Alaska Rental Property Insurance: Local Coverage for Landlords

Owning rental property in Alaska comes with distinct challenges that landlords in the lower 48 states rarely face. Extreme weather, remote locations, and limited insurance options mean you need Alaska rental property insurance that actually fits your situation.

At Aurora National Insurance, we’ve helped countless Alaska landlords protect their investments with coverage designed for the state’s unique risks. This guide walks you through what you need to know.

Why Alaska Rental Property Insurance Costs More

The Alaska Premium Drives Prices Higher

Alaska rental property insurance operates in an entirely different pricing environment than the continental U.S., and costs reflect genuine, measurable risk. Landlord insurance in Alaska averages around $1,230 per year, but that baseline masks the real story: premiums have surged over 25% in the last 18 months due to the Alaska Premium-the higher labor and shipping costs combined with severe weather exposure that underwriters factor into every quote. This isn’t theoretical pricing. When you need a roof repair in Anchorage or Juneau, contractors charge significantly more than in Seattle or Portland, and that reality flows directly into your insurance costs.

Earthquake and Flood Risks Require Extra Coverage

Alaska is the most seismically active state in the nation, which means standard landlord policies exclude earthquake damage entirely. You’ll need a separate Difference in Conditions endorsement to cover foundation damage from seismic activity, and most carriers require this as a non-negotiable add-on for Alaska properties. Flood risk compounds the problem: Alaska’s ice jams and spring breakups create flooding scenarios that generic insurance models don’t account for, forcing you to purchase separate National Flood Insurance Program coverage or a private flood policy if your property sits in a designated flood zone.

Remote Location Multiplies Replacement Costs

Remote location multiplies replacement costs in ways that catch many landlords off guard. A standard homeowners policy might work in Arizona, but an Alaska rental property needs dwelling coverage that reflects true replacement cost in your specific location-not a national average. Properties in rural areas face even steeper premiums because access for repairs takes longer and costs more.

