Alaska company auto insurance: Tailored Solutions For Your Business Vehicles

Running a business in Alaska means dealing with weather, terrain, and distances that most other states don’t face. Your vehicles need protection that goes beyond standard coverage.

At Aurora National Insurance, we understand that Alaska company auto insurance requires more than a one-size-fits-all approach. This guide walks you through the specialized coverage options your business vehicles actually need, how to compare providers, and what to look for when choosing the right partner for your fleet.

Why Alaska’s Harsh Conditions Demand Real Coverage Solutions

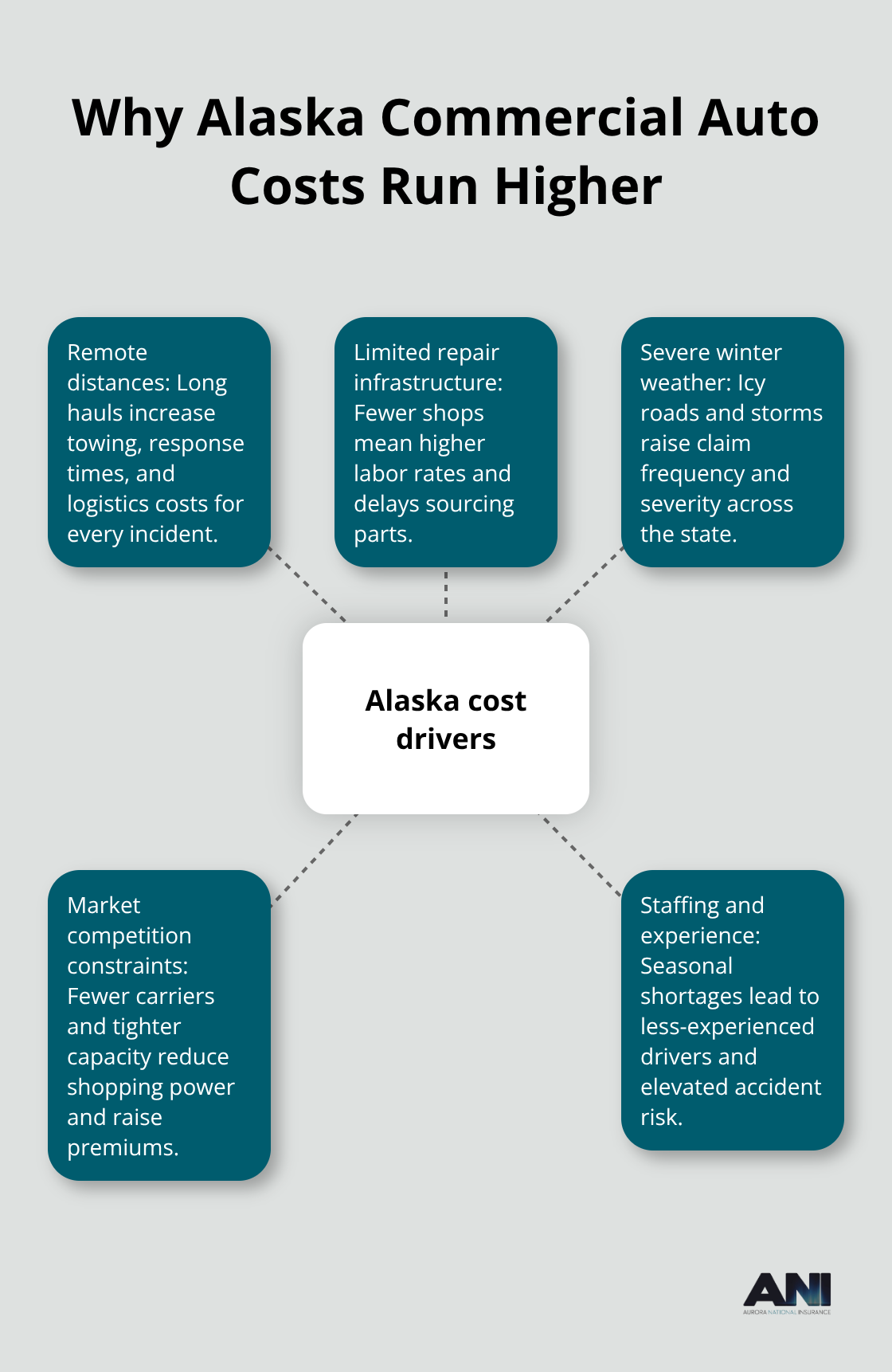

Alaska’s driving environment stands apart from the rest of the nation, and standard commercial auto insurance simply doesn’t account for the actual risks your fleet faces. Interior roads freeze solid for months, creating conditions where accidents happen faster and with more severity than in temperate climates. Anchorage and Fairbanks see winter temperatures that regularly dip below minus 20 degrees, turning routine drives into high-risk operations. Your vehicles contend with black ice, whiteout conditions, and roads that deteriorate rapidly under freeze-thaw cycles. A food truck operating in Anchorage faces different exposure than one in Seattle. A contractor hauling equipment across remote Alaska routes encounters hazards that don’t exist on interstate highways in the lower 48 states. This isn’t about caution-it’s about recognizing that Alaska businesses operate in conditions that directly increase accident frequency and severity. Standard policies written for national exposure miss these specifics entirely.

Geography Creates Real Coverage Gaps

Remote locations in Alaska mean your vehicles spend hours or days far from immediate help. When a service van breaks down 200 miles from Anchorage, a simple mechanical failure becomes an operational crisis. Coverage gaps become catastrophic in remote areas because recovery costs escalate dramatically. Towing services charge premium rates for long-distance work, and parts availability forces extended downtime. Alaska’s minimum liability requirements include $25,000 bodily injury liability per person, $50,000 bodily injury liability per accident, and $25,000 property damage liability per accident, rarely reflecting the actual financial exposure your business faces when operating across the state. A contractor working in rural Alaska should carry limits well above minimums because a serious accident with multiple injuries or significant property damage can exceed standard coverage within moments. Assessing your specific routes and operations helps determine whether minimums provide adequate protection or whether higher limits make financial sense for your operation.

