Alaska Condo Insurance Quotes: Is a Condo Policy Right for You?

Condo ownership in Alaska comes with unique insurance needs that standard homeowners policies simply don’t address. Your HOA insurance covers the building structure, but it leaves significant gaps in personal protection.

At Aurora National Insurance, we help condo owners understand why getting accurate Alaska condo insurance quotes matters. The right policy protects your belongings, covers your liability, and shields you from unexpected HOA assessments.

Why Your HOA Insurance Leaves You Exposed

Your HOA master policy covers the building structure and common areas, but it explicitly excludes what’s inside your unit. This creates a dangerous gap that many condo owners don’t realize until after a loss occurs. The master policy pays for damage to exterior walls, the roof, hallways, and shared spaces-not your kitchen cabinets, flooring, furniture, or personal belongings. In Alaska, where winter damage from frozen pipes and ice dams is common, this distinction matters enormously. If a pipe bursts in your unit and damages your hardwood floors and belongings, the HOA policy won’t cover any of it. You’re responsible for everything within your four walls, which is why a separate condo insurance policy is not optional-it’s essential.

The Real Cost of the HOA Deductible

When a covered loss affects common areas, the HOA master policy deductible gets split among all unit owners. Loss assessment coverage, an optional add-on to your condo policy, protects you from these surprise assessments. Without it, you could face unexpected bills that strain your finances. Many Alaska condo owners overlook this coverage entirely, then face assessments they can’t afford. The cost to add loss assessment coverage is minimal compared to the financial protection it provides when the HOA needs to cover a deductible or fund repairs to common areas.

Liability in Shared Living Spaces

Personal liability exposure in a condo is higher than in a single-family home because guests and neighbors live in closer proximity. If a visitor slips on your icy balcony or gets injured inside your unit, they can sue you for medical bills and damages. The HOA master policy doesn’t cover your personal liability-only liability for common areas. Your condo policy provides personal liability coverage that protects you if you or a household member cause injury to others or damage to their property. Standard limits are typically $100,000 to $300,000, but given Alaska’s legal environment and rising medical costs, higher limits are worth considering. Medical payments coverage, included in most condo policies, covers guest injuries regardless of fault, preventing small incidents from becoming costly disputes.

