Rural Alaska Home Insurance: Protecting Remote Homes From Seasonal Risks

Rural Alaska home insurance isn’t a luxury-it’s a necessity. Homes in remote areas face weather patterns, isolation, and wildlife threats that standard policies simply don’t cover.

At Aurora National Insurance, we’ve seen firsthand how seasonal risks can devastate unprotected properties. The right coverage makes the difference between financial security and catastrophic loss.

What Makes Rural Alaska Homes So Hard to Insure

Frozen Pipes and Water Damage in Extreme Cold

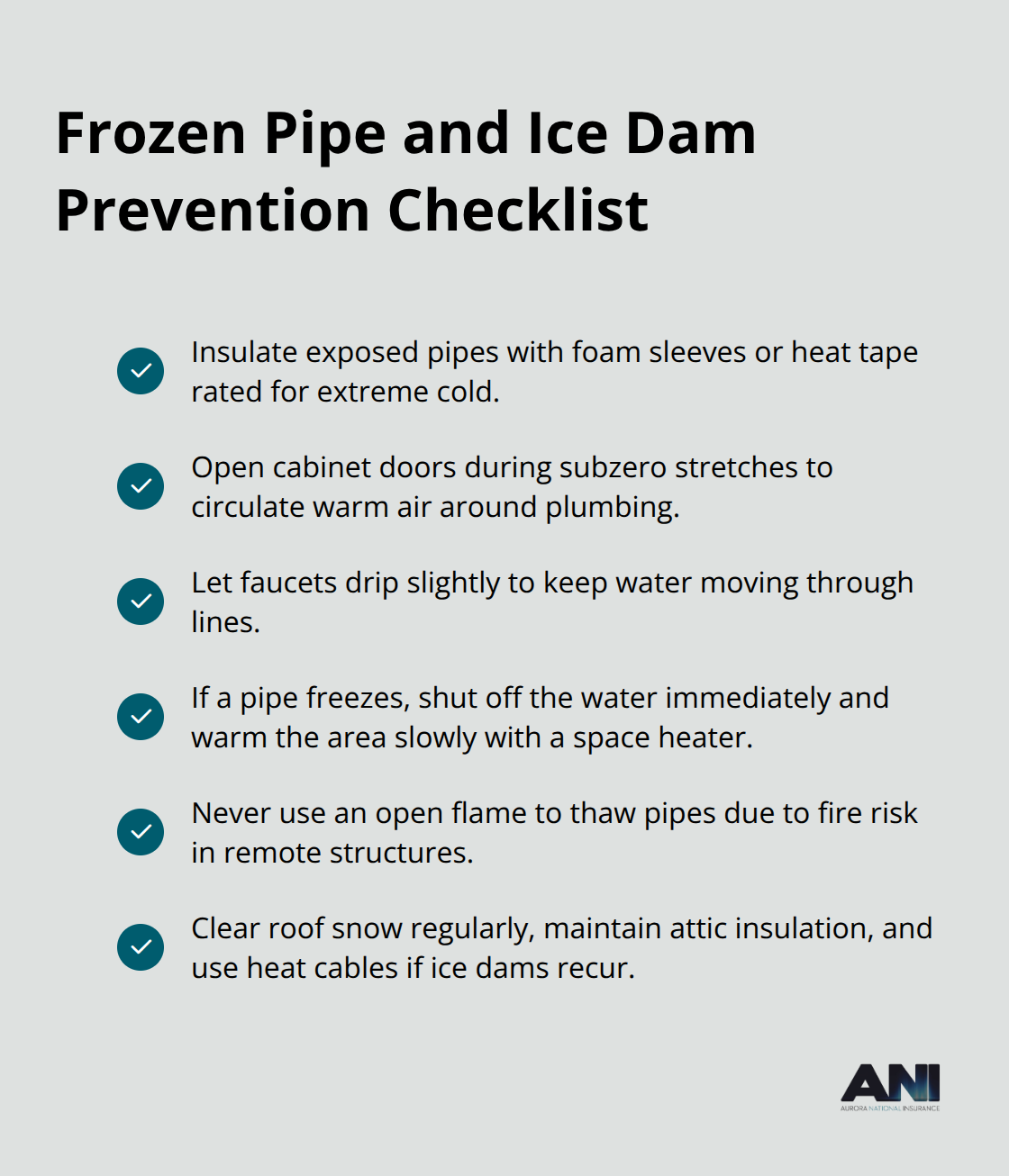

Extreme cold in rural Alaska destroys homes systematically. When temperatures drop below minus 20 degrees Fahrenheit for weeks at a time, frozen pipes become inevitable without constant vigilance. Water damage from burst pipes ranks as one of the costliest claims in remote Alaska properties, and standard homeowners policies cover the damage itself, but only if you take reasonable precautions. You must keep cabinet doors open around plumbing, let faucets drip during cold snaps, and insulate pipes in crawlspaces and basements. If a pipe freezes, you shut off water immediately and warm the area slowly with a space heater-never use an open flame, which risks fire in structures already vulnerable due to isolation.

Ice dams compound the problem significantly. Heavy snow combined with temperature swings causes melted water to back up under shingles and leak inside. The EPA notes that average winter temperatures in Alaska have risen about 6 degrees Fahrenheit over six decades, yet this warming paradoxically increases freeze-thaw cycles that create ice dams. You prevent them by keeping your attic well-insulated, regularly clearing snow from the roof with a roof rake, and installing heat cables along roof edges if dams recur.

Fire Risk and Limited Emergency Response

Limited fire protection infrastructure in rural areas means that when a fire starts, your home faces near-total loss. Remote properties typically have ISO protection classes of 9 or 10 due to sparse fire departments and slow response times, which directly increases your insurance premiums and may make some carriers unwilling to write coverage at all. Wildfire risk around areas like Fairbanks and the Mat-Su Valley can trigger surcharges or coverage denials if your property lacks defensible space-a 30-foot cleared perimeter around structures is standard, though insurers increasingly use satellite vegetation data to assess risk precisely.

