Construction Company Auto Insurance: Protecting Your Heavy-Duty Fleet

Construction company auto insurance isn’t a one-size-fits-all product. Your fleet faces risks that standard commercial policies simply don’t cover.

At Aurora National Insurance, we’ve seen firsthand how the wrong coverage leaves construction businesses exposed to costly claims. This guide walks you through the specialized protection your heavy-duty vehicles actually need.

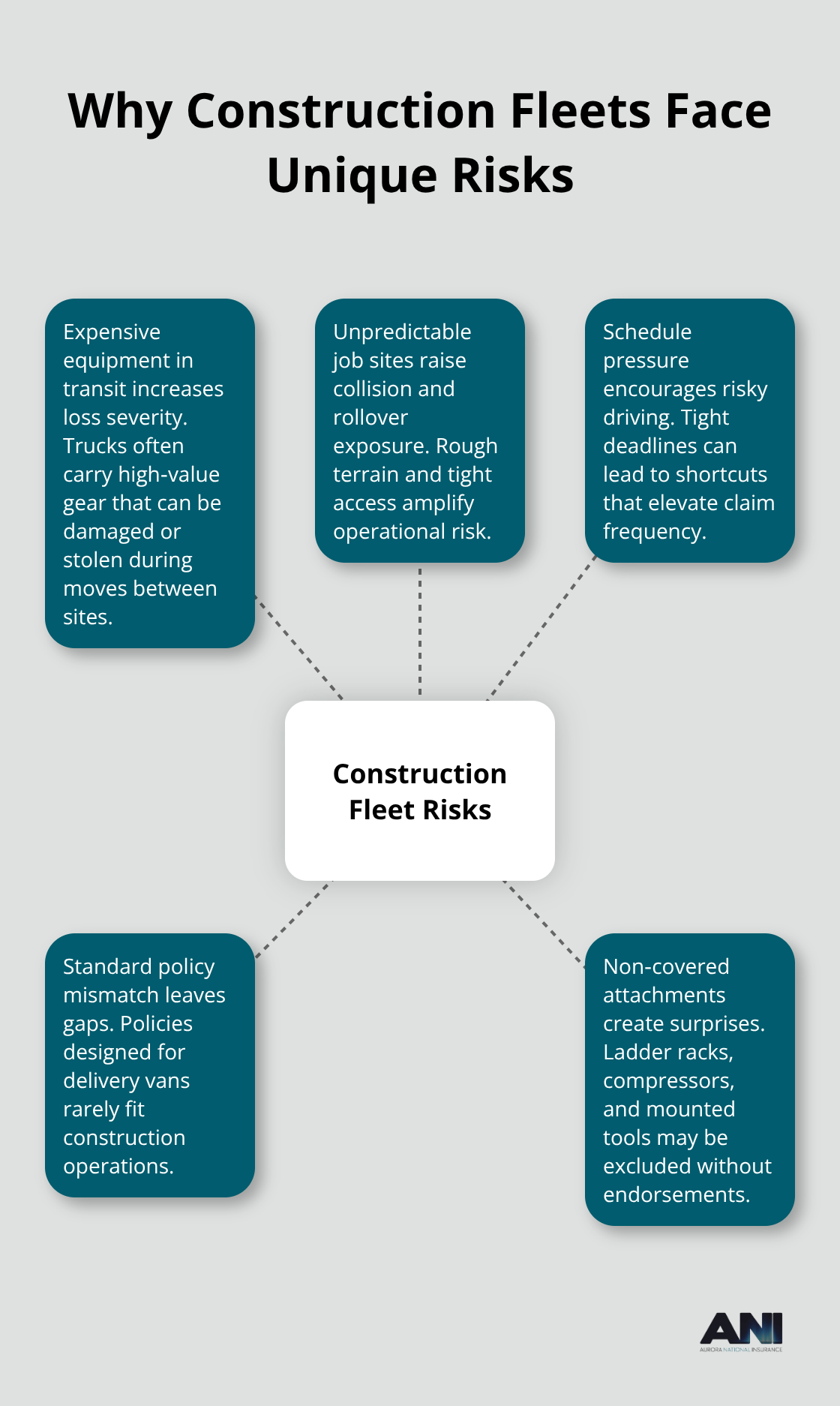

Why Your Construction Fleet Needs Different Coverage

Construction vehicles operate in an entirely different risk environment than standard commercial fleets. Heavy-duty trucks routinely transport expensive equipment worth tens of thousands of dollars, navigate unpredictable job sites, and operate under tight schedules that pressure drivers to cut corners. Standard commercial auto policies were designed for delivery vans and service vehicles, not for the reality of construction operations. Construction companies across Washington, Oregon, and Alaska face risks that generic coverage simply doesn’t address.

