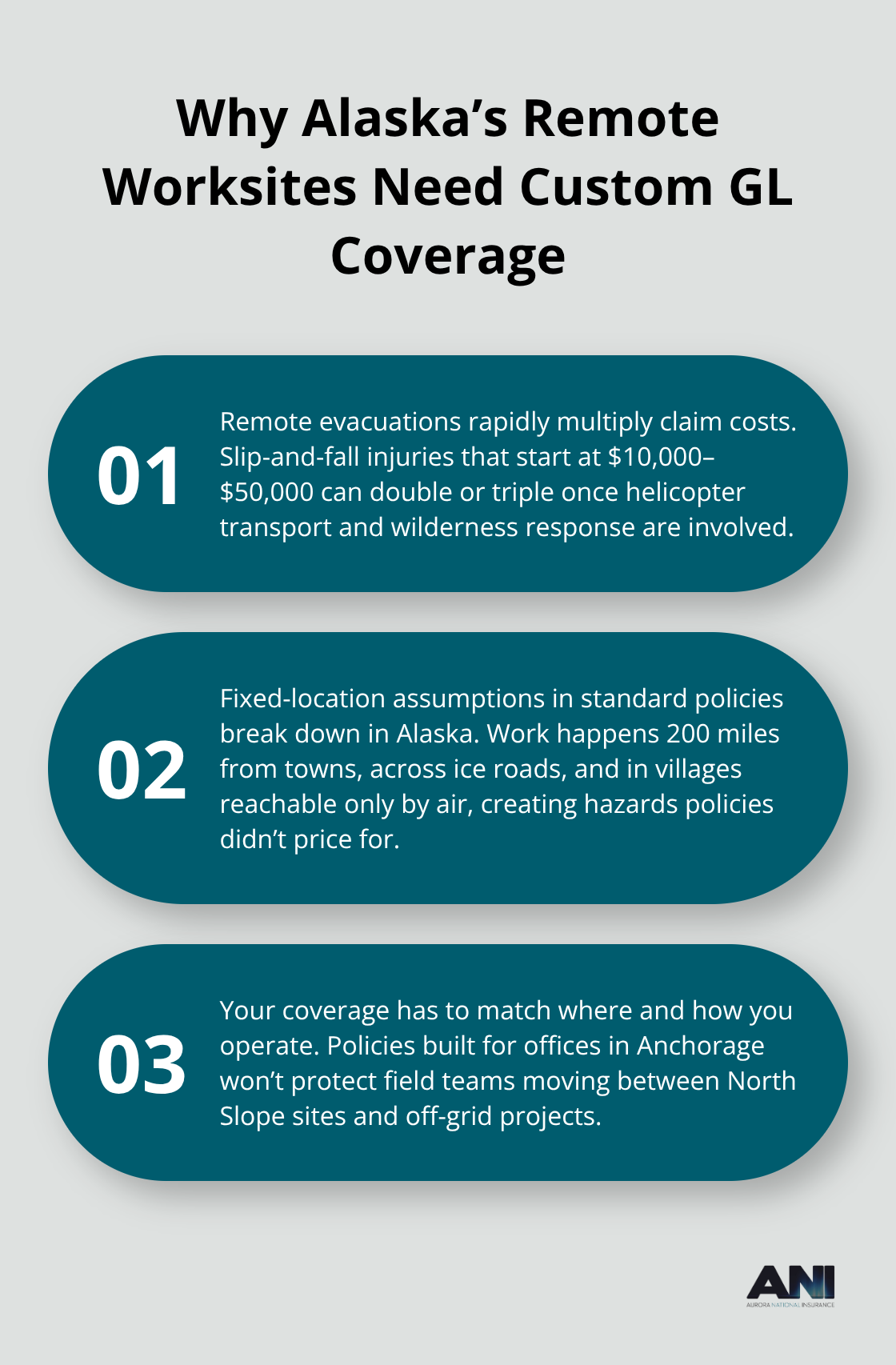

Why Alaska’s Remote Worksites Demand Different Coverage

Standard general liability policies assume your business operates from a fixed location with controlled access and predictable hazards. Alaska’s remote worksites violate every assumption insurers build into those policies. Slip-and-fall medical costs in Alaska commonly range from $10,000 to $50,000, but evacuation expenses in remote areas push claims far higher-sometimes doubling or tripling the initial injury cost. A standard policy written for an office in Anchorage won’t protect you when an accident happens 200 miles away on the North Slope or in a remote village accessible only by helicopter.

