Washington Rental Property Insurance: Local Solutions for Property Owners

Owning rental property in Washington comes with real financial exposure. Tenant injuries, property damage, and lost rental income can drain your savings fast.

Standard homeowners policies leave you vulnerable in these exact situations. At Aurora National Insurance, we’ve helped countless Washington property owners protect their investments with coverage designed specifically for rental properties.

Why Rental Property Insurance Protects Your Bottom Line

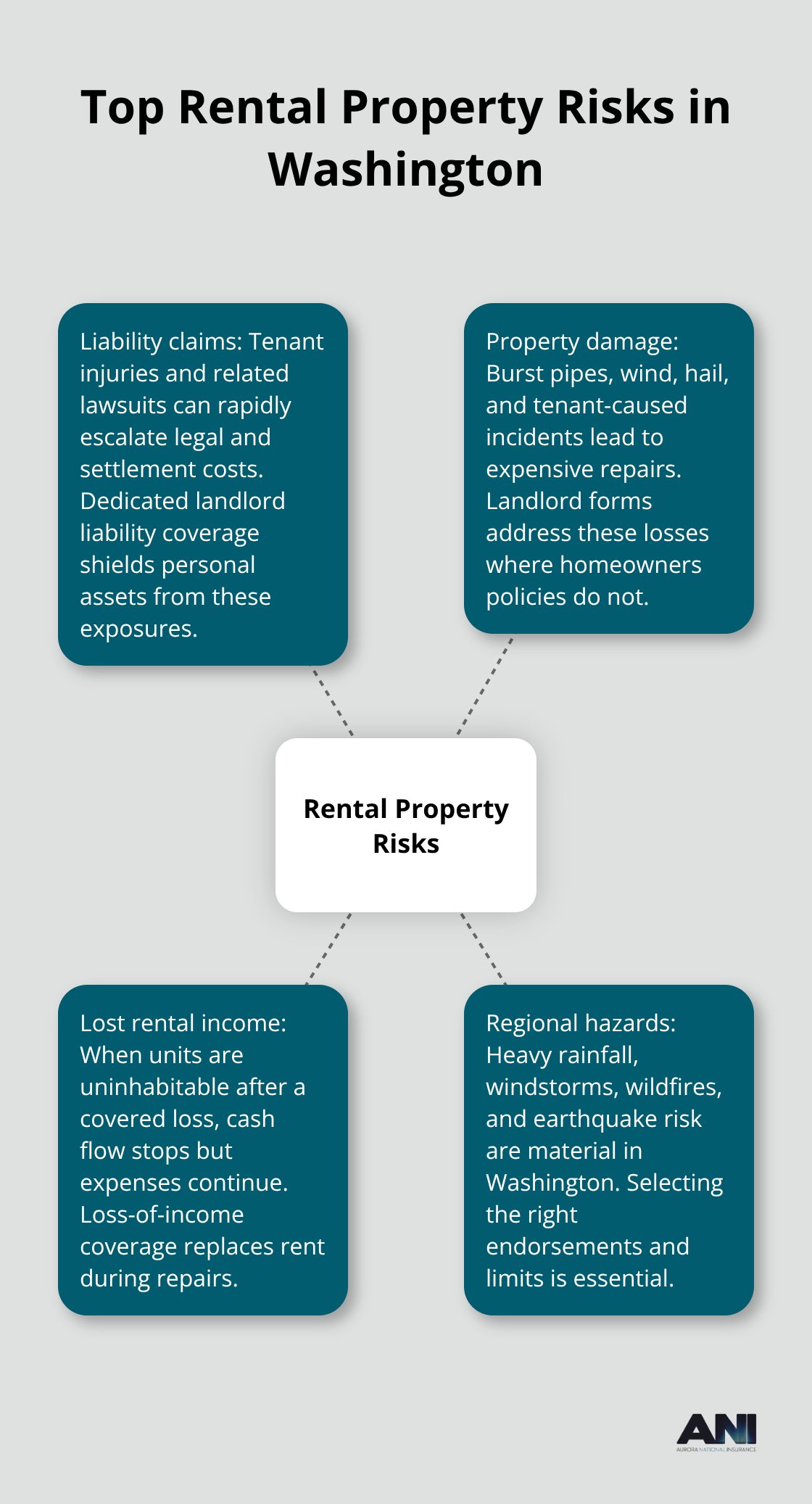

Liability Claims Can Devastate Your Finances

Liability claims from tenant injuries alone can cost $50,000 to $300,000 depending on severity, and standard homeowners policies explicitly exclude rental properties. A tenant who slips on your stairs, gets injured by a defective appliance, or claims discrimination can file a lawsuit that decimates your equity if you lack proper coverage. Most landlords across Washington assume their homeowners policy covers rental units-it does not. Rental property insurance provides the liability protection you need, typically starting at $500,000 in coverage for single-family rentals and scaling up for multifamily buildings.

Property Damage Happens More Often Than You Think

Property damage occurs constantly in rental units. Tenants cause damage through negligence or intentional acts, pipes freeze and burst during winter, and wind or hail from Pacific storms damage roofs and siding. A single burst pipe can cost $3,000 to $25,000 in repairs, and if the damage makes the unit uninhabitable, you lose rental income immediately. Standard homeowners policies will not pay for any of this because the property is occupied by tenants, not you.

Lost Rental Income Drains Cash Flow Fast

Loss of rental income is the financial killer most landlords underestimate. If a fire or major weather event forces repairs lasting three to six months, your mortgage, property taxes, and maintenance costs continue while rent stops coming in. In dense markets like Seattle, a six-month vacancy translates to over $13,000 in lost gross revenue on a modest two-bedroom rental. Rental property insurance includes loss-of-income coverage that replaces your actual rental income while repairs happen, preserving your cash flow when you need it most.

Washington’s Climate Creates Unique Risks

Western Washington experiences heavy rainfall and windstorms that damage roofs and gutters, while eastern Washington faces wildfire exposure that increases annually. The Cascadia subduction zone creates a 14 percent chance of a magnitude-7 earthquake within the next 50 years, another threat standard policies do not address. So ensure you add earthquake coverage in Washington. Understanding these regional hazards helps you select the right coverage limits and endorsements for your specific situation.

What Homeowners Policies Actually Exclude

Your Homeowners Policy Stops Working the Moment You Rent

