Small Business Auto Insurance: Affordable Solutions for Your Fleet

Running a business fleet comes with real costs and real risks. Vehicle accidents, liability claims, and uninsured losses can drain your budget fast.

Small business auto insurance protects your company from these financial hits while keeping you compliant with state laws. At Aurora National Insurance, we help business owners find coverage that fits their fleet size and budget without overpaying for protection they don’t need.

Why Your Business Needs Commercial Auto Insurance

State Law Requires It-And the Penalties Are Severe

State law requires commercial auto insurance if you operate any vehicle for business purposes. This requirement exists for a reason: accidents happen, and someone must pay for the damage. If you cause an accident while driving an uninsured business vehicle, you face personal liability that can exceed hundreds of thousands of dollars. Your personal assets, home, and business income become targets if you’re underinsured or uninsured.

Personal Auto Policies Leave You Completely Exposed

A personal auto policy won’t cover business use-insurers specifically exclude commercial activities. This means you have zero protection the moment you use your vehicle to visit clients, make deliveries, or transport equipment for work. The moment you cross that line from personal to business use, your personal policy becomes worthless. You drive uninsured, whether you realize it or not.

The Real Cost of an Accident Without Coverage

The financial impact of an accident without proper coverage hits immediately and lasts for years. A minor fender-bender with injuries costs $50,000 to $100,000 in medical claims and vehicle damage. A serious collision involving multiple vehicles or permanent injury easily exceeds $1 million. Small business owners typically pay between $200 and $400 monthly for commercial auto coverage-a fraction of what a single accident costs.

What Commercial Auto Insurance Actually Covers

Commercial policies cover liability when you’re liable for damages, physical damage to your own vehicles, medical payments for injured parties, and uninsured motorist protection. Personal policies explicitly exclude all business use, leaving you exposed. The difference between commercial auto insurance and personal auto insurance is critical: one protects your business, the other leaves it vulnerable.

Understanding Your Fleet’s Specific Risks

Different fleets face different risks. A delivery service with multiple drivers on the road daily faces higher exposure than a contractor who occasionally uses a truck for site visits. Your vehicle types matter too-cargo vans and pickup trucks carry different risk profiles than sedans. The coverage you need depends entirely on how you operate. Choosing the right commercial auto coverage requires understanding exactly what risks your fleet faces and what protection actually covers those risks.

How to Pick the Right Coverage for Your Fleet

Match Coverage to Your Operations

Choosing commercial auto insurance requires matching coverage to how your business actually operates, not picking the cheapest quote. Start by listing every vehicle you own or lease for business purposes, then note the vehicle type-sedans cost far less to insure than cargo vans or pickup trucks. According to industry data, sedans run $130–$185 monthly while cargo vans range $160–$265 and pickup trucks $210–$340. Your location matters significantly too; Florida averages $412 monthly while California averages $154 for the same coverage, reflecting state-specific accident rates and repair costs.

Assess Your Drivers and Risk Profile

Next, count your drivers and pull their motor vehicle records. A driver with multiple violations or recent accidents can double your premium, while a clean record keeps costs down. Small businesses with 1–4 vehicles typically pay $200–$400 monthly total, though construction contractors and high-risk trades average $264–$299 monthly because their work exposes vehicles to greater damage. Once you know your fleet composition, compare coverage limits across quotes-this step stops you from accidentally comparing apples to oranges.

Determine Your Coverage Limits

Most contractors need $1 million per occurrence liability with $2 million aggregate, but verify what your client contracts actually require before binding coverage. Hired and non-owned auto coverage costs under $50 monthly in most states and protects you when employees use personal vehicles or when you lease equipment temporarily, making it a practical addition for growing fleets.