Heating System Failures and Underwriting Challenges

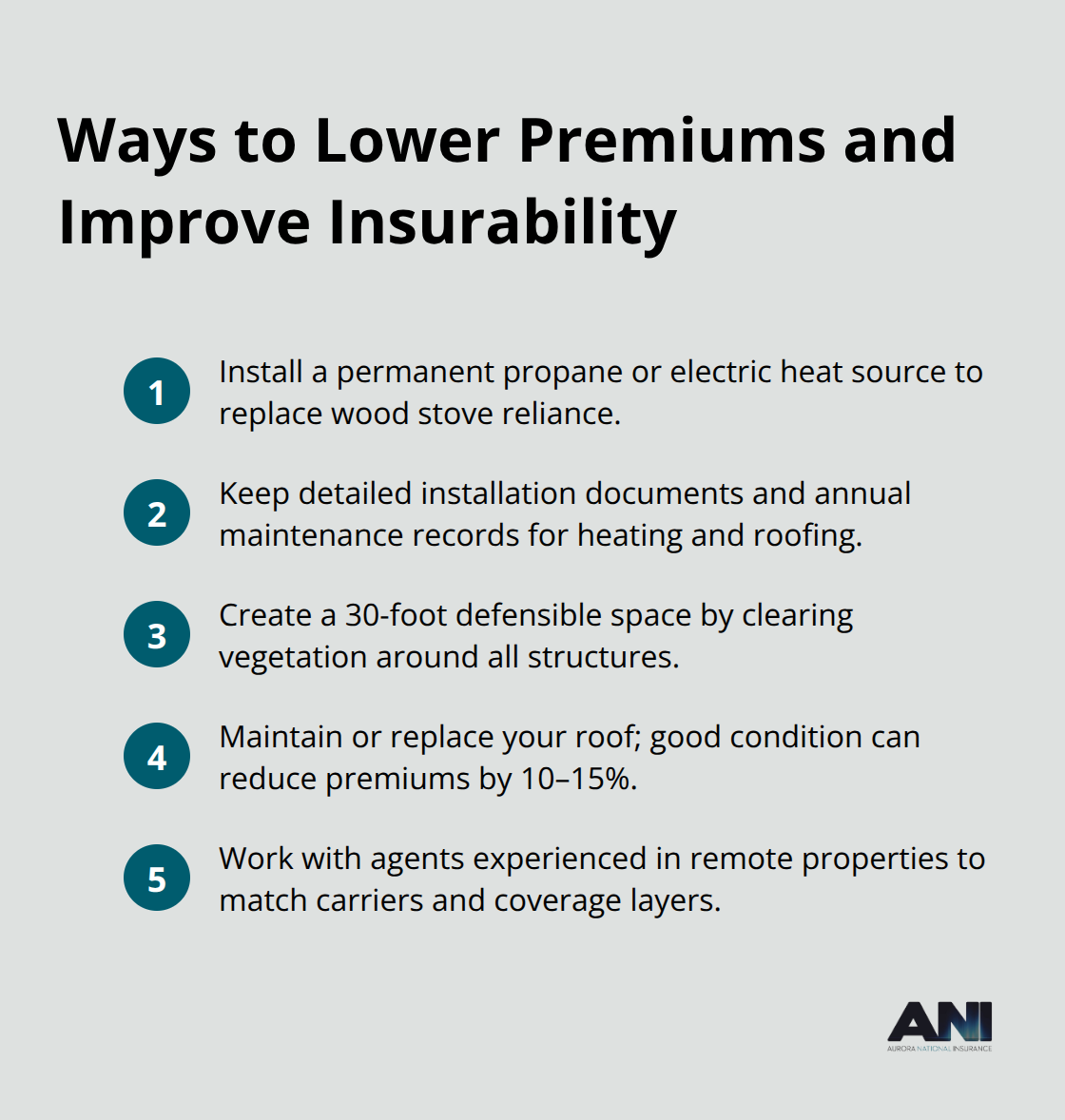

Heating system failures during extreme cold create life-threatening situations that insurance cannot prevent but must account for in underwriting. Many remote homes rely on wood stoves or portable heaters as primary heat sources, which complicates coverage because insurers view these as higher-risk than permanent propane or electric systems. You significantly improve your insurability and reduce premiums by installing a permanent heat source rather than depending on wood.

Isolation as an Underwriting Factor

Isolation itself becomes an underwriting factor that shapes your coverage options. The lack of year-round road access can limit coverage options entirely, forcing you toward excess and surplus lines carriers that charge substantially more. You must disclose proximity to water sources and other location details to your agent because these factors influence both premium and coverage terms directly. Understanding these underwriting realities helps you prepare the documentation and property improvements that make your remote home more insurable-a topic we address in detail as we explore the specific coverage options available to rural Alaska homeowners.

