Anchorage Home Insurance Rates: Finding Affordable Local Coverage

Anchorage home insurance rates vary widely depending on where you live and what risks your home faces. Alaska’s severe weather, from heavy snow to earthquakes, directly impacts what you’ll pay for coverage.

At Aurora National Insurance, we help homeowners cut through the confusion and find policies that actually fit their budgets. This guide walks you through what drives your premiums and how to lower them without sacrificing protection.

What Drives Your Anchorage Home Insurance Costs

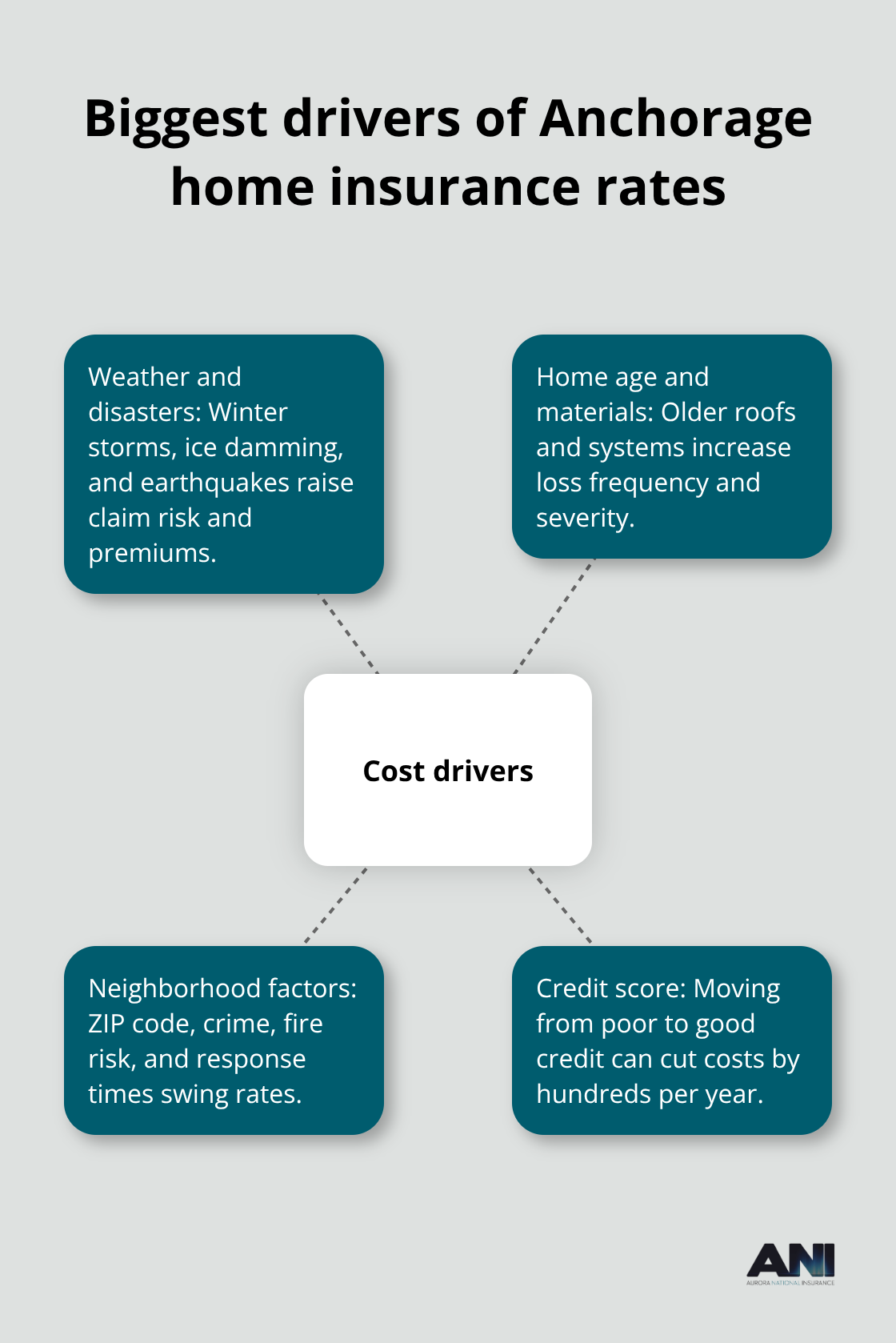

Alaska’s Weather and Natural Disasters Create Real Costs

Alaska’s weather creates real financial pressure on homeowners. Winter storms, heavy snow loads, and ice damming cause significant structural damage each year. The Cold Climate Housing Research Center found that ice damming results from air leaks, insufficient insulation, and improper ventilation-problems that lead directly to roof and water damage claims. Anchorage also faces earthquake risk, though standard homeowners policies exclude earthquake damage entirely. You need a separate earthquake endorsement, which typically carries a deductible around 10% of your home’s value. This means a $300,000 home could require a $30,000 deductible for earthquake coverage.

Flood damage presents another gap in standard policies. The National Flood Insurance Program notes that typical homeowners policies don’t cover flooding, and FEMA flood maps should guide your assessment of local risk. If your property sits in a flood zone, private flood insurance or NFIP coverage becomes essential, though coverage doesn’t start for 30 days after purchase.