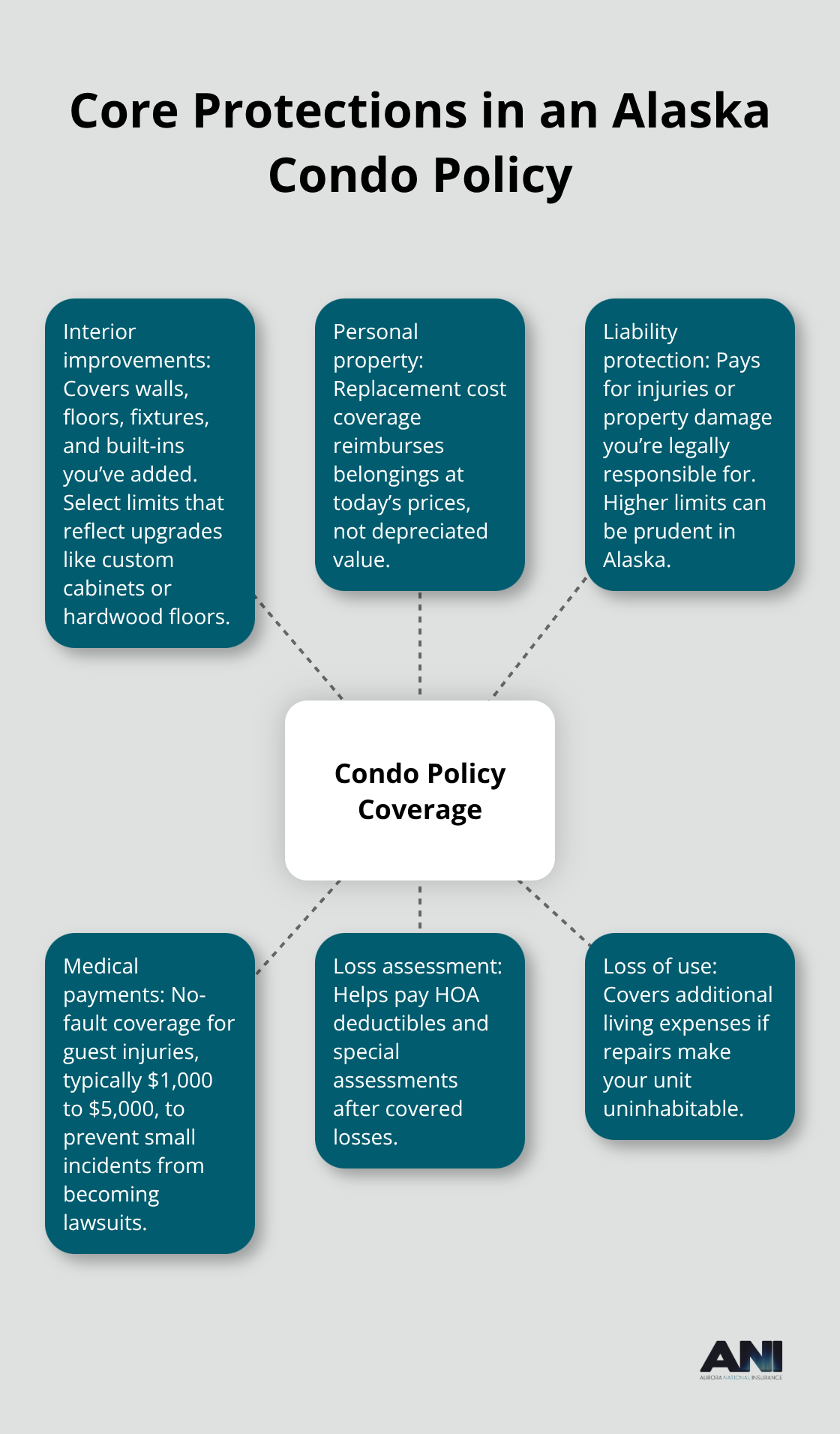

What Your Condo Policy Actually Protects

Your condo insurance covers interior walls, fixtures, and personal belongings that the HOA policy ignores. This includes your furniture, clothing, electronics, and permanently attached improvements like cabinets and appliances. If fire, theft, or water damage strikes your unit, your condo policy reimburses you for replacement costs (assuming you select replacement cost coverage rather than actual cash value). Loss of use coverage also reimburses your additional living expenses if you cannot occupy your unit while repairs happen. These protections fill the gaps that the HOA master policy leaves open, giving you complete coverage for everything you own and control within your unit.

Understanding Your Ownership Boundaries

The line between what the HOA covers and what you cover depends on your condo association’s bylaws and master policy. Most associations state that owners are responsible for everything inside the unit, including permanently attached fixtures and improvements. You need to review your HOA agreement to understand exactly where the association’s responsibility ends and yours begins. This clarity prevents coverage gaps and helps you select appropriate policy limits when you shop for quotes. The master policy deductible and the association’s potential assessments also influence how much loss assessment coverage you should carry, making this review step essential before you request quotes from carriers.

What Your Condo Policy Actually Covers

Interior Improvements and Personal Belongings

Your condo policy protects three critical areas that the HOA master policy ignores: your interior improvements, your personal belongings, and your liability exposure. A traditional condo insurance policy will cover damages to interior improvements, walls, floors and ceiling coverings, as well as your personal belongings. If you’ve upgraded your kitchen with custom cabinets or installed hardwood floors, these improvements receive coverage under your policy’s dwelling coverage, up to your chosen limit.

Personal property coverage reimburses furniture, clothing, electronics, and other belongings you own. You should select replacement cost coverage rather than actual cash value to avoid depreciation penalties. Many Alaska condo owners underestimate the value of their belongings and set limits too low, then face claim denials for items that exceed their coverage. Take time to inventory your possessions and add up replacement costs realistically-a used couch costs more to replace than insurance companies typically estimate.

Water Damage and Theft Protection

Water damage and theft represent two perils that hit Alaska condos frequently, and your condo policy covers both. Frozen pipes, ice dam leaks, and toilet overflows damage flooring, cabinets, and personal property constantly during Alaska winters, and your policy pays for repairs and replacement. Theft coverage protects your belongings if someone breaks into your unit or steals items from common areas, though you may need to document serial numbers or purchase receipts for high-value electronics to streamline claims.