What Coverage Actually Works for Remote Alaska Homes

Why Standard Policies Fall Short in Rural Settings

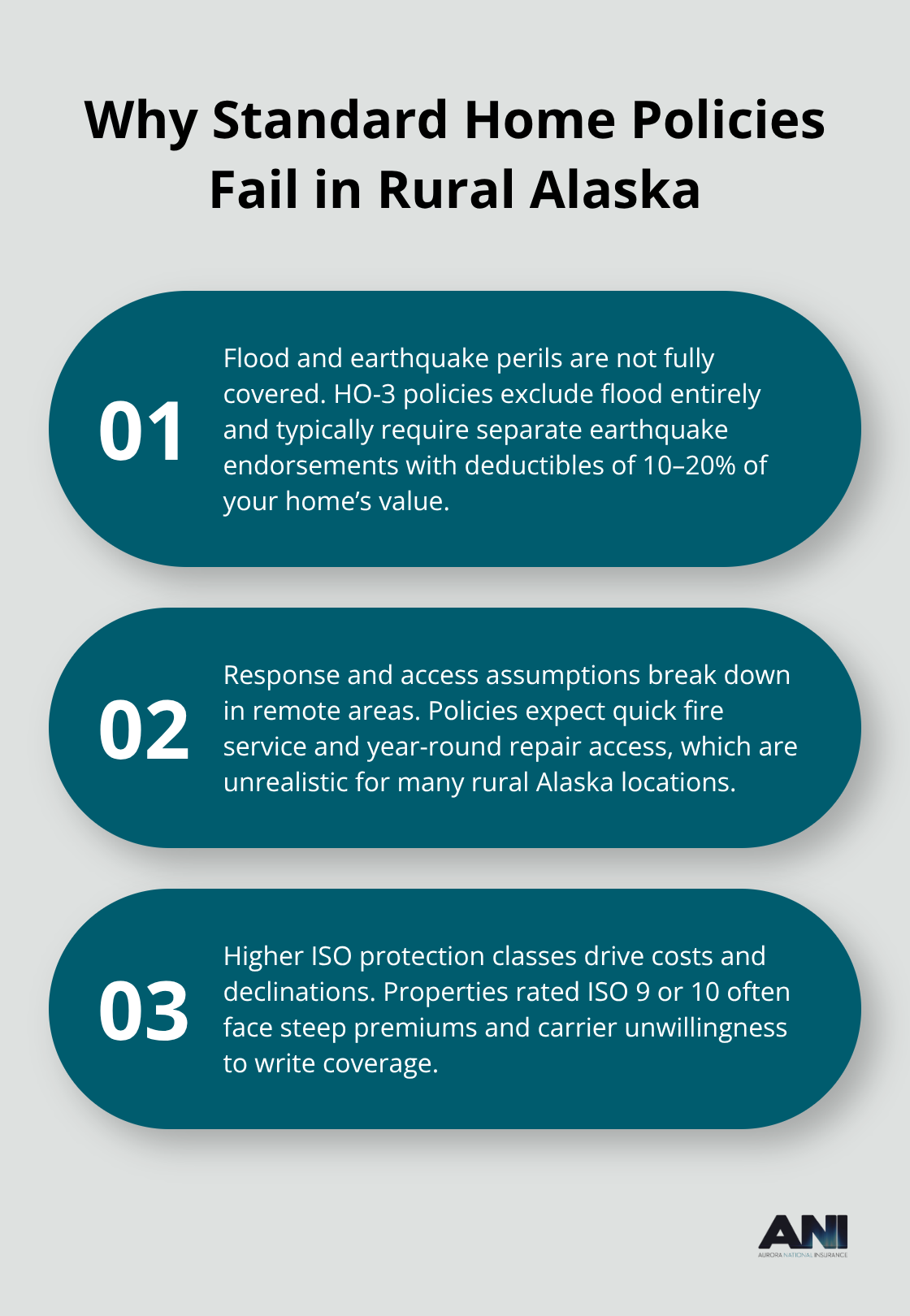

Standard homeowners policies sold in urban Alaska collapse under the weight of rural conditions. The standard HO-3 policy covers fire, windstorm, hail, theft, and vandalism, but it excludes flood damage entirely and typically excludes earthquake damage unless you add a separate endorsement with deductibles running 10 to 20 percent of your home’s value. More critically, standard policies assume fire departments arrive within minutes and that repair crews can reach your property year-round. In remote Alaska, neither assumption holds true.

Insurers classify rural properties at ISO protection classes 9 or 10 due to limited fire protection infrastructure, which directly drives higher premiums and causes many carriers to decline coverage altogether.

Layering Coverage for Remote Alaska Risks

You cannot simply buy a standard policy and expect it to protect a remote home. You need specialized coverage that acknowledges the realities of your location. Flood insurance through the National Flood Insurance Program forms the foundation of rural protection. NFIP policies cost roughly 20 to 40 percent less than private flood carriers in Alaska and provide up to standard limits, though a proposed Alaska Flood Authority under SB 11 could eventually offer up to one million dollars in coverage. Water backup endorsements address sump pump failures and drain backups that plague freeze-thaw cycles, typically costing 10 to 15 dollars annually per thousand dollars of coverage. Earthquake endorsements become essential if your property sits in high-risk zones like Anchorage or southern coastal areas, though these require separate policies with substantial deductibles and sometimes geological assessments that add 200 to 400 dollars to your annual cost.

Excess and Surplus Lines Carriers for High-Risk Properties

Specialized policies for excess and surplus lines carriers become necessary when standard insurers reject your property outright. These carriers accept risks that traditional companies won’t touch, including homes with wood stove heating, limited road access, or high wildfire exposure. Expect premiums 30 to 50 percent higher than standard market rates, but the alternative is no coverage. Home Protector endorsements add roughly 25 percent to your rebuilding cost coverage and address specific gaps in standard protection.

Structuring Personal Property and Liability Protection

Personal property coverage on remote properties should run at least 50 percent of your dwelling limit, and if you own high-value equipment like snowmobiles or fishing gear, scheduled personal property coverage protects these items at replacement cost rather than depreciated value. Personal liability coverage should exceed 100,000 dollars on rural properties where you host workers or guests regularly. The average Alaska homeowner pays around 1,035 dollars annually for 300,000 dollars of dwelling coverage according to Quadrant Information Services data, but rural properties typically cost 1,500 to 2,200 dollars for equivalent coverage due to underwriting challenges.