Home Age and Construction Materials Impact Your Premium

Home age and construction materials matter far more than many homeowners realize. MoneyGeek’s analysis shows that a home built in 1980 costs roughly 53% more to insure than an identical 2020 home-about $1,446 versus $944 annually. Older roofing, outdated electrical systems, and deteriorated foundations increase claim frequency and severity. Insurers charge more for these homes because they pose higher risk.

Your Anchorage Neighborhood Determines Your Rate

Your location within Anchorage creates the biggest rate swings. The Zebra’s data across 83 million insurance rates nationwide shows ZIP code 99516 averages about $911 annually, while 99503 reaches $1,074-a difference of $163 per year for the same coverage. Anchorage’s overall average sits around $995 per year according to NerdWallet, but this masks significant neighborhood variation driven by local crime rates, fire risk, and emergency service proximity.

Credit Score Affects Your Bottom Line More Than You Think

Your credit score heavily influences pricing. MoneyGeek found that poor credit can push premiums to $1,985 yearly versus $1,004 for excellent credit-nearly double the cost. This 53% spread means improving your credit from poor to good could save roughly $981 annually on the same policy. These rate differences exist because insurers view credit as a predictor of claim behavior and financial responsibility.

Understanding these cost drivers helps you identify which factors you can control and which ones require different solutions. Choosing a local insurance agency can help you navigate these variables and find policies that match both your protection needs and your budget.