Shop Multiple Carriers and Bundle Policies

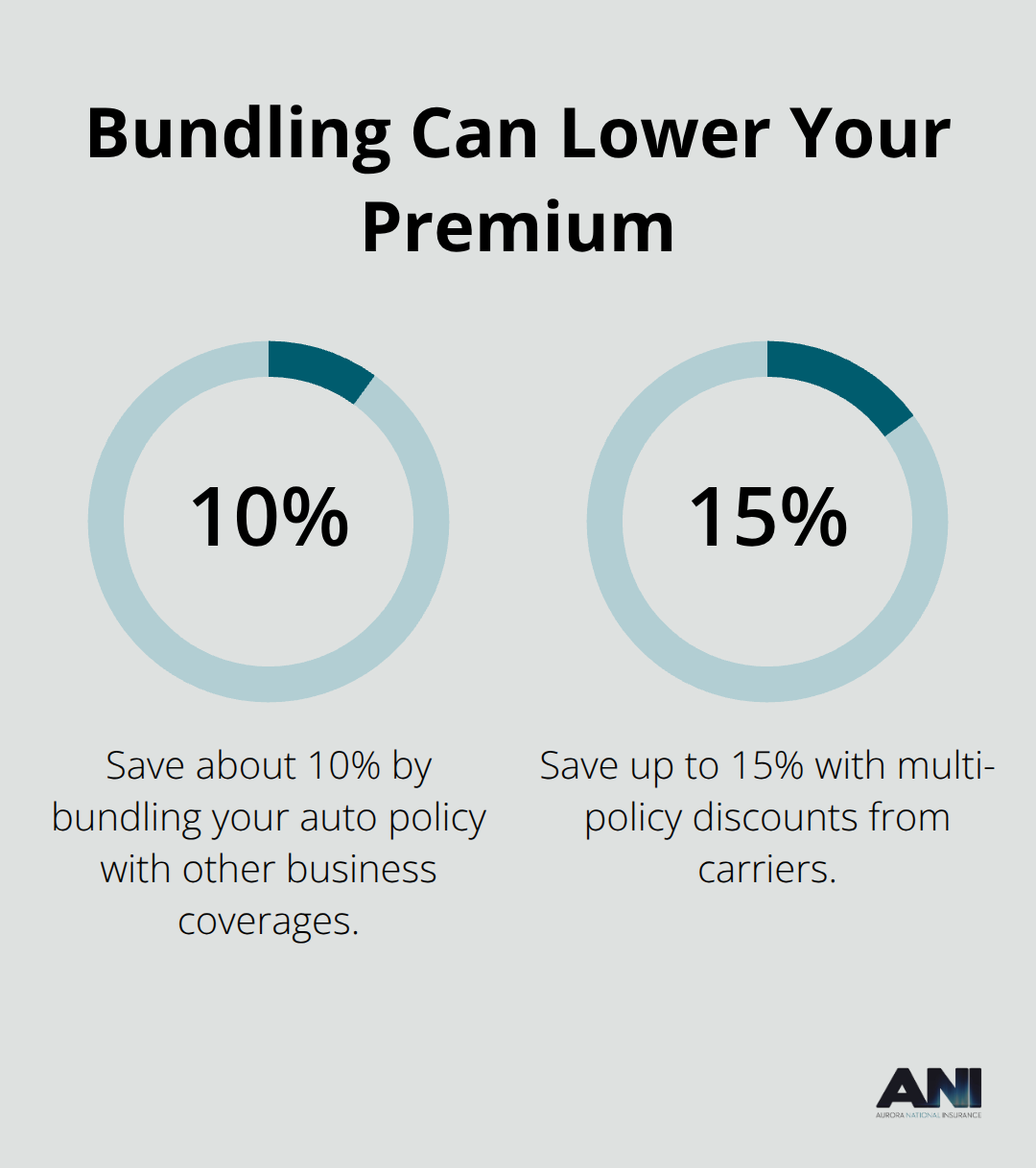

Finding competitive rates demands shopping multiple carriers rather than accepting the first quote. Progressive can issue a certificate of insurance in 15 minutes, ERGO NEXT provides instant online COIs, and BiBERK completes quotes in under 10 minutes-all critical when you need coverage fast for a new client contract. Bundling auto insurance with general liability and inland marine coverage typically saves 10–15% compared to buying policies separately, so always ask carriers about multi-policy discounts. Request quotes from at least three carriers because rate differences for identical coverage regularly exceed $100 monthly.