A standard policy might cover your truck, but it won’t cover the $15,000 compressor in the bed or the $8,000 ladder rack bolted to the frame when they’re damaged in transit or stolen from a job site.

Equipment Theft and Damage Create Financial Exposure

Job sites attract theft. Construction equipment left unattended overnight, even on supposedly secure sites, disappears regularly. Tools, compressors, generators, and mounted equipment can represent 20 to 40 percent of a contractor’s total asset value. Without inland marine endorsements or tools and equipment coverage, you absorb those losses personally. A stolen welder or hydraulic pump forces you to either delay the next job or rent expensive replacement equipment-both outcomes cut into your margins immediately. Physical damage coverage for permanently attached equipment gives you the choice to cover items such as bolted tool boxes or ladder racks. A rollover on a wet road or a backing accident can total specialized truck bodies and attached tools in seconds. Standard commercial auto policies treat these items as afterthoughts, if they address them at all.

Liability Exposures Extend Beyond Simple Accidents

Construction work creates liability scenarios that don’t exist in other industries. Your driver hits another vehicle while hauling a load of lumber-that’s standard liability, covered. But what if the load shifts during transport and damages property on the roadside? What if faulty workmanship causes a building to leak months after your crew leaves, and the property owner sues? What if an employee operating a piece of equipment injures a third party on site? These situations require workers’ compensation, general liability, and sometimes errors and omissions coverage working together. Regulatory bodies in Washington, Oregon, and other states increasingly demand higher liability minimums for heavy-duty vehicles. Vehicles over 10,001 pounds GVWR typically require around $750,000 in bodily injury and property damage liability, compared to roughly $300,000 for lighter trucks.

Contract Requirements Drive Coverage Decisions

Many construction contracts now mandate additional insured status for general contractors, meaning your policy must explicitly cover their interests or you lose the job. One missed requirement can disqualify you from bidding on projects worth hundreds of thousands of dollars. Construction companies that understand these contractual obligations gain a competitive advantage-they can respond faster to bid requests and avoid delays caused by coverage disputes. The next section covers the specific coverage options that address these exposures and help you meet contract requirements without overpaying for unnecessary protection.