Limited Carriers and Policy Types Shape Your Options

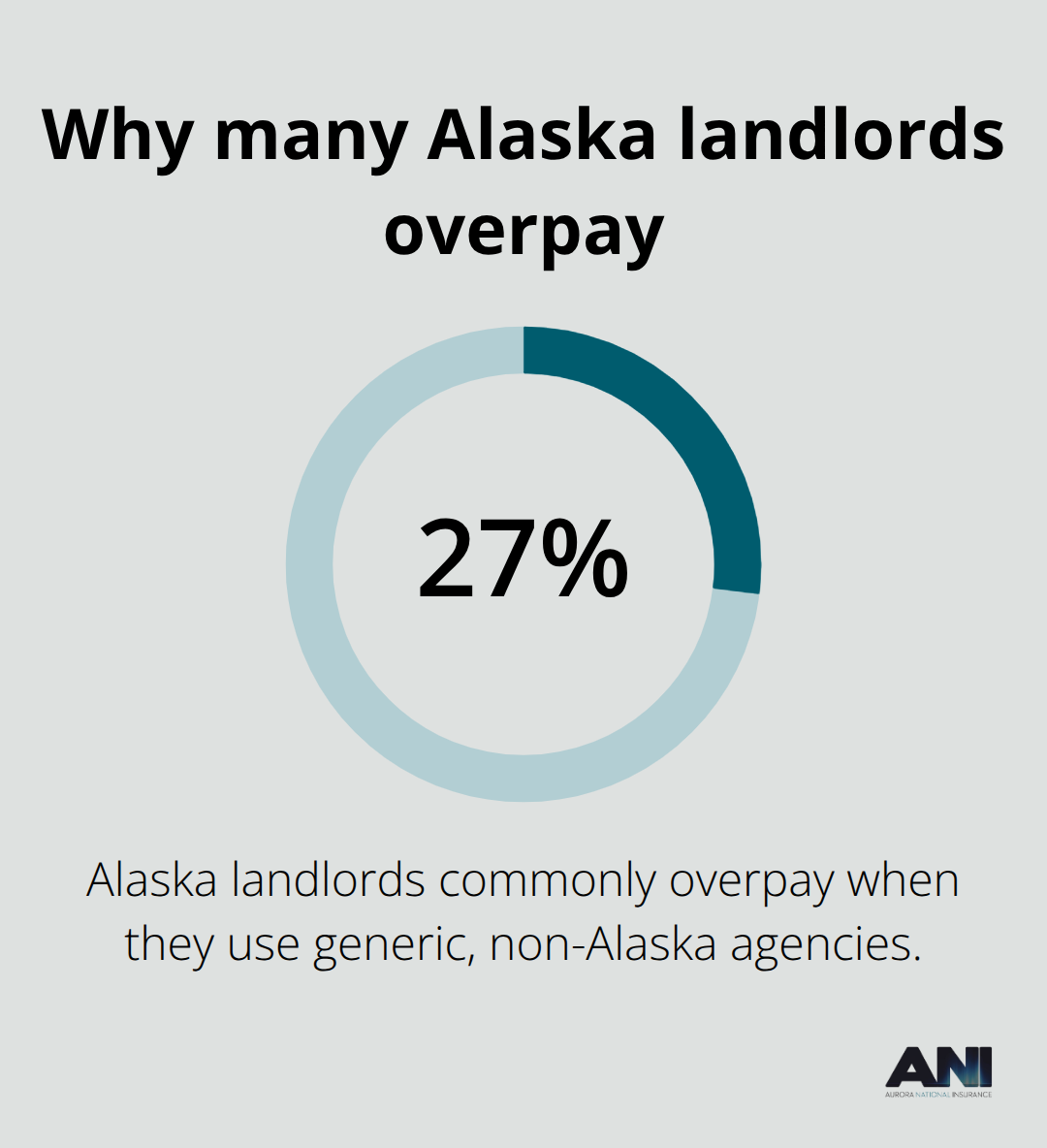

Limited carrier options in Alaska mean you shop from a smaller pool than landlords in populated states, and that scarcity drives prices upward. Industry data shows Alaska landlords commonly overpay about 27% by working with generic agencies that don’t understand local risk factors. The difference between a DP-1 Basic policy and a DP-3 Special Form policy runs substantial-DP-3 covers open perils and is what most Alaska landlords choose because it protects against the broader range of weather-driven damage the state delivers.

Deductibles, Underinsurance, and Maintenance Records

Deductibles matter enormously here: raising your deductible from $500 to $1,000 or $2,500 lowers premiums noticeably, but in Alaska’s climate, small claims add up fast and can trigger future rate increases or coverage denials if claimed repeatedly. The math demands that you understand your property’s actual replacement cost value and insure to that amount, not a percentage less. Underinsurance penalties apply if you fall short-you’ll pay more out-of-pocket when a claim hits because the insurer reduces your payout proportionally. Documented upgrades like new roofs, updated heating systems, and robust weatherproofing signal lower risk to underwriters and yield meaningful rate credits, so you should keep maintenance records and present them at renewal time. Understanding these cost drivers prepares you to select the right coverage type and limits for your specific property, which brings us to the coverage types that every Alaska landlord actually needs.