How to Compare Home Insurance Quotes in Anchorage

Get Multiple Quotes From Different Carriers

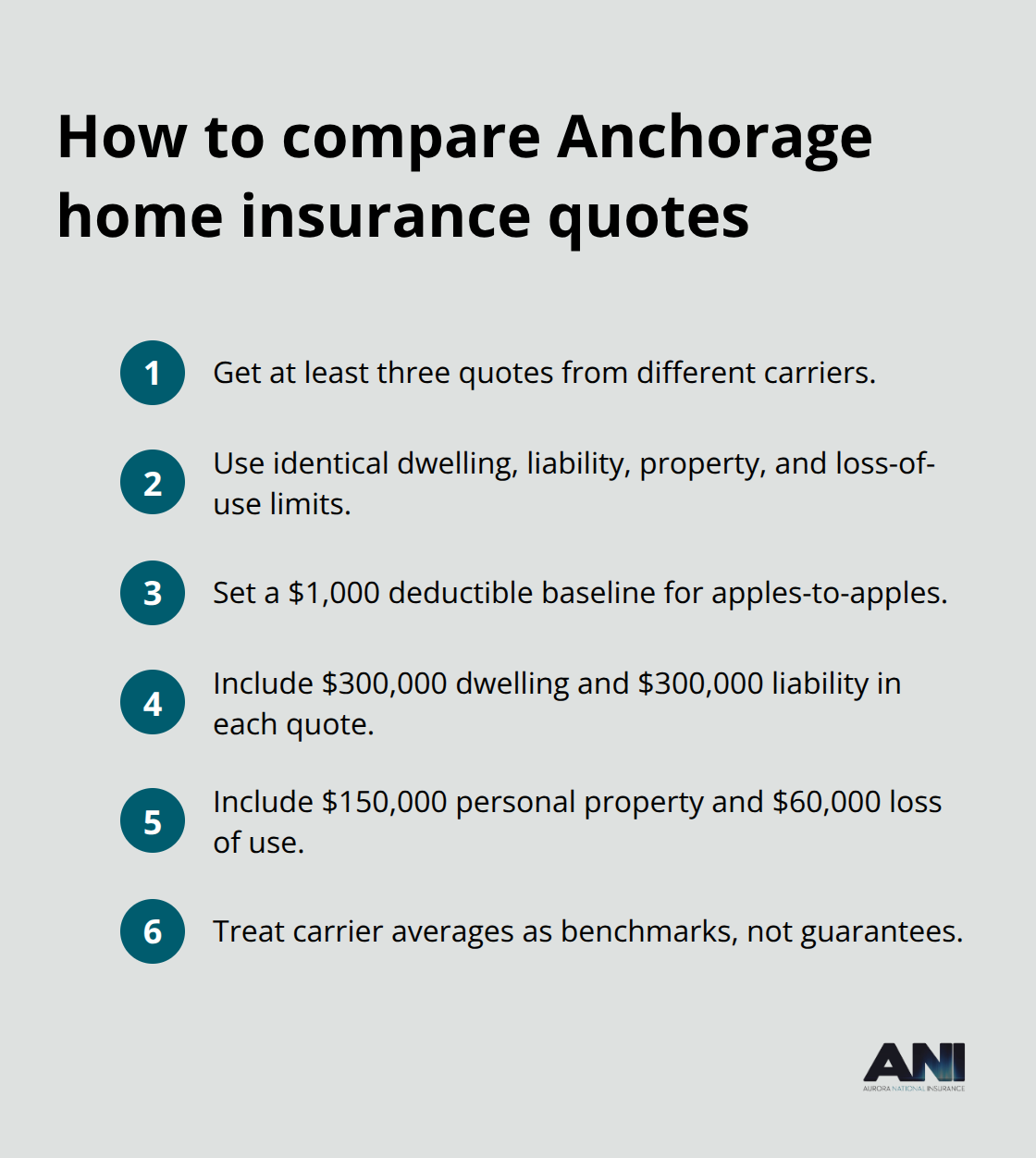

Shopping for Anchorage home insurance without comparing multiple carriers leaves money on the table. The Zebra’s analysis of over 83 million insurance rates shows that price gaps for identical coverage in Alaska can be nearly fourfold-some insurers quote $74 per month while others charge $268 for the same protection. This massive spread means you need at least three quotes to find real savings. When you request quotes, standardize the comparison across all carriers. Use identical coverage limits: $300,000 dwelling coverage, $300,000 liability, $150,000 personal property, $60,000 loss of use, and a $1,000 deductible as your baseline. This consistency reveals real price differences rather than mixing different coverage levels.

Liberty Mutual, Country Financial, and State Farm consistently offer affordable Anchorage options, with Liberty Mutual averaging around $739 yearly, Country about $784, and State Farm near $830 according to The Zebra’s data. However, affordability varies by your specific ZIP code and home characteristics, so treat these averages as benchmarks only. Regional carriers like Umialik Insurance average around $74 monthly in Alaska-substantially lower than household names-yet many Anchorage homeowners never consider them simply because they’re unfamiliar.