Coverage Options for Construction Fleet Vehicles

Commercial Auto Liability Forms Your Foundation

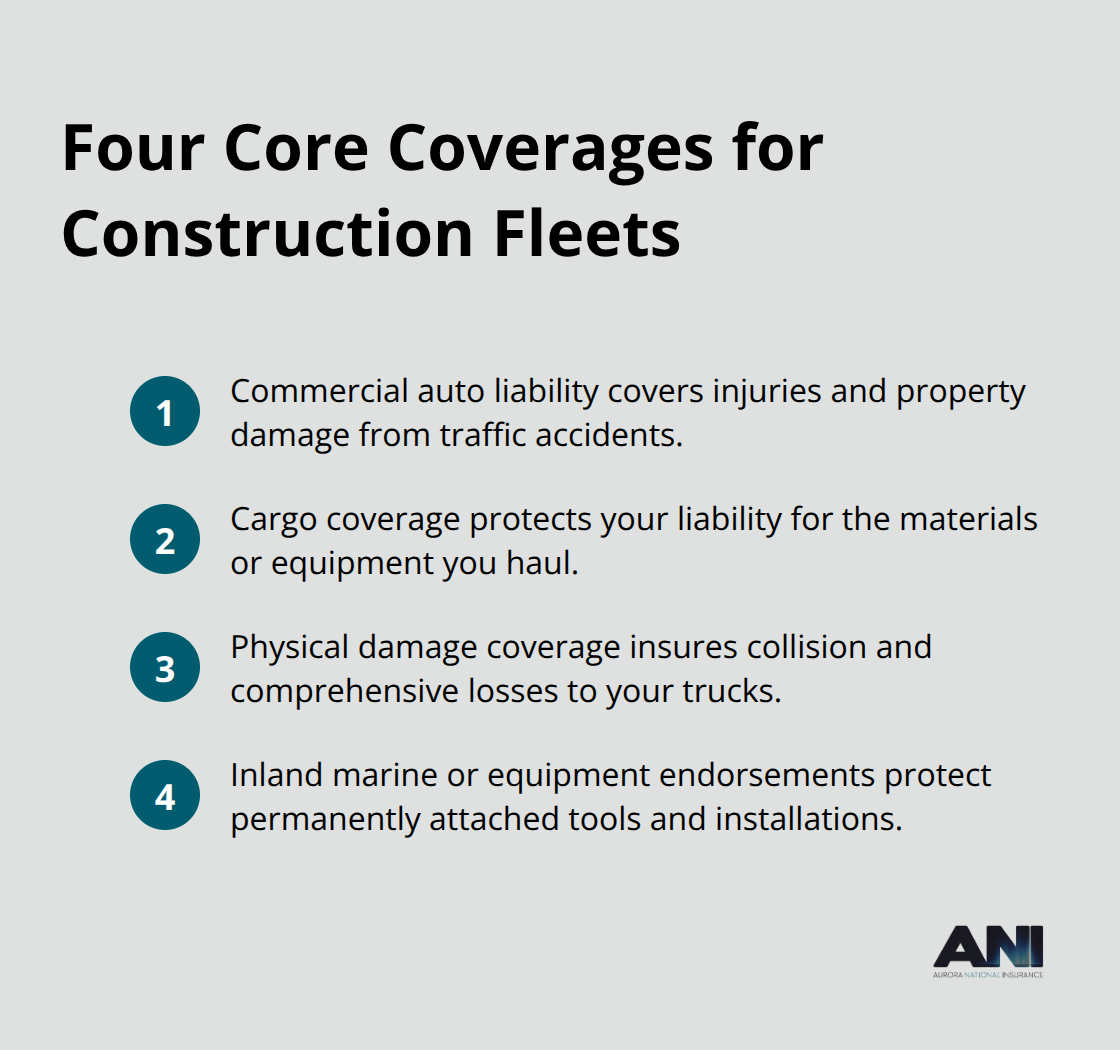

A construction fleet requires four core coverage types working together, not in isolation. Commercial auto liability protects you when your driver injures someone or damages property in a traffic accident, but it stops there-it won’t cover the equipment you’re hauling or the tools mounted on your truck. Bodily injury and property damage liability minimums for vehicles over 10,001 pounds GVWR sit around $750,000, roughly double the requirement for lighter commercial trucks.

This higher threshold exists because heavy-duty construction vehicles cause more severe accidents.

Cargo coverage becomes legally required when you haul materials or equipment, and the minimum amount depends on what your trucks carry. If you transport a $30,000 compressor and it gets damaged in transit, cargo coverage protects your liability if the cargo itself causes damage to another vehicle or property. Physical damage coverage for your vehicles themselves is optional but essential-it covers collision and comprehensive losses on trucks worth $50,000 to $200,000 or more.

Permanently Attached Equipment Needs Separate Protection

The real gap in standard commercial policies emerges with permanently attached equipment. A $12,000 hydraulic lift bolted to your truck bed, an $8,000 ladder rack, or a $15,000 custom tool storage system attached to the frame doesn’t get covered under standard auto physical damage. You need inland marine coverage or an equipment endorsement to protect these installations. Without it, a rollover or backing accident becomes your personal expense.

Hired and Non-Owned Vehicles Require Coverage Extension

Hired and non-owned vehicle coverage addresses a practical reality most construction companies face-your employees sometimes use their personal vehicles for work, or you rent trucks during peak seasons. This endorsement extends your liability coverage to employee-owned vehicles being used for business purposes and to vehicles you temporarily rent. The cost is minimal, typically adding 5 to 10 percent to your base premium, but the protection is substantial.

A crew member driving their personal pickup to pick up materials on your behalf creates liability exposure that standard policies exclude. Adding non-owned auto coverage prevents a single accident from becoming an uninsured claim that damages your business.

Heavy Equipment Transport and Fleet Yard Operations

Specialized endorsements for heavy equipment transport round out proper construction fleet protection. If you transport heavy machinery between job sites-excavators, loaders, or cranes-you need in-transit coverage that protects the equipment while being moved. This differs from equipment coverage at a stationary job site. Garagekeepers liability applies if you maintain a fleet yard or storage facility where you work on your own vehicles or temporarily store equipment. A fire in your maintenance facility could destroy multiple trucks and equipment simultaneously; standard commercial auto policies often exclude this scenario entirely.