Your homeowners policy was written to protect owner-occupied residences, not rental investments. The moment a tenant signs a lease, your standard homeowners coverage becomes invalid for that property. Insurance companies treat rental properties as commercial ventures with higher risk profiles than owner-occupied homes. A tenant injury, stolen appliance, or months of vacancy create exposures that homeowners underwriting never contemplated. Washington property owners who discover this gap only after a loss occurs face complete financial exposure-and by then it is too late.

Liability Coverage Vanishes for Tenant Injuries

The liability section of your homeowners policy explicitly excludes injuries to people who rent your property. If a tenant falls on your deck, gets hurt by a malfunctioning heater, or claims the property caused illness, your homeowners insurer will deny the claim outright. Courts in Washington have upheld these exclusions repeatedly because the policy language is clear: coverage applies only to owner-occupied dwellings. A single tenant injury lawsuit can result in significant legal and settlement costs, and that money comes directly from your pocket without insurance protection. Rental property insurance provides liability coverage for single-family rentals, with multifamily buildings requiring higher limits depending on unit count and local risk factors.

Lost Rental Income Receives Zero Protection

Your homeowners policy ignores lost rental income entirely, treating the property as a structure rather than an income-producing asset. When a fire, severe weather, or pipe burst makes a unit uninhabitable, your mortgage and property taxes keep coming due while tenant rent stops arriving. Landlords face substantial financial pressure during extended vacancies, yet homeowners policies offer zero reimbursement for this income gap. Rental property insurance includes loss-of-income coverage that replaces your actual rental revenue while repairs happen, typically covering 12 to 24 months of lost rent depending on the policy. This protection preserves your cash flow during the restoration period and prevents you from tapping savings or taking loans to cover fixed expenses.

Tenant-Caused Damage Falls Outside Standard Coverage

Damage from tenant actions-deliberate vandalism, negligent water leaks, or theft-falls outside homeowners coverage because the policy assumes you occupy the property and control its use. Tenants damage rental units far more frequently than owner-occupants damage their own homes, making this exclusion substantial. A single burst pipe costs $3,000 to $25,000 in repairs, and if the damage makes the unit uninhabitable, you lose rental income immediately. Standard homeowners policies will not pay for any of this because the property is occupied by tenants, not you. Rental property insurance covers these exact scenarios-the three areas where rental claims occur most often (liability, income loss, and tenant-caused damage).