Understand What Each Policy Covers

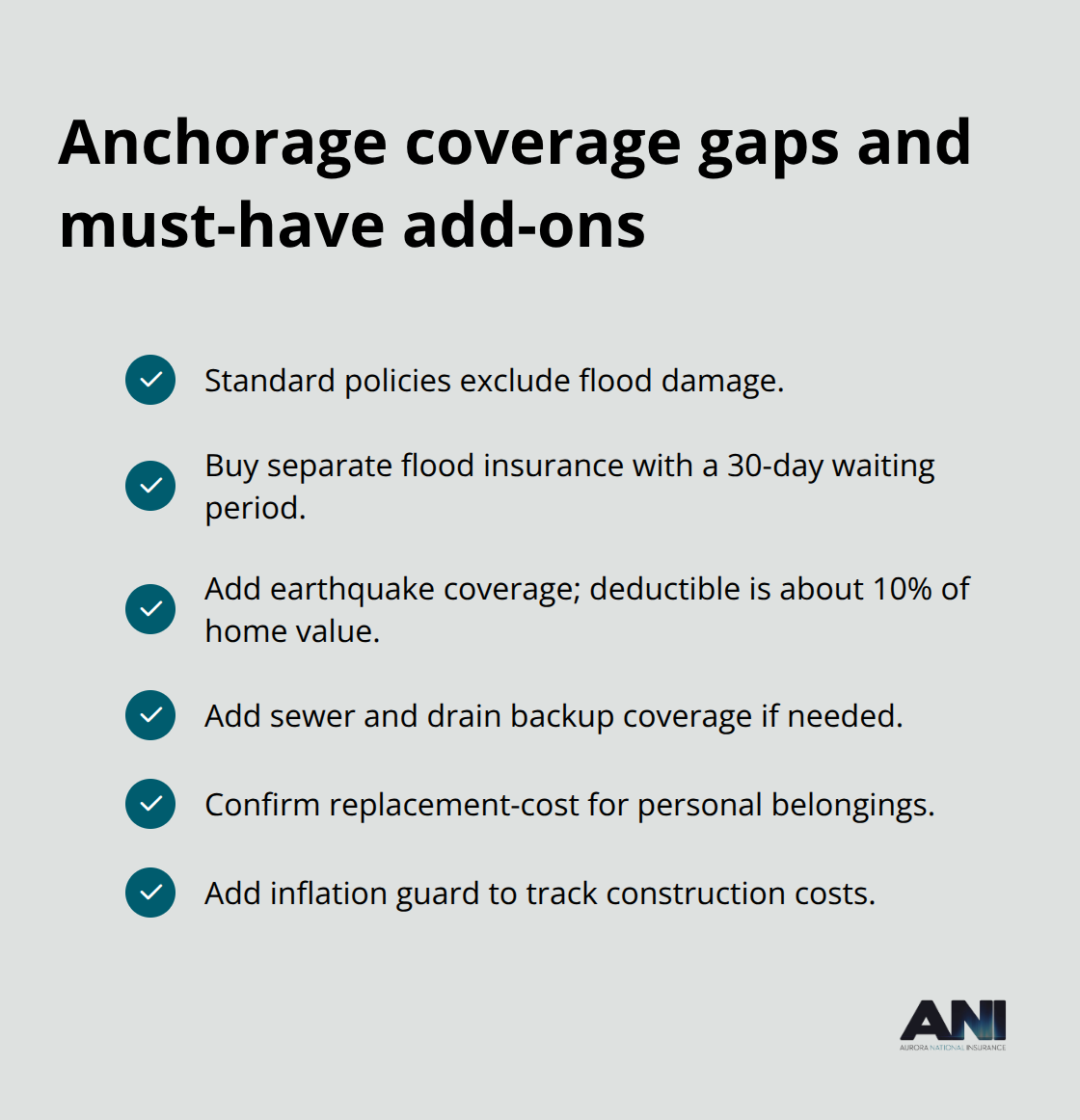

Standard homeowners policies exclude critical Anchorage risks, so examine coverage details carefully. Flood damage isn’t covered by any standard policy-you need separate flood insurance with its typical 30-day waiting period. Earthquake coverage requires an additional endorsement carrying roughly a 10% deductible on your home’s value. Water damage from sewer or drain backups needs specific coverage that many basic policies omit.