Telematics Unlocks Real Premium Reductions

Telematics integration with your commercial auto policy has become a legitimate cost-reduction tool. Carriers increasingly offer usage-based pricing that monitors actual driver behavior, speed, harsh braking, and distracted driving patterns. Construction fleets that implement telematics typically see 10 to 15 percent premium reductions within the first year if driver behavior scores remain clean. This isn’t theoretical-it’s how modern fleet underwriting works across the industry. The next section explores how fleet maintenance programs, driver training, and ongoing risk management strategies lower your total cost of ownership while protecting your assets.

How to Cut Fleet Insurance Costs Without Cutting Corners

Reducing your construction fleet insurance premiums doesn’t mean accepting lower coverage or ignoring maintenance problems until they become catastrophic. Strategic risk management directly lowers what carriers charge you. The carriers backing construction fleets track three specific data points that determine your renewal rate: vehicle maintenance records, driver safety performance, and real-time operational metrics from telematics systems. Construction companies that actively manage these three areas see measurable premium reductions, not theoretical ones.

Maintenance Records Prove You Prevent Claims

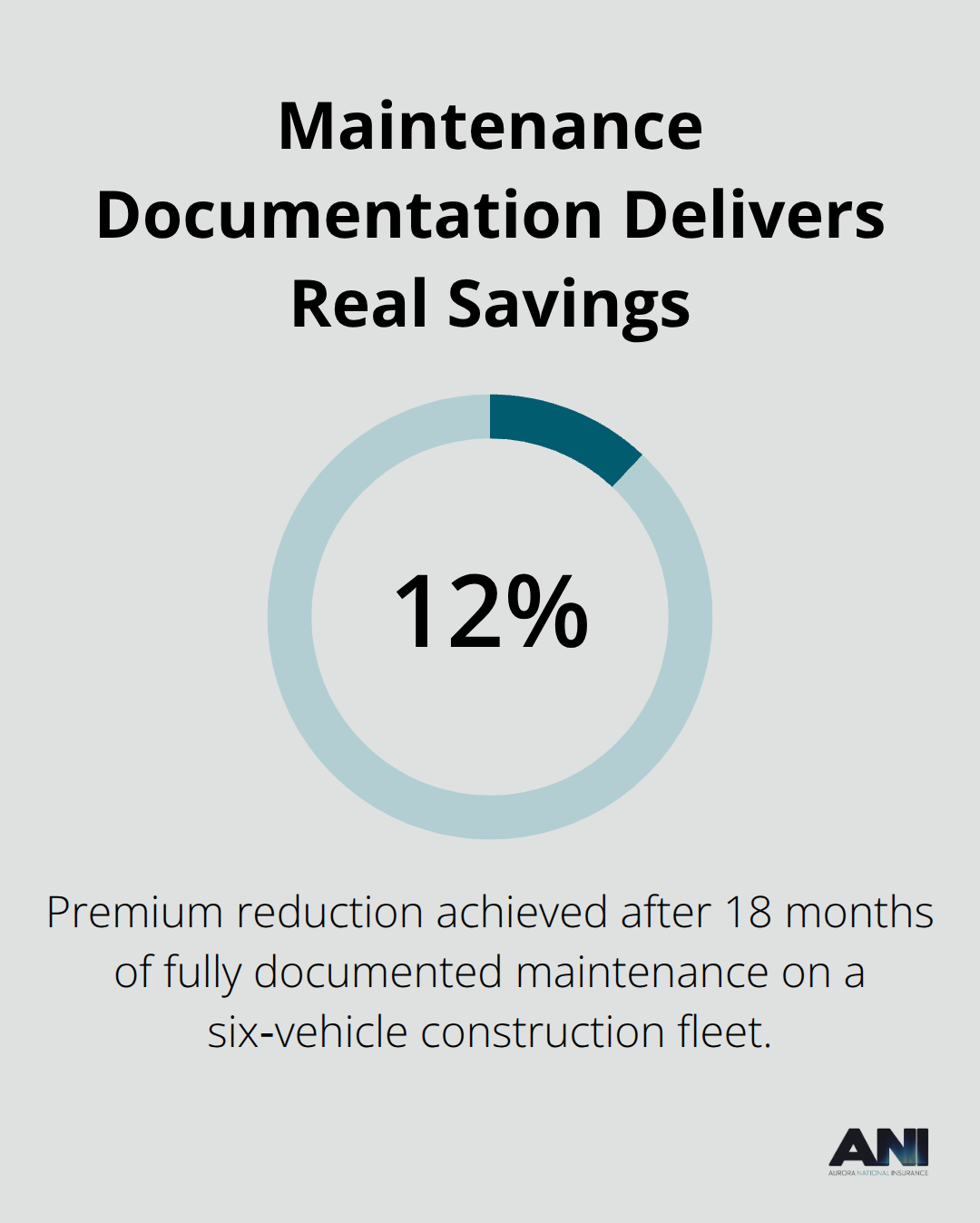

Carriers now request detailed maintenance logs before quoting heavy-duty construction fleets. A truck with documented oil changes every 5,000 miles, regular brake inspections, and tire replacements at manufacturer specifications tells underwriters you’re serious about preventing mechanical failures that cause accidents. Construction vehicles operating in harsh conditions-rough job sites, heavy loads, extended hours-accumulate wear faster than standard commercial trucks. One contractor operating a six-vehicle fleet in Portland documented every maintenance visit for eighteen months and received a 12 percent premium reduction at renewal because the data showed proactive prevention rather than reactive repairs.

Spotty or nonexistent maintenance records signal the opposite message. Carriers view that as evidence you’ll eventually have a breakdown-related accident, and they price accordingly. Establish a maintenance schedule aligned with manufacturer recommendations for your specific vehicle types and document everything. Digital maintenance platforms like Samsara or Verizon Connect now integrate with fleet telematics, so your maintenance records automatically sync with the same system tracking driver behavior.

Driver Training Addresses the Root Cause of Claims

Construction fleets experience higher accident rates than general commercial fleets because job-site pressure creates rushed driving. Drivers hurrying between sites to meet schedules take risks they otherwise wouldn’t. A formal driver training program that addresses construction-specific hazards-backing onto tight job sites, securing loads properly, managing fatigue during long shifts-shows carriers you’ve identified the actual problem and implemented solutions.