How Alaska’s Terrain Multiplies Liability Exposure

Winter ice, uneven terrain, and long emergency-response times create injury scenarios that generic coverage simply doesn’t anticipate. Your liability doesn’t stay in one place; it follows you to client sites, job locations, and temporary worksites across the state. Standard commercial policies assume a fixed location with controlled access, which remote work violates entirely. A policy designed for another state or business model will leave you underprotected when Alaska-specific conditions trigger claims.

Environmental and Geographic Hazards Drive Up Claim Costs

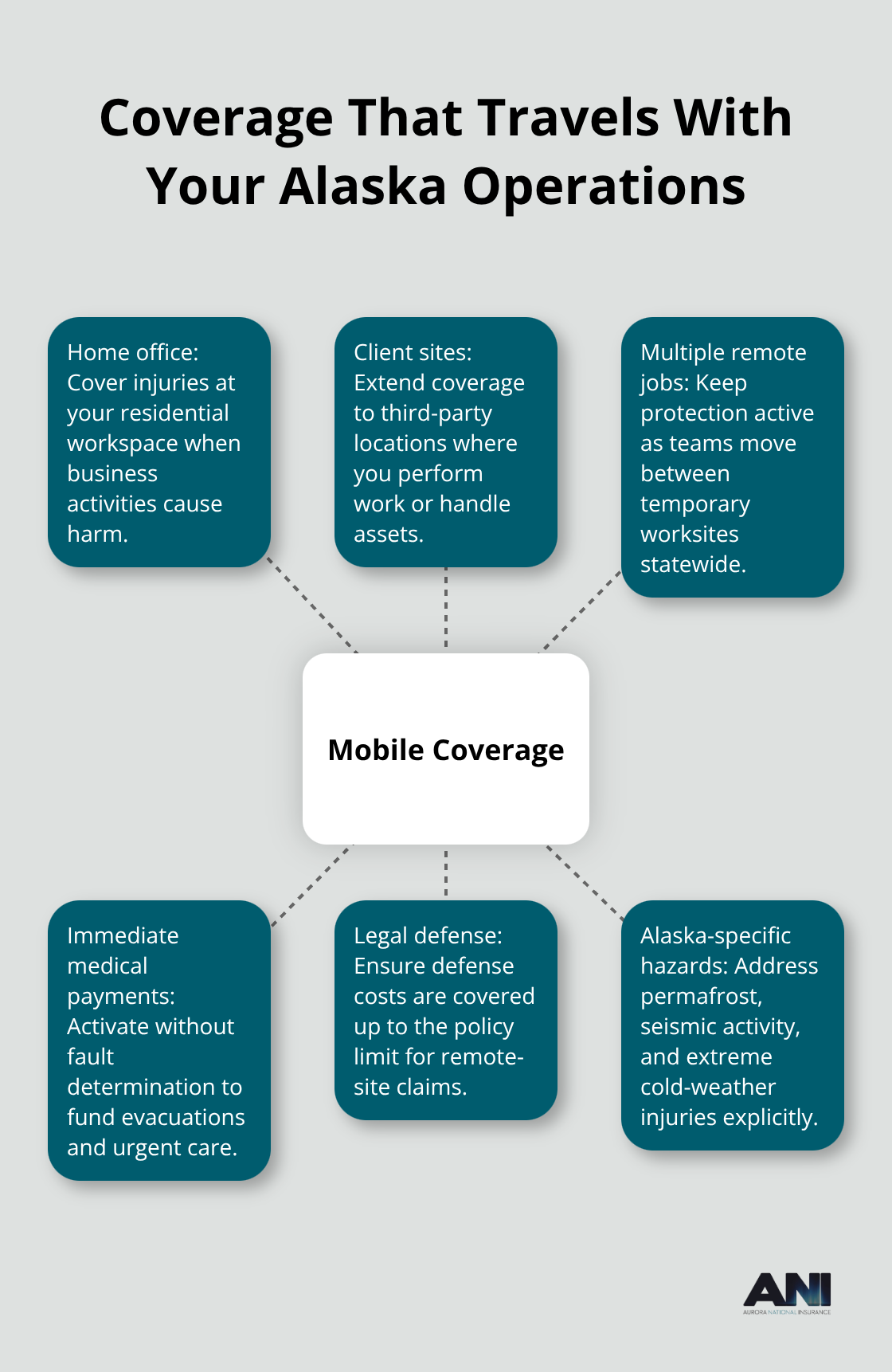

Alaska’s terrain and weather increase medical costs and claim complexity far beyond national averages. Remote work in Alaska shifts liability into home offices and mobile work sites, making standard homeowners’ policies inadequate for business injuries. If you work from home and also travel to client sites, a typical commercial GL policy written for a fixed location leaves dangerous gaps-injuries at your residential workspace aren’t covered, and damage at client locations may fall outside the policy scope.

Coverage Must Travel With Your Operations

Environmental hazards specific to Alaska (permafrost subsidence, seismic activity, extreme cold-weather injuries) require coverage that explicitly addresses these exposures. Your coverage must travel with you and your activities across multiple remote job sites, and it must activate medical payments immediately without requiring fault determination, since evacuation and emergency response can’t wait for liability investigation. The right policy protects injuries at your residential workspace as well as damage at client locations, plus immediate medical payments without fault determination.