Regulatory Compliance Isn’t Optional

Alaska requires commercial auto insurance for any business vehicle, and the state enforces these requirements seriously. Non-compliance brings fines, vehicle registration suspension, and potential business shutdown. If your operation involves for-hire services (whether livery, delivery, or transport), commercial auto becomes mandatory rather than optional. Heavy trucks and owner-operator rigs face additional FMCSA and USDOT safety regulations that directly tie to insurance coverage and compliance. Driving history matters significantly in Alaska because insurers review motor vehicle reports for all drivers accessing business vehicles, typically examining the past three years of records. A single driver with violations can meaningfully increase premiums across your entire fleet. The regulatory framework exists because Alaska’s conditions create genuine risk, and carriers price accordingly.

What Happens When You Operate Without Proper Coverage

Many Alaska business owners underestimate the financial consequences of inadequate coverage. A single accident involving multiple vehicles or serious injuries can quickly exceed your policy limits, leaving your business liable for the difference. Workers in remote areas face longer recovery times and higher medical costs, which standard minimums don’t adequately address. Equipment-heavy operations (food trucks with attached gear, contractors carrying tools) need coverage that protects both the vehicle and its contents. Your employees represent another exposure-if they operate company vehicles, their actions create liability that extends directly to your business. Understanding these real-world scenarios helps you make informed decisions about coverage levels rather than simply purchasing the cheapest option available.

Finding Coverage That Matches Your Actual Operations

The right commercial auto policy reflects how your business actually operates, not how insurers assume it operates. A landscaper with multiple crews working different sites faces different risks than a consultant who occasionally drives to client meetings. A snow plow service operating during winter months encounters seasonal exposure that standard policies may not adequately address. Your vehicle types, driver profiles, annual mileage, and service areas all influence both your actual risk and your premium costs. Comparing quotes from multiple carriers reveals how different insurers evaluate Alaska-specific exposures and price accordingly. An independent agency with local Alaska expertise can help you navigate these distinctions and identify coverage gaps before they become costly problems.