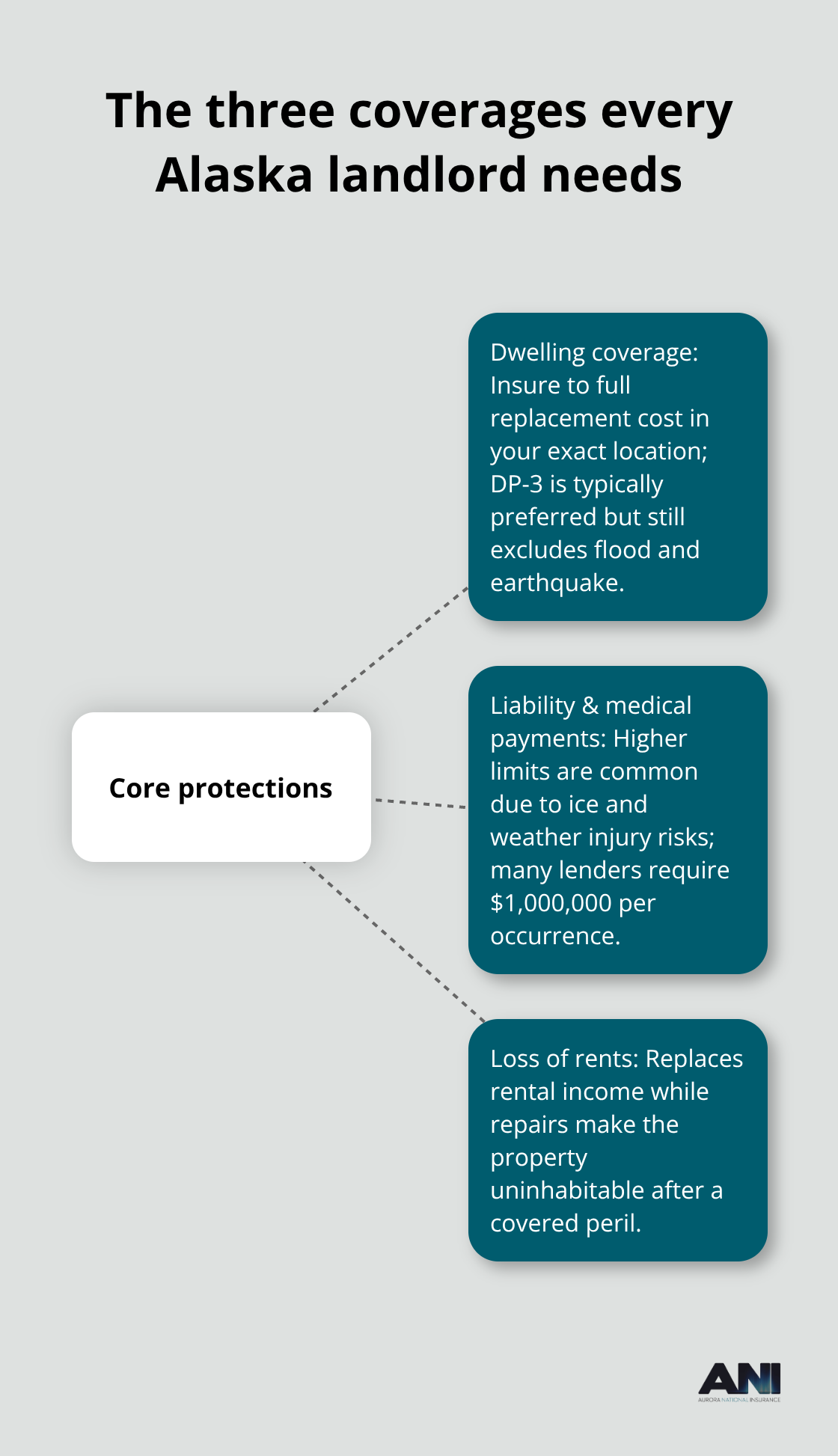

The Three Coverage Types That Protect Your Alaska Rental Income

Dwelling Coverage: Get the Limit Right

Standard landlord policies in Alaska come in three forms: DP-1 Basic covers named perils like fire and theft, DP-2 Broad adds windstorm, hail, and smoke damage, and DP-3 Special Form covers open perils and is what most Alaska landlords should choose because it protects against nearly everything except flood, earthquake, and a few other excluded events. The critical decision isn’t the form type-it’s the coverage limit itself. You must insure the dwelling to full replacement cost value in your specific location, not a national average or a percentage less than replacement cost.

Underinsurance penalties hit hard. If you insure a property worth $300,000 to replace for only $240,000, and a covered loss hits for $100,000, the insurer calculates your payout as $80,000 because you failed to meet the coinsurance requirement. That $20,000 gap comes straight from your pocket. In Alaska, where labor and materials run 30-40% higher than the continental U.S., this mistake costs thousands.

Have a professional rebuild estimate completed every two to three years and adjust your dwelling limit accordingly. Documented upgrades to your heating system, roof, or plumbing reduce your rebuild estimate and lower premiums, so keep receipts and share them at renewal.

Liability and Medical Payments: Protect Against Injury Claims

Liability coverage protects you when a tenant, guest, or visitor gets injured on your property and sues. Alaska’s icy walkways and extreme weather create genuine injury risk, which is why general liability typically runs higher here than in other states-most landlords carry $500,000 to $1,000,000 per occurrence limits, and many lenders require the higher amount.

Premises medical payments, usually included at around $5,000 per occurrence, covers immediate medical costs if someone gets hurt on your property regardless of fault. This coverage often prevents lawsuits before they start because injured parties receive prompt payment for their medical bills.