What Coverage Limits Protect Alaska Remote Worksites

Starting With the Right Bodily Injury and Property Damage Limits

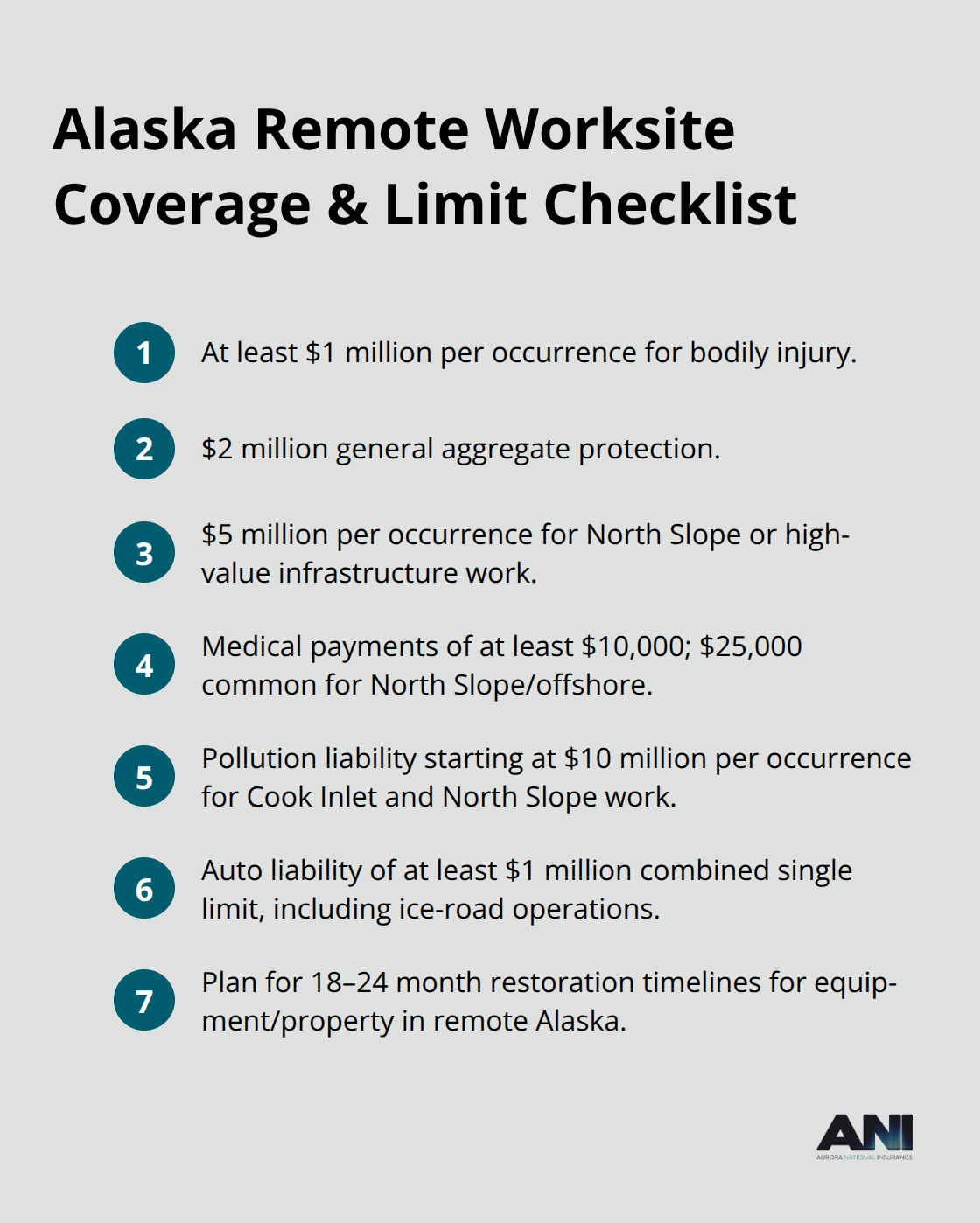

Bodily injury and property damage coverage form the foundation of any remote worksite policy in Alaska, but standard limits won’t protect you adequately. Alaska’s higher medical and evacuation costs demand that you right-size your coverage to match actual exposure rather than accepting national defaults. Start with bodily injury limits of at least $1 million per occurrence, with $2 million in general aggregate protection. This baseline reflects what most Alaska service contracts require, but your specific limits should track your contract terms and the value of property or equipment you handle at client locations. If you work on North Slope operations or handle high-value infrastructure, $5 million per occurrence becomes the practical minimum.

Medical Payments Coverage That Activates Without Delay

Medical payments coverage should activate immediately without fault determination, since evacuation and emergency response in remote Alaska can’t wait for liability investigation. Try for medical payments of at least $10,000 to cover initial emergency costs and transport, though North Slope and offshore operations often require $25,000 or higher. This coverage pays immediate medical costs regardless of who caused the injury, which matters when a worker needs helicopter evacuation from a remote site and the clock is running.

Environmental Liability for Alaska’s Aging Infrastructure