Loss Assessment Coverage

Loss assessment coverage separates smart condo owners from those facing financial surprises. When the HOA needs to pay a large deductible or fund repairs to common areas, the association spreads costs among all unit owners through special assessments, and loss assessment coverage reimburses these unexpected bills up to your chosen limit. Without this optional coverage, you could face assessments of several thousand dollars if a major loss affects the building’s roof, foundation, or electrical systems.

Alaska condo associations frequently levy assessments for winter weather damage, and the cost to add loss assessment coverage-typically $50 to $100 annually for reasonable limits-is minimal compared to the protection it provides. Choose a loss assessment limit that matches your HOA’s master policy deductible and the potential size of assessments based on your building’s age and condition. If your association has an older roof or aging plumbing, higher assessment coverage makes sense. Review your HOA meeting minutes and reserve study documents to understand what major repairs may be coming, then set your loss assessment limit accordingly.

Medical Payments and Liability Protection

Medical payments coverage rounds out your policy by paying medical expenses for guests injured in your unit, regardless of fault, preventing small slip-and-fall incidents from becoming lawsuits. Most policies include $1,000 to $5,000 in medical payments coverage, which covers an injured guest’s doctor visits and minor emergency care without requiring you to prove negligence. These three coverage components-interior improvements, personal property, and liability protection-work together to fill the gaps left by your HOA master policy.

Understanding what each component covers helps you select appropriate limits when you shop for quotes and compare carriers in Alaska’s competitive insurance market.