Loss of Rents: Replace Your Income During Repairs

Loss of rents coverage reimburses you for lost rental income if a covered peril makes the property uninhabitable during repairs. If your rental brings in $3,000 monthly and a fire requires three months of repairs, loss of rents coverage pays you $9,000 instead of leaving you with a vacant property and zero income while reconstruction happens.

The cost is modest-typically around $1 per $1,000 of annual rent-so a $36,000 annual rent might cost only $36 per year for a $36,000 loss-of-rents limit. Alaska landlords with mortgages often discover their lender requires this coverage anyway, so the real question is whether you’re buying enough.

Calculate your annual rental income, divide by 12 to get monthly rent, then multiply by the number of months your property would realistically sit vacant during major repairs. In Anchorage or Juneau, try at least three to four months for serious structural damage. That calculation tells you the loss-of-rents limit you actually need, not what some agent suggests. Once you understand what coverage protects your property and income, the next step is finding the right insurance provider who knows Alaska’s specific landscape and can match you with carriers that deliver both competitive rates and reliable claims support.

Finding the Right Alaska Insurance Agent

Specialize or Overpay: The Agent Decision Matters

The difference between paying 27% too much for landlord insurance and getting a fair price often comes down to one decision: who you hire to shop your coverage. Alaska’s insurance market does not reward laziness. Generic agencies that operate nationwide treat Alaska like any other state, missing the specific risk factors that drive your actual costs. An agent who knows Alaska rental properties will flag that your property sits in an earthquake zone and recommend a Difference in Conditions endorsement before you discover the exclusion on a claim. That same agent will ask about your roof age, heating system condition, and documented maintenance records because these factors yield 10-15% rate reductions that generic agencies never uncover. When you contact an insurance provider, ask directly whether they specialize in Alaska rental properties and how many Alaska landlords they represent. If the answer is vague or they treat you like any other state, move to the next call.