Reducing Premiums Through Property Improvements and Documentation

Permanent heat sources like propane or electric systems can reduce premiums by 15 to 25 percent compared to wood stove reliance. Maintaining detailed documentation of heating system installation, annual maintenance records, and roof condition gives you leverage during underwriting and renewal. Agents experienced in remote properties account for Alaska-specific risks far better than automated online quotes, which cannot adapt to the complexities of your location. This expertise becomes invaluable as you move forward with selecting the right agent and preparing your property for the seasonal challenges ahead.

Protecting Your Rural Home Through the Seasons

Winter Pipe Protection and Maintenance

Winter demands relentless attention to prevent catastrophic damage. The most effective defense against frozen pipes starts before temperatures plummet-you must insulate all exposed pipes in crawlspaces, basements, and exterior walls with foam sleeves or heat tape rated for Alaska’s extreme cold. During subzero stretches, you should open cabinet doors under sinks to circulate warm air around plumbing and let faucets drip slightly to maintain water movement through the lines. If a pipe freezes despite these measures, you must shut off the water supply immediately and warm the area slowly using a space heater or electric heat tape. Never use an open flame, which creates fire risk in structures already vulnerable due to isolation and delayed emergency response.

Managing Ice Dams and Roof Damage

Ice dams require year-round preparation to prevent costly water intrusion. You should keep your attic insulated to at least R-38 to prevent heat loss that melts snow on the roof, and you must regularly clear accumulated snow using a roof rake before it builds up. If dams recur seasonally, you can install heat cables along roof edges to manage the problem. These preventive steps directly reduce your risk profile and can lower your insurance premiums.

Heating System Reliability and Backup Plans

Heating system failures become life-threatening in extreme cold, so you must schedule annual maintenance before winter arrives and replace filters regularly. You should keep fuel tanks filled to ensure continuous heat availability throughout the season. You need backup heat sources ready-electric heaters or a properly installed wood stove-and you should know how to close unused rooms to conserve warmth if your primary system fails. Your documentation of heating system installation and annual maintenance records directly influences your insurability and premium rates, making these records essential to maintain and provide to your agent during underwriting.

Wildfire Prevention and Defensible Space

Wildfire prevention and year-round inspections protect both your property and your insurance coverage. You must clear vegetation within 30 feet of all structures to create defensible space, removing dead branches, fallen limbs, and dense brush that fuel rapid fire spread. Insurers increasingly use satellite vegetation data to assess wildfire risk precisely, so this work directly affects your ability to secure coverage and your premium cost. You should inspect your roof annually for damage, missing shingles, or debris accumulation that compromises fire resistance-a newer roof or one maintained in good condition can reduce premiums by 10 to 15 percent.

Property Inspections and Documentation

You must check all exterior walls, foundation, and outbuildings for gaps, cracks, or deterioration that allows water infiltration during freeze-thaw cycles. You should test your water system before winter to ensure pipes flow freely and identify weak points before temperatures drop. You must document these inspections with photos and maintenance records, which strengthen your position during claims and demonstrate that you maintain the property to insurable standards. This consistent attention to your property’s condition separates insurable remote homes from those carriers reject outright.

Final Thoughts

Rural Alaska home insurance requires a fundamentally different approach than coverage in urban or suburban areas. Standard homeowners policies cannot address frozen pipes, wildfire exposure, heating system failures, and delayed emergency response that define remote Alaska living. You need flood coverage through the National Flood Insurance Program, water backup endorsements for freeze-thaw damage, and earthquake protection if your property sits in a high-risk zone, plus excess and surplus lines carriers when standard insurers decline your property.

An agent who understands Alaska’s specific challenges separates adequate coverage from catastrophic gaps. Local expertise matters because remote properties require documentation, property improvements, and coverage structures that automated online quotes cannot address. An experienced agent knows which carriers accept remote properties, how to layer coverage for maximum protection, and which underwriting factors directly influence your premium and eligibility.

We at Aurora National Insurance work with you to structure the protection your rural Alaska home actually needs. Contact Aurora National Insurance to get quotes from multiple carriers and discuss the specialized coverage your remote property requires.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.