Coverage That Protects Your Alaska Fleet

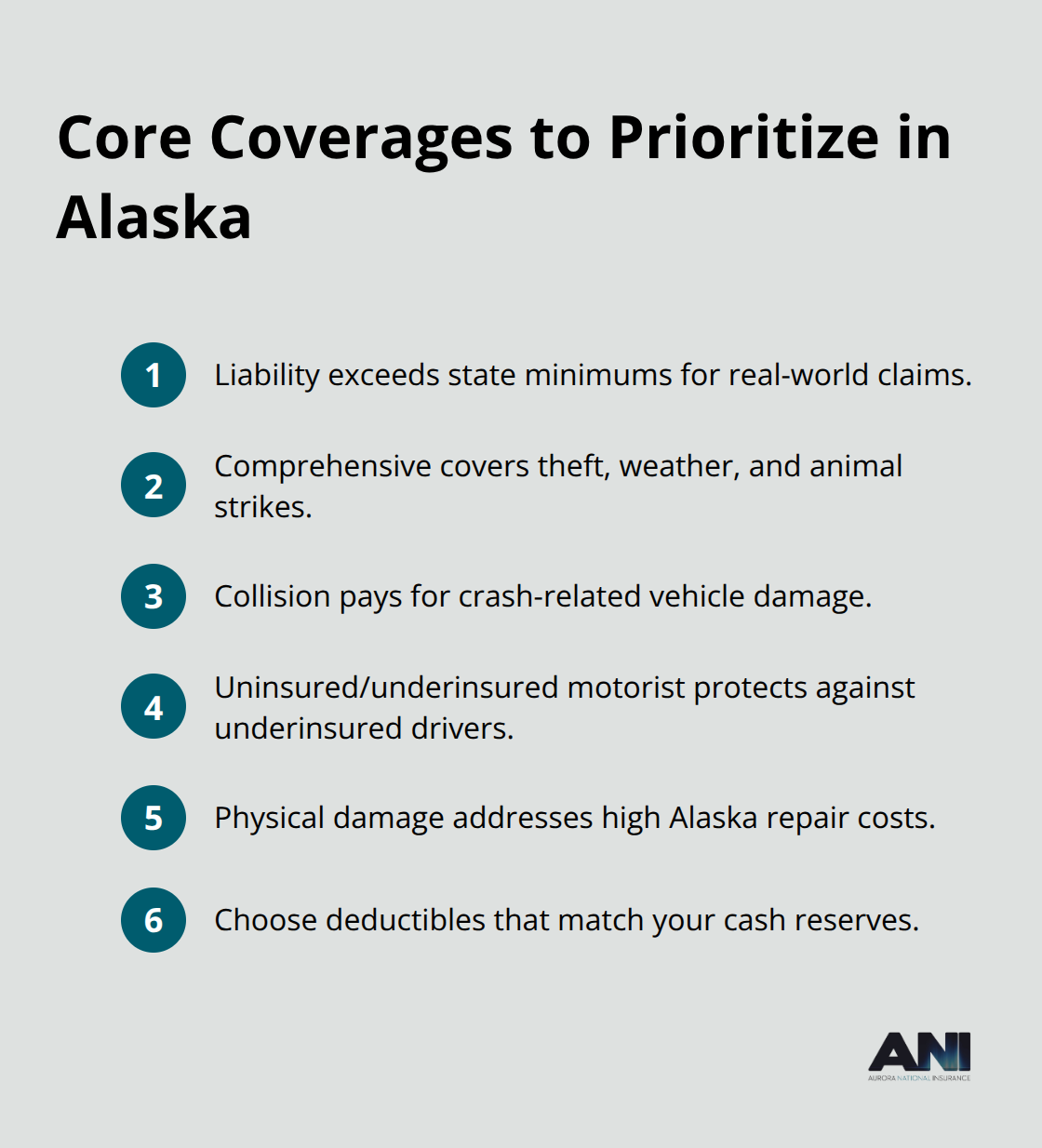

Liability Coverage Forms Your Foundation

Liability coverage forms the foundation of any Alaska commercial auto policy, and the state’s minimum requirements represent a floor, not a ceiling. Alaska’s minimum liability requirements include $50,000 per person and $100,000 per accident for bodily injury liability, plus $25,000 for property damage per incident. These minimums exist because they theoretically cover basic scenarios, but Alaska’s accident severity and medical costs regularly exceed these thresholds. A contractor involved in a multi-vehicle collision on an icy road faces medical bills exceeding $100,000 within hours. Progressive, the nation’s number one commercial auto insurer, reports that businesses operating in high-risk environments typically carry liability limits of at least $300,000 per accident to adequately protect against realistic exposure.

Your actual limits should reflect your vehicle types, the value of equipment you transport, and your annual mileage across Alaska’s network. A food truck with $50,000 in attached cooking equipment needs different coverage than a consultant’s sedan. Higher limits cost more monthly, but they prevent catastrophic financial exposure when serious accidents occur.

Physical Damage Coverage Addresses Alaska-Specific Risks

Physical damage coverage-both collision and comprehensive-protects your vehicles from Alaska-specific perils. Collision covers damage from accidents with other vehicles or objects. Comprehensive covers theft, vandalism, weather damage, and wildlife strikes, which occur at higher rates in remote Alaska locations. Choosing appropriate deductibles matters significantly; a $500 deductible costs less monthly but creates larger out-of-pocket expenses when incidents occur. Many Alaska businesses find $1,000 deductibles strike the right balance between manageable premiums and reasonable risk retention.

Remote operations increase the likelihood of comprehensive claims. A vehicle parked overnight in a rural area faces higher theft risk than one in an Anchorage lot. Winter weather causes collision damage at rates far exceeding national averages.