How to Get Accurate Condo Insurance Quotes in Alaska

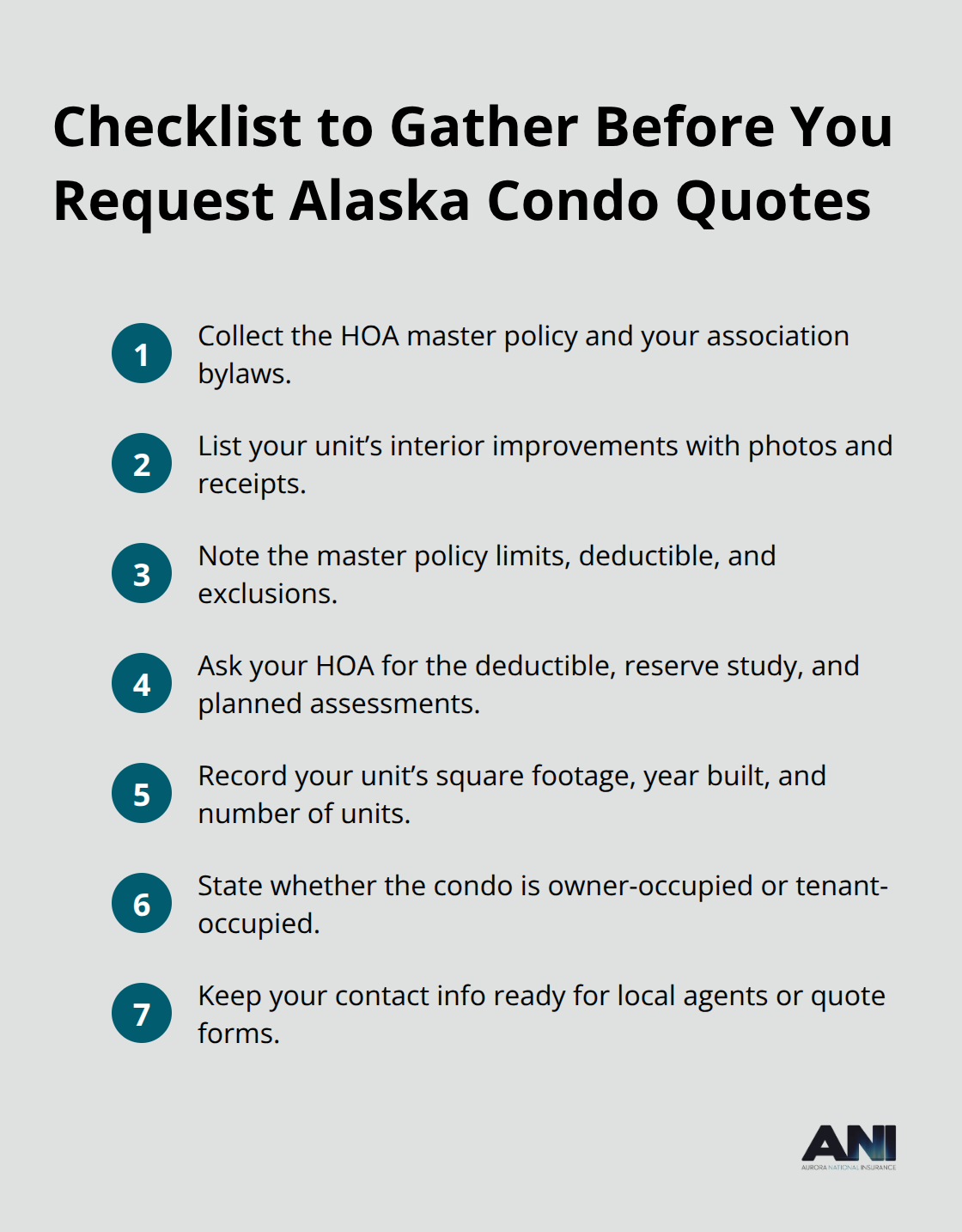

Gather the Information Carriers Need

Requesting condo insurance quotes in Alaska requires preparation that most owners skip. You need specific information about your unit and HOA coverage before contacting carriers, or you’ll receive quotes that don’t reflect your actual situation. Start by collecting your HOA master policy documents, your condo association’s bylaws, and details about your unit’s improvements. Note the master policy’s coverage limits, deductible amount, and what it explicitly excludes. Contact your HOA directly and ask for the master policy deductible, the association’s reserve study, and any planned assessments.

This information determines how much loss assessment coverage you need and what dwelling limits make sense for your improvements.

If your kitchen has custom cabinets or you’ve installed hardwood floors, document these upgrades with photos and receipts. When you contact insurers, provide your unit’s square footage, year built, number of units in the building, and whether your condo is owner-occupied or tenant-occupied. Alaska Service Agency, a local resource for Alaska condo quotes, requires your name, email, and phone number to provide personalized quotes and operates at (907) 337-2311.