Understanding Your Coverage Gap Matters Now

Washington property owners who rely on homeowners policies for rental units face complete financial exposure. The exclusions are not ambiguous or subject to interpretation; they are explicit and enforceable. Your next step involves selecting the right rental property insurance form and coverage limits that match your specific property type and local risk exposure.

How to Pick the Right Policy for Your Washington Rental

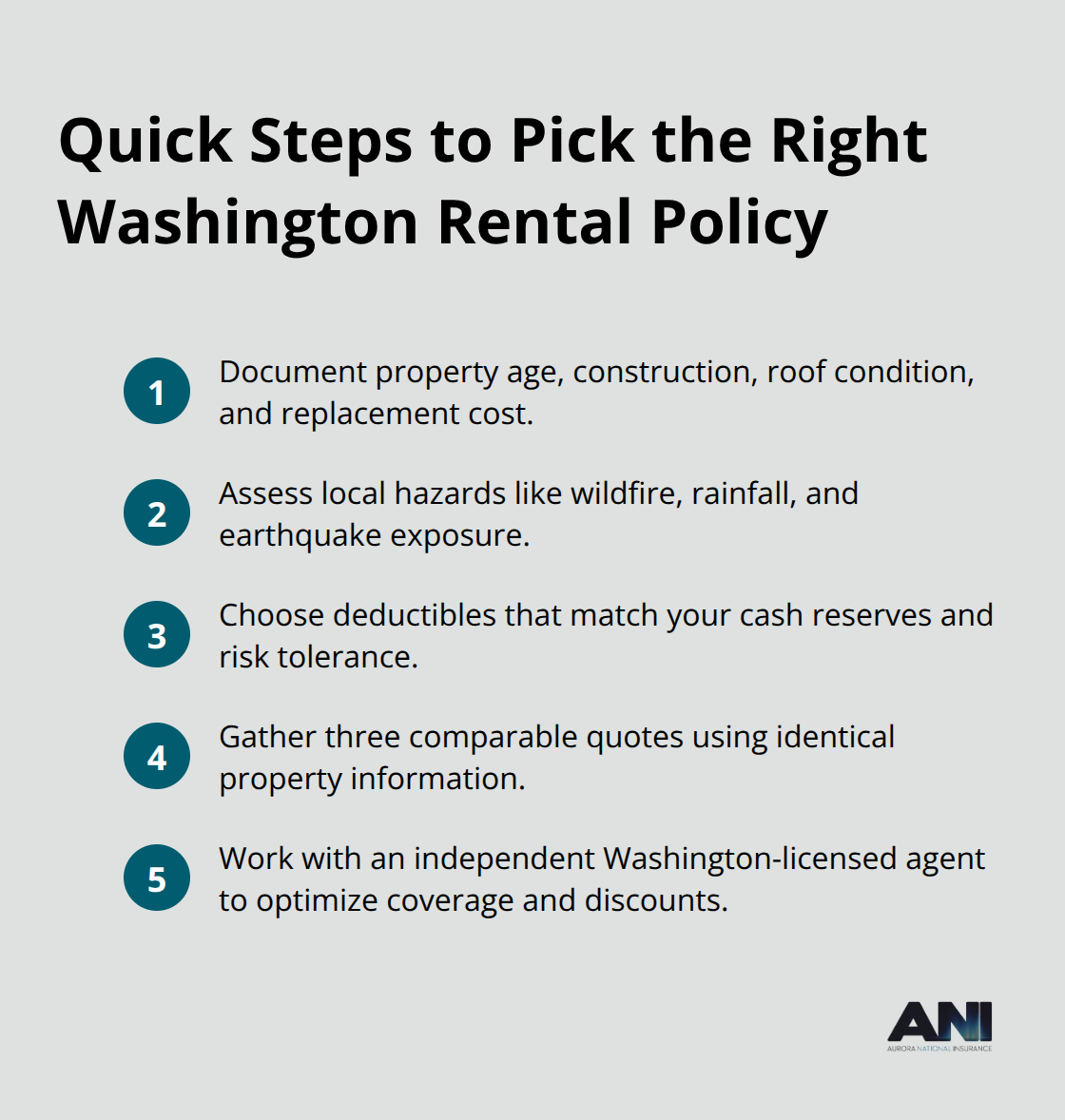

Start With Your Property Details

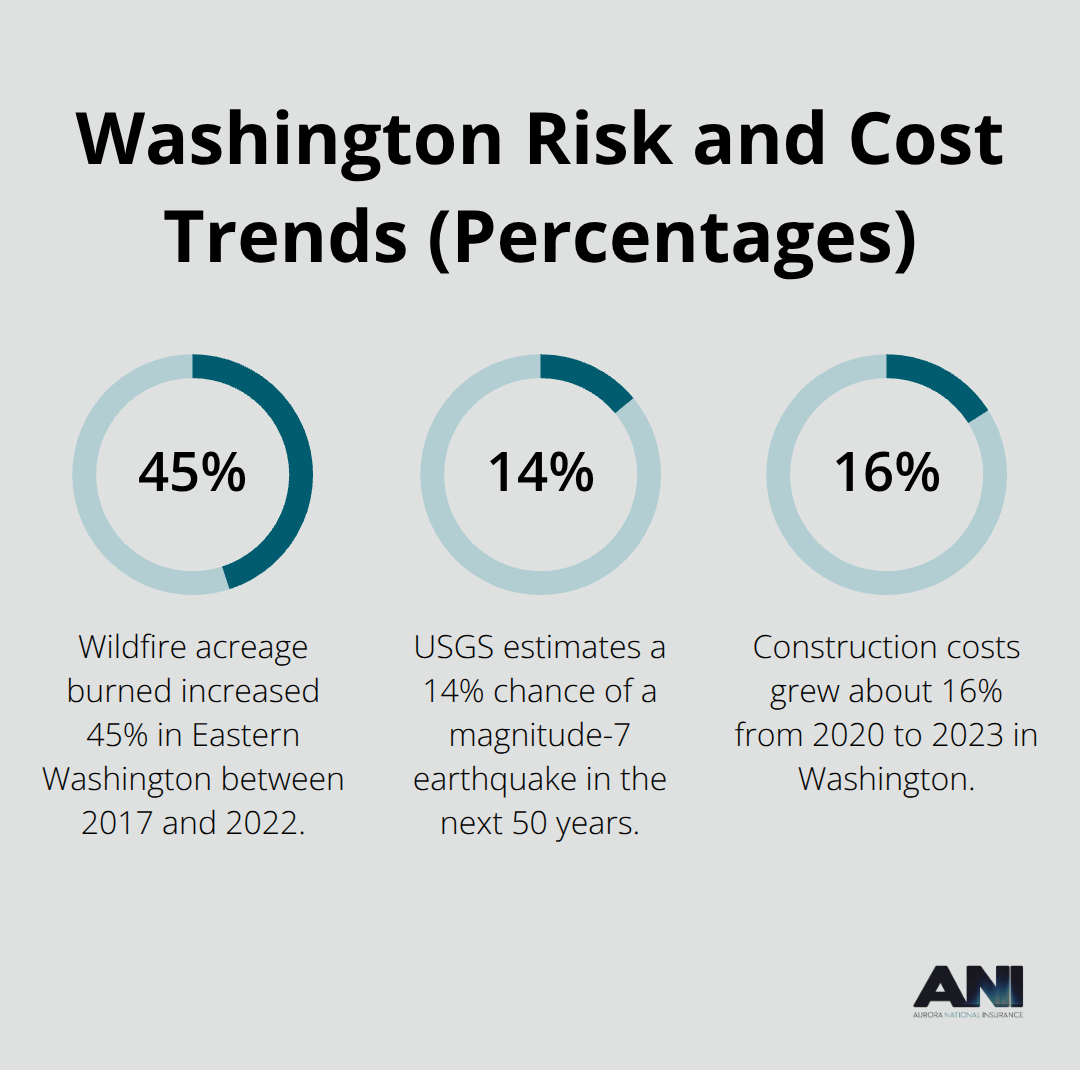

Your property specifics determine coverage needs because a single-family home in Spokane requires different protection than a four-unit building in Seattle. Document the dwelling’s age, construction type, roof condition, and replacement cost before requesting quotes. Properties with roofs older than ten years almost always need DP-3 coverage instead of DP-1 or DP-2 because DP-3 provides open-perils protection with customizable endorsements that match aging structures. Calculate your actual replacement cost by researching local construction expenses; the Associated General Contractors of Washington reported construction costs grew about 16 percent from 2020 to 2023, meaning your repair estimates from three years ago are now substantially outdated.