Contractors who completed DOT compliance training programs and defensive driving courses for their teams reported accident reductions over twelve months. Those accident reductions directly translate to lower premiums because carriers experience fewer claims from your fleet. Training should happen annually, not as a one-time onboarding event. New drivers in construction need specific instruction on load securement, backing procedures for unfamiliar sites, and how to handle equipment transport without damaging cargo or other vehicles. A single preventable accident can increase your renewal premium by 20 to 30 percent for that driver’s vehicle class.

Telematics Data Gives You Negotiating Power

Telematics systems now provide the concrete data carriers need to justify premium reductions. When your fleet demonstrates clean scores across speed compliance, smooth acceleration and braking, and minimal harsh maneuvers over a three-month period, carriers have objective evidence you operate safely. Construction fleets implementing telematics typically qualify for discounts within the first year if safety metrics remain strong.

The data also reveals which drivers need additional coaching and which vehicles have mechanical issues causing poor performance. A telematics system showing one truck consistently hard-braking might indicate worn brakes needing replacement-fixing that mechanical problem prevents an accident and keeps your safety scores high. Carriers increasingly tie renewal pricing directly to telematics performance data rather than relying solely on claims history from previous years. This shift favors construction companies willing to invest in monitoring technology because they can prove current safety performance rather than arguing about past accidents.

Final Thoughts

Construction company auto insurance protects far more than your vehicles-it protects your ability to operate profitably and meet contractual obligations. The coverage gaps we’ve outlined throughout this guide represent real financial exposure that standard commercial policies ignore. Heavy-duty fleets face equipment theft, liability scenarios unique to job sites, and regulatory requirements that demand specialized protection.

The strategies we’ve covered-maintenance documentation, driver training, and telematics integration-work because they address what carriers actually measure when pricing your renewal. Construction companies that implement these approaches see measurable premium reductions while simultaneously reducing accident frequency and equipment losses. This approach delivers both cost savings and stronger protection for your fleet.

Our licensed agents at Aurora National Insurance compare coverage options from multiple top-rated carriers to find the protection that matches your specific operations and budget. Contact us today to discuss your actual fleet operations and identify gaps in your existing coverage.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.