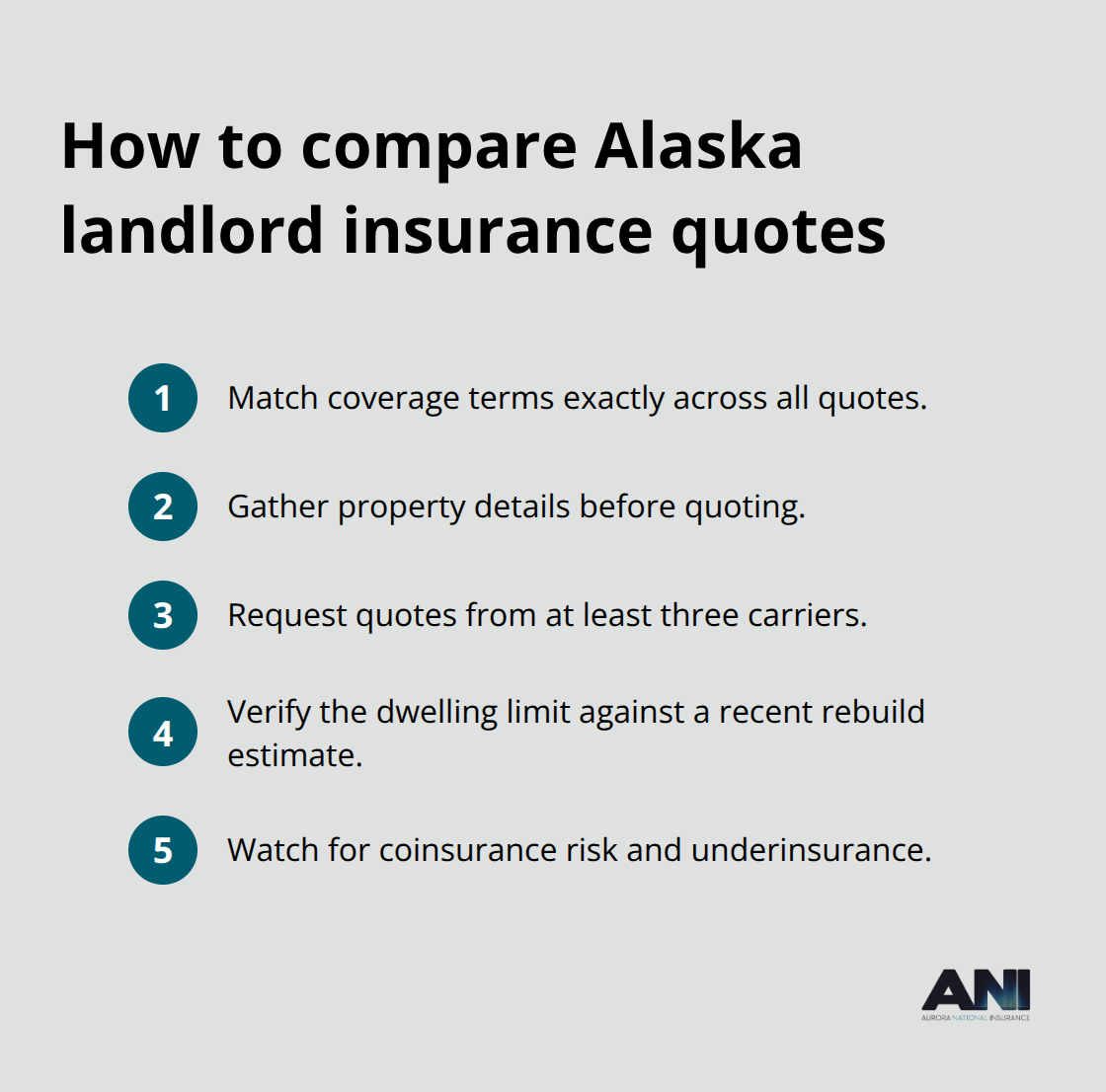

Request Identical Quotes Across Multiple Carriers

Comparing quotes across multiple carriers is non-negotiable, but comparison only works if you look at identical coverage. Request quotes for the same dwelling limit, deductible, liability limit, and loss-of-rents coverage from at least three carriers so you see actual price differences rather than comparing apples to oranges. Document your property’s square footage, year built, roof condition, heating system type, and whether you have any prior claims, because these details shift premiums significantly.

Once you receive quotes, verify that each one reflects your property’s actual replacement cost value by checking the dwelling limit against a recent professional rebuild estimate. If a carrier quotes you for $250,000 in dwelling coverage but your property costs $350,000 to replace, you are underinsured and will face coinsurance penalties when a claim hits.

Verify Coverage Gaps and Carrier Strength

Ask each agent to walk you through their carrier’s DP-3 coverage exclusions, especially around flood and earthquake, so you know exactly what gaps exist and what endorsements you need to close them. Request that your quotes include AM Best ratings for each carrier because lenders typically require A- VIII or better, and weaker carriers may deny coverage or disappear during claims surges. This step protects you from binding coverage with a financially unstable insurer who cannot pay claims when disaster strikes Alaska properties.

Evaluate Policy Flexibility and Rate Lock Terms

Ask about month-to-month policy options versus annual lock-ins, since Alaska’s market moves fast and you want flexibility to switch if a carrier raises rates dramatically at renewal. Some carriers offer month-to-month terms that let you adjust coverage as your property portfolio grows or market conditions shift. Others lock you into annual agreements that leave you stuck with unfavorable rates for twelve months. Understanding these terms upfront prevents surprises and keeps your options open as Alaska’s insurance landscape continues to shift.

Final Thoughts

Alaska rental property insurance protects your income stream and financial stability in a state where standard policies fail to deliver adequate protection. Your dwelling limit must reflect actual replacement cost in your location, not a national average, because underinsurance penalties will cost you thousands when a claim hits. The agent you select determines whether you pay fair rates or overpay by 27 percent, which is why working with someone who specializes in Alaska rental properties makes a measurable difference.

An agent familiar with Alaska rental properties knows which carriers offer month-to-month flexibility, which ones provide the strongest earthquake endorsements, and how to structure your loss-of-rents coverage to match your actual income. They understand that a roof in Juneau ages differently than one in Seattle, that heating system failures drive claims in ways other states never see, and that documented maintenance records yield real rate credits. This expertise translates directly into lower premiums and better coverage alignment.

Contact an independent Alaska insurance agency that represents multiple carriers and can shop your Alaska rental property insurance across different options. At Aurora National Insurance, our Anchorage-based team understands Alaska’s rental property landscape and delivers tailored comparisons from top-rated carriers with instant online quotes. Request quotes today and verify that your coverage reflects your property’s true replacement cost, your liability exposure, and your income protection needs.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.