Medical Payments and Uninsured Motorist Protection

Medical payments coverage and uninsured motorist protection address the reality that not every driver on Alaska roads carries adequate insurance. Medical payments coverage pays treatment costs for you and your employees regardless of fault, which matters when your crew operates far from major medical facilities and requires emergency transport. Uninsured motorist coverage protects your business when another driver causes an accident but lacks sufficient insurance.

Alaska’s remote areas include drivers operating without adequate coverage, making this protection essential rather than optional. Your employees represent another exposure-if they operate company vehicles, their actions create liability that extends directly to your business.

Workers’ Compensation and Commercial Auto Work Together

Workers’ compensation requirements apply whenever employees operate company vehicles, and standard commercial auto policies do not replace workers’ comp. Your commercial auto policy covers liability to third parties; workers’ compensation covers your employees’ medical expenses and lost wages from work-related injuries. These operate as separate systems, and both matter for complete protection.

Specialized Endorsements for Your Operations

For fleet operations, additional endorsements address specific exposures. If your business uses vehicles to transport customer property or equipment, garagekeepers liability coverage protects against damage to items in your care. Food truck operations need coverage for attached equipment and refrigeration systems, which standard policies may not fully cover. Heavy trucks and tow trucks require specialized coverage for on-hook liability when hauling cargo or disabled vehicles.

An independent Alaska agency can review your specific operations and identify which endorsements apply to your business rather than purchasing unnecessary add-ons or discovering gaps after an accident occurs. The next chapter walks you through comparing providers and selecting the partner that understands your actual operations.