Optimize Rates Through Safety and Monitoring

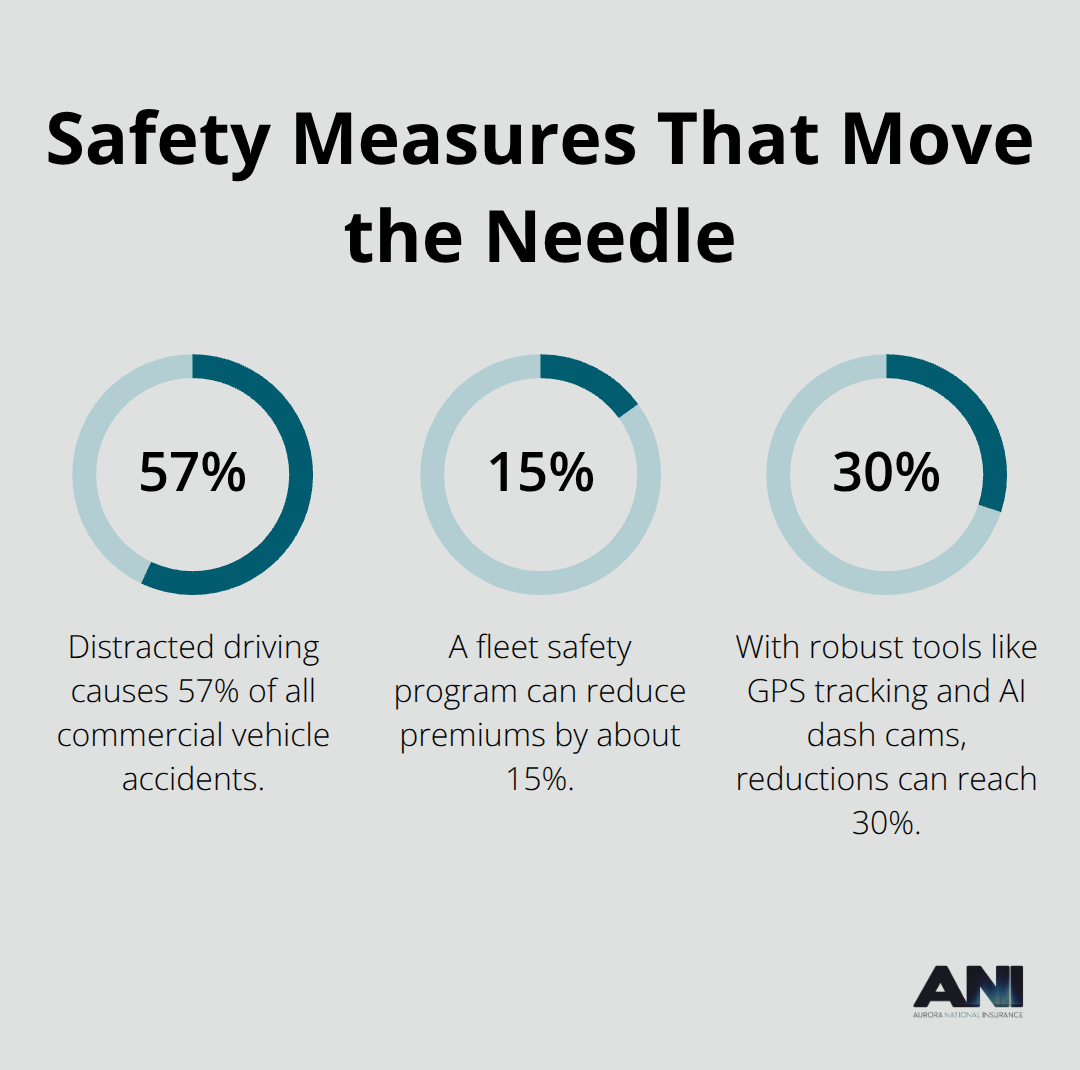

When comparing quotes, ensure deductibles are identical; a $1,000 deductible costs less than a $500 deductible but shifts more risk to your business when accidents occur. Vehicle type affects pricing dramatically, so don’t mix quotes for different vehicle lists. Implementing a fleet safety program directly affects your commercial auto insurance premiums and claims, often qualifying you for discounts that offset the program investment within months. Telematics systems that monitor driver behavior and vehicle performance further reduce premiums while protecting your business from distracted driving claims, which cause 57% of all commercial vehicle accidents according to industry data. Review your motor vehicle records annually and remove high-risk drivers from your policy or require additional training, since your loss history directly determines your future rates and insurability. These steps position your fleet for better coverage options and lower costs as your business grows.

How to Actually Cut Your Fleet Insurance Costs

Bundle Policies to Slash Your Total Premium

Combining your auto policy with general liability and inland marine coverage cuts 10–15% from your total premium compared to buying policies separately. This isn’t theoretical savings-carriers reward customers who consolidate their business insurance. When you shop for quotes, ask each carrier about multi-policy discounts before comparing final prices. Some carriers build the discount into their quote automatically while others require you to request it, so don’t assume the cheapest single-policy quote beats a bundled rate from another carrier. A $150 monthly auto policy bundled with general liability might cost $280 total, while buying them separately runs $320. That $40 monthly difference adds up to $480 annually with no change to your coverage.

Implement Safety Programs That Carriers Reward

Safety programs directly reduce your premiums because they reduce your claims. A fleet safety program can help reduce your premiums by 15-30% with tools like GPS tracking and AI dash cams. Distracted driving causes 57% of all commercial vehicle accidents, so establish a clear policy against mobile device use while driving and address your biggest risk. Telematics systems track driver behavior and vehicle performance, qualify you for additional discounts, and provide real data on which drivers create risk.