Compare Rebuild Cost Estimates Across Carriers

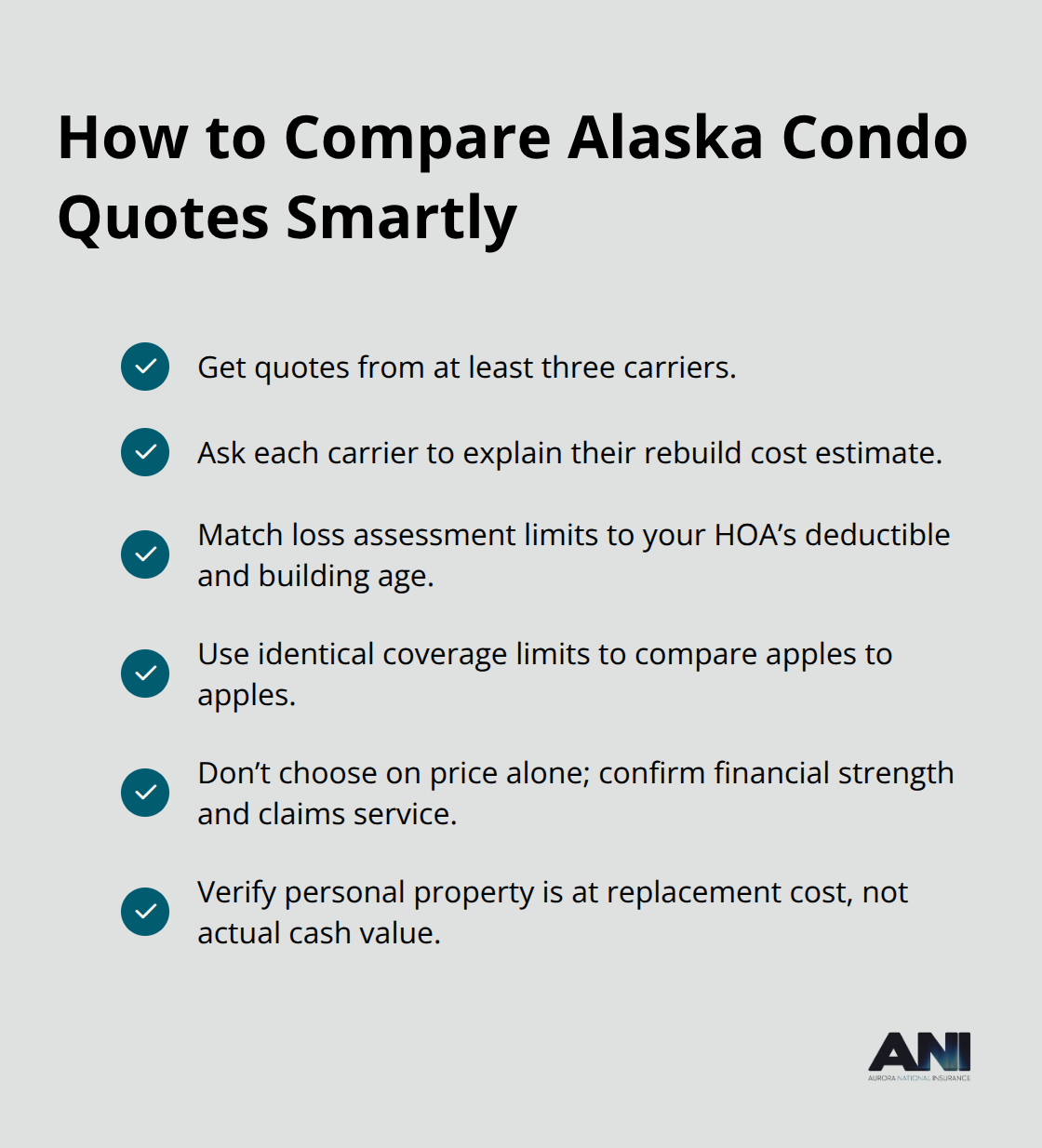

Comparing quotes across multiple carriers reveals massive price variations driven by how each insurer calculates rebuild costs and assesses risk. A Reddit discussion on r/anchorage showed a USAA customer facing a premium jump from $2,100 to $3,500 annually due to a higher rebuild cost estimate, a 66.7% increase that illustrates why comparing carriers matters. Request quotes from at least three carriers and ask each one to justify their rebuild cost figure, because this single number drives your premium more than any other factor.

When reviewing quotes, verify that loss assessment coverage limits align with your HOA’s deductible and building age. Older buildings with aging roofs or plumbing systems warrant higher assessment limits, typically $5,000 to $10,000, while newer condos may need only $2,500 to $5,000.

Verify Coverage Details Match Your Needs

Pay close attention to whether quotes include replacement cost or actual cash value for personal property, as replacement cost coverage costs more but prevents depreciation penalties on claims. Request identical coverage limits across all quotes so you’re comparing apples to apples, not different protection levels at different prices. Don’t select a quote based on price alone; verify that the carrier is financially strong and has responsive claims handling, because a cheap premium means nothing if the insurer struggles to pay claims when you need them.

Final Thoughts

Choosing the right condo insurance in Alaska requires you to balance three critical factors: understanding what your HOA master policy covers, selecting appropriate limits for your personal improvements and belongings, and protecting yourself from unexpected assessments. The gap between what the association covers and what you own is substantial, and underestimating this gap leaves you financially exposed when loss strikes. Your condo policy must reflect your unit’s actual condition, including any upgrades you’ve made, and your liability exposure in a shared living environment.

Alaska condo insurance quotes vary significantly across carriers because each insurer calculates rebuild costs differently-sometimes by thousands of dollars annually. You should gather your HOA documents, document your improvements with photos, and request quotes from multiple carriers using identical coverage details. Verify that each carrier offers replacement cost coverage for personal property, adequate loss assessment limits, and strong financial ratings before you make your decision.

Local Alaska agents understand your state’s unique risks and how HOA policies interact with personal coverage in ways that national carriers often miss. Aurora National Insurance represents multiple top-rated carriers and provides tailored comparisons that help you find the right protection at competitive prices. Contact us today for instant online quotes and expert guidance on Alaska condo insurance that fits your needs and budget.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.