Picking the Right Insurance Partner for Your Alaska Fleet

Compare Quotes Across Multiple Carriers

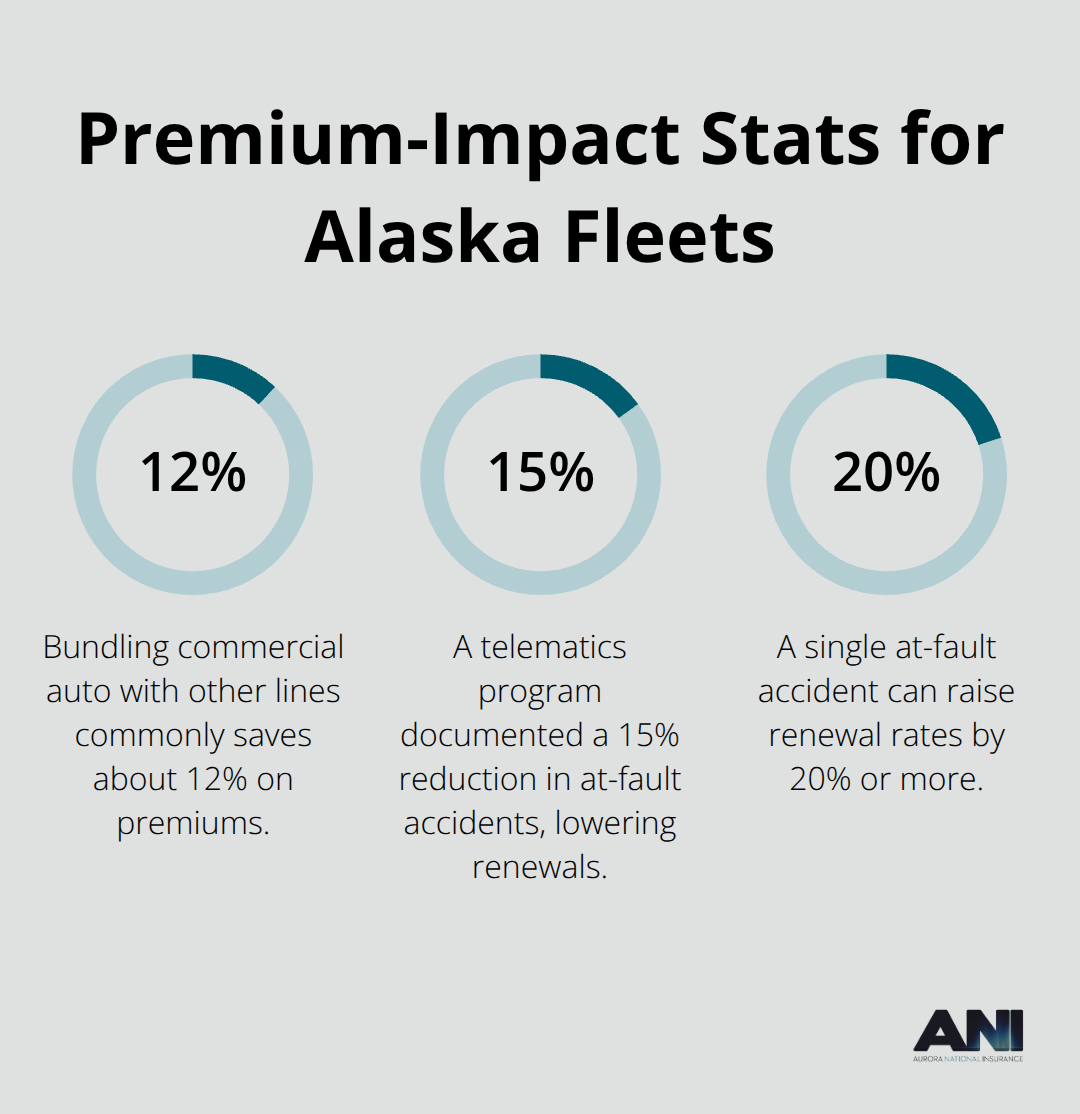

Multiple quotes from different carriers reveal how dramatically insurance costs and coverage options vary for Alaska operations. When you request quotes, provide detailed information about your actual operations: vehicle types, annual mileage, service areas, driver histories, and the specific work your fleet performs. A contractor hauling equipment across interior Alaska receives vastly different quotes than a delivery service operating primarily in Anchorage, and comparing apples to apples requires consistent information across all quotes. Comparing multiple quotes helps you identify the best value for your specific situation.