Pull motor vehicle records for every driver annually and remove anyone with recent violations or multiple at-fault accidents, since your loss history determines your future insurability and rates.

Maintain Clean Records and Document Your Efforts

Carriers review your claims history carefully; three years of clean driving records with no accidents positions you for better quotes than a fleet with claims on file. Regular vehicle maintenance prevents breakdowns that lead to rushed decisions and accidents, so establish a maintenance schedule and document completion. Track your fleet’s safety metrics-miles driven, accidents, near-misses, and training completion-because this documentation proves to underwriters that you take risk seriously and qualify for preferred rates. When you renew your policy, provide this safety data to your carrier; it often justifies lower rates or retention with a carrier that might otherwise drop you due to industry-wide claims challenges.

Final Thoughts

Small business auto insurance protects your fleet from financial devastation while keeping you legally compliant. A single accident without proper coverage costs $50,000 to over $1 million, wiping out years of profit. Affordable coverage exists for every fleet size and budget, and you can move fast when you need it-Progressive issues certificates of insurance in 15 minutes, ERGO NEXT provides instant online quotes, and BiBERK completes quotes in under 10 minutes.

List your vehicles, note their types and locations, pull your drivers’ motor vehicle records, and determine what coverage limits your client contracts require. Request quotes from at least three carriers because rate differences for identical coverage regularly exceed $100 monthly. When comparing quotes, match deductibles and coverage limits exactly across all options, then bundle your auto policy with general liability and inland marine coverage to save 10–15% compared to buying policies separately.

Implement a fleet safety program and telematics monitoring to qualify for additional discounts while reducing your actual accident risk. Pull motor vehicle records annually and remove high-risk drivers, since your loss history directly determines your future rates and insurability. We at Aurora National Insurance help business owners find small business auto insurance that fits their fleet and budget-visit us today for instant online quotes and expert guidance tailored to your operation.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.