Assess Your Specific Hazard Exposure

Eastern Washington property owners face wildfire risk that increased 45 percent in acreage burned between 2017 and 2022, requiring smoke damage coverage that extends beyond on-premises events. Western Washington landlords encounter heavy rainfall and Cascadia earthquake risk that demands loss-of-income protection lasting at least six months and serious consideration of standalone earthquake coverage. The United States Geological Survey estimates a 14 percent chance of magnitude-7 earthquakes in the next 50 years, and earthquake damage runs $50,000 to $150,000+ per unit, making this exposure impossible to ignore.

Set Your Deductible Strategy

Calculate your maximum acceptable out-of-pocket loss before a claim occurs; if you cannot absorb $5,000 in repairs yourself, you need lower deductibles even if premiums cost more. Conversely, if you maintain substantial reserves, raising your deductible from $1,000 to $2,500 yields roughly 12 percent premium savings.

Obtain Multiple Quotes and Compare Carefully

Obtain at least three quotes from different carriers because premium variations for identical coverage often exceed 30 percent. Provide each insurer with identical property information including square footage, year built, number of units, roof age, and loss history to ensure apples-to-apples comparisons. Request explicit coverage details for water damage, vandalism, theft, and loss of rent duration since these vary significantly between DP-1, DP-2, and DP-3 forms. Ask specifically about exclusions for cannabis cultivation, short-term rentals like Airbnb properties, and vacant units because Washington’s legal environment creates coverage gaps that standard policies do not address.

Work With Independent Agents Licensed in Washington

Verify that liability limits match your property type; single-family rentals typically need $500,000 minimum, while multifamily buildings with four or more units require $1,000,000 or higher depending on tenant density and local lawsuit frequency. Consider adding umbrella coverage of $1,000,000 or more for multifamily properties because a single serious injury claim can exhaust standard liability limits quickly. Work exclusively with independent agents licensed in Washington who represent multiple carriers rather than captive agents working for single insurers. Independent agents shop your property across numerous companies simultaneously, identifying discounts for security systems, seismic shut-off valves, monitored alarms, and sprinkler systems that can reduce premiums by 5 to 12 percent. Some Washington counties offer up to 20 percent credits for sprinkler systems in multifamily buildings, savings that captive agents often miss entirely. Avoid online quote tools that lack human review because they frequently misclassify properties or miss endorsements critical for Washington’s unique risks. Your agent should explain exactly why DP-3 costs more than DP-2 and whether that additional expense justifies the broader protection for your specific property and financial situation.

Final Thoughts

Washington rental property insurance protects your income stream and equity when tenant injuries, property damage, or weather events strike. Standard homeowners policies leave you completely exposed in these situations, forcing you to cover liability claims, repairs, and lost rent from your own pocket. A single tenant injury lawsuit costs $50,000 to $300,000, a burst pipe runs $3,000 to $25,000 in repairs, and a six-month vacancy in Seattle eliminates over $13,000 in gross revenue-these scenarios happen regularly across Washington’s rental market.

Document your property details including age, construction type, roof condition, and replacement cost before requesting quotes. Assess your specific hazard exposure based on location: eastern Washington properties need wildfire coverage, western Washington rentals require earthquake consideration, and all Washington landlords should plan for loss-of-income protection lasting at least six months. Calculate your maximum acceptable deductible based on your financial reserves, then obtain at least three quotes from different carriers using identical property information to ensure accurate comparisons.

Work with independent agents licensed in Washington like Aurora National Insurance who represent multiple carriers rather than single insurers. These agents shop your property across numerous companies, identify discounts for security systems and monitored alarms that reduce premiums by 5 to 12 percent, and explain exactly why DP-3 coverage costs more than DP-2 and whether that expense justifies broader protection for your situation. Get started today with an instant online quote and take control of your rental investment’s financial security.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.