The lowest quote doesn’t automatically represent the best value. A cheap policy with significant coverage gaps creates false economy when an accident exposes your business to uninsured losses. Request quotes that include comparable coverage levels and deductibles so you can evaluate actual price differences rather than comparing fundamentally different policies.

Prioritize Local Alaska Expertise

Local Alaska agencies understand regional risk factors that national carriers often miss or price incorrectly. An agency with boots on the ground in Anchorage, Fairbanks, or Mat-Su Valley recognizes that winter driving conditions create seasonal exposure peaks, that remote operations require different claim support than urban routes, and that specific industries dominate Alaska’s economy. When evaluating any provider, ask directly about their claims support in remote areas-how quickly they dispatch adjusters, what resources exist for vehicle recovery in areas far from major cities, and what happens when your business operates during winter weather emergencies.

Aurora National Insurance, an independent Anchorage-based agency rooted in Alaska, leverages local expertise to help clients navigate these distinctions and identify coverage that matches their actual operations rather than generic assumptions. Representing multiple top-rated carriers, their licensed agents deliver tailored comparisons and responsive service to help you find the right protection at competitive prices.

Verify Financial Strength and Claims Infrastructure

Financial stability matters equally when selecting an insurance partner. Check ratings from AM Best or Standard & Poor’s to confirm your carrier has the financial strength to pay claims when serious accidents occur. A carrier with strong ratings and robust Alaska claims infrastructure costs more upfront but prevents the nightmare scenario where your business suffers a major loss and discovers your insurer lacks the resources to respond effectively.

Ask potential carriers about their specific experience handling claims in remote Alaska locations. Response times matter significantly when your vehicle sits disabled hundreds of miles from the nearest service center. Carriers with established relationships with Alaska towing companies, repair shops, and medical providers can mobilize support faster than those treating Alaska as a secondary market.

Evaluate Coverage Options for Your Specific Operations

Different Alaska businesses need different coverage structures. A food truck operation with attached equipment requires endorsements that a consultant’s sedan doesn’t need. A snow plow service operating seasonally faces different exposure than a year-round delivery fleet. Heavy trucks and tow trucks require specialized coverage for on-hook liability when hauling cargo or disabled vehicles.

An independent Alaska agency can review your specific operations and identify which endorsements apply to your business rather than purchasing unnecessary add-ons or discovering gaps after an accident occurs. This tailored approach prevents both overpaying for irrelevant coverage and underinsuring critical exposures that matter to your actual operations.

Final Thoughts

Alaska company auto insurance demands a fundamentally different approach than coverage designed for the lower 48 states. Your business operates in conditions that create genuine, measurable risk-harsh winters, remote locations, regulatory complexity, and accident severity that far exceeds national averages. Standard policies written for national exposure miss these specifics entirely, leaving your fleet and your business financially exposed when accidents occur. The right coverage reflects how your business actually operates, whether you run a food truck with attached equipment, a contractor hauling tools across interior Alaska, or a delivery service operating primarily in Anchorage.

Comparing quotes from multiple carriers reveals how dramatically costs and coverage options vary for your specific situation. Prioritize providers with local Alaska expertise who understand seasonal exposure peaks, remote area claims support, and the industries that dominate your state’s economy. Verify financial strength through AM Best or Standard & Poor’s ratings to confirm your carrier can pay claims when serious accidents occur. Your liability limits should exceed Alaska’s minimums because realistic accident scenarios regularly exceed $100,000 in damages.

Your policy requires regular review as your business grows and your vehicle fleet changes. When you add vehicles, hire new drivers, or enter new service areas, contact your insurance provider immediately rather than discovering gaps after an accident. Aurora National Insurance brings local Anchorage-based expertise to help you navigate these distinctions, with licensed agents representing multiple top-rated carriers who deliver tailored comparisons so you find the right protection at competitive prices.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.