Environmental liability in Alaska’s harsh climate requires explicit attention because aging infrastructure, permafrost subsidence, and seismic activity create pollution exposures that standard policies exclude entirely. Cook Inlet operations and North Slope work need pollution liability starting at $10 million per occurrence, with gradual pollution coverage for aging equipment and cleanup cost protection. This coverage protects you when equipment leaks or environmental conditions deteriorate over time, not just from sudden spills.

Equipment and Vehicle Coverage Across Remote Job Sites

Alaska’s extreme cold, ice roads with seasonal access, and remote delivery logistics create equipment and vehicle exposures that demand higher restoration periods and replacement-cost valuation. Property coverage should account for 18- to 24-month restoration timelines due to Arctic delivery delays, and your auto liability should cover ice-road operations and cargo coverage for in-transit equipment at limits of at least $1 million combined single limit. These extended timelines reflect the reality that replacing equipment or vehicles in remote Alaska takes far longer than in the lower 48 states.

Tailoring Coverage to Your Specific Operations

Property damage coverage protects third-party assets at client sites, but you also need coverage that travels with your equipment and vehicles across multiple job locations. Your policy should explicitly cover home-office operations, client-site work, and equipment stored at home to avoid gaps when liability arises at non-traditional spaces like coffee shops, coworking spaces, or remote job sites. The next section walks through how to assess your operational risks and work with local agents who understand Alaska’s unique exposures.

How to Right-Size Coverage for Your Alaska Operations

Assess Your Actual Liability Exposure

Start by listing every location where work happens: your home office, client sites, temporary job locations, and any facilities you access regularly. Next, document what you handle at each location-equipment value, client assets you touch, the number of people present, and environmental hazards specific to that site. A remote North Slope worksite with permafrost risk and extreme cold demands different coverage than a seasonal Cook Inlet project near populated areas.

Quantify your exposure by adding up the replacement cost of equipment you own, the value of client property you’re responsible for, and potential medical costs from injuries. Alaska’s slip-and-fall injury costs depend on many factors, including the severity of your injuries and the cost of your medical treatment. Your bodily injury limit should exceed your worst-case medical scenario by a comfortable margin.

Set Property Damage and Bodily Injury Limits

Property damage limits should cover the total value of client assets you handle plus your own equipment. If you work on contracts, check what limits the client actually requires-many Alaska service contracts specify $1 million per occurrence and $2 million aggregate, but don’t assume that’s your ceiling. Review your lease agreements and licensing requirements too; Alaska contractors need $20,000 for property damage, $50,000 bodily injury per person, and $100,000 per occurrence as state minimums, but real-world contract demands run much higher. Document these numbers in a simple spreadsheet so you have a clear picture of your exposure before talking to any agent.

Work With Local Alaska Agents

Local Alaska agents understand permafrost subsidence, ice-road seasonality, seismic risk, and extreme-weather claim patterns in ways national carriers simply don’t. An agent based in Anchorage or Fairbanks knows that Cook Inlet operations face tidal extremes and marine exposures that require specialized endorsements, while North Slope work demands pollution liability, control-of-well coverage, and extended restoration periods for equipment replacement. They also know which carriers actually price competitively in Alaska and which ones treat the state as a high-risk outlier.

When you contact an agent, bring your operational risk assessment and your contract requirements. Request quotes with identical limits and deductibles across multiple carriers so you can compare apples to apples; don’t let agents quote you different coverage combinations because you won’t know what’s driving price differences.

Verify Coverage for Remote Worksite Specifics

For remote worksites, ask specifically whether the policy covers home-office operations, multiple job sites, and Alaska-specific hazards like permafrost and seismic activity. Verify that medical payments coverage activates without fault determination and that legal defense costs are covered up to the policy limit. If you work seasonally or on projects with defined end dates, ask how coverage adjusts as your project duration changes. A three-month summer job on the North Slope has different risk than year-round operations, and your premium and coverage should reflect that reality.

An independent Alaska agency like Aurora National Insurance represents multiple top-rated carriers and leverages local expertise to deliver tailored comparisons and competitive pricing, with instant online quotes available so you can see options immediately.

Final Thoughts

Custom general liability coverage Alaska plans eliminate the financial exposure that standard policies leave open. When you work in remote locations across Alaska, a one-size-fits-all policy from a national carrier won’t protect you against the specific hazards you face daily. The slip-and-fall injuries, evacuation costs, environmental risks, and equipment damage that happen in Alaska’s harsh conditions demand coverage built around your actual operations, not generic assumptions.

Getting started with the right coverage takes three concrete steps. First, document your operational risks by listing every location where work happens and quantifying the equipment and client assets you handle at each site. Second, gather your contract requirements and licensing obligations so you know exactly what limits and endorsements you must carry. Third, connect with an Alaska-based agent who understands permafrost subsidence, ice-road seasonality, seismic risk, and the claim patterns that drive costs in remote worksites.

We at Aurora National Insurance represent multiple top-rated carriers and bring local Alaskan expertise to every quote and consultation. Request a quote at Aurora National Insurance and bring your operational risk assessment and contract requirements so our agents can walk you through coverage options tailored to Alaska’s unique exposures. The right coverage costs less than the financial damage a single uninsured claim can cause.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.