When comparing quotes, verify whether each policy includes replacement-cost coverage for personal belongings, which pays what items cost today rather than their depreciated value. Check if the policy offers inflation guard riders that automatically increase your dwelling coverage annually to match construction cost inflation. Ask each carrier about available discounts-bundling home and auto typically saves 10% to 25% on both policies, while security systems, smoke detectors, and newer roofs can reduce premiums by 10% to 20%.

Look Beyond Price to Find Real Value

The cheapest quote doesn’t always deliver the best protection. NerdWallet’s analysis weights consumer experience, financial strength, coverage options, and available discounts when rating Alaska insurers, with Chubb, USAA, and State Farm earning the highest marks. A carrier that charges $50 less annually but offers weaker coverage or slower claims service costs you more in the long run.

Request quotes from carriers you’ve never heard of alongside the major names. This approach exposes you to regional options that often undercut national competitors. The final step involves verifying that each carrier actually issues new policies in Anchorage, since some insurers have stopped accepting new customers in Alaska. Once you’ve narrowed your choices to three finalists, contact each one directly to confirm current availability and ask about any additional discounts specific to your situation (such as military service, professional affiliations, or home improvements you’ve completed).

Ways to Lower Your Anchorage Home Insurance Premiums

Increase Your Deductible to Cut Annual Costs

The most direct way to lower your Anchorage premiums is to increase your deductible, and the numbers prove this strategy works. Increasing your deductible from $500 to $2,000 can significantly reduce your annual costs. This approach works because you accept more financial responsibility for small claims, which insurers reward with lower rates. The catch is simple: only increase your deductible if you can actually afford to pay it out of pocket when a claim happens. A $5,000 deductible saves money only if you have $5,000 in emergency savings available. If you’d struggle to cover that amount, stick with a $1,000 or $1,500 deductible instead.

Bundle Home and Auto Policies for Immediate Savings

Bundling your home and auto policies with the same insurer delivers immediate savings without requiring you to accept more risk. Bundling typically reduces your combined premium by 10% to 25% according to insurance data, which translates to real dollars across both policies. In Anchorage, bundling home and auto saves about 10% on average. State Farm customers who bundle pay roughly $977 for auto coverage, while those purchasing policies separately pay significantly more. USAA bundled rates sit around $825 for auto, and Allstate bundled customers see combined savings that make the two-policy approach substantially cheaper than separate quotes. The reason is straightforward: insurers want to retain customers across multiple products because it reduces their acquisition costs and increases customer lifetime value. Before you bundle, however, compare the bundled price against separate quotes from competitors-occasionally a different carrier offers better rates on one policy even if their bundle price seems attractive.

Install Security Systems and Upgrade Home Components

Security systems, fire alarms, and smoke detectors reduce your premiums by 10% to 20%, according to insurance industry data. These improvements work because they lower claim frequency and severity. A monitored security system that connects to local police reduces theft and break-in losses. Fire detection equipment catches problems early, preventing total loss situations. The investment typically costs $300 to $1,000 for a basic system, but the annual savings of $100 to $200 means the system pays for itself within five years. Newer roofs also qualify for discounts-replacing a roof before it fails signals to insurers that you maintain your home responsibly. Home age drove the biggest cost differences in our earlier discussion, but upgrading key components like roofing, electrical systems, or plumbing can offset some of that age-related premium burden. Ask your insurer specifically which improvements they’ll discount before you invest in upgrades.

Final Thoughts

Finding affordable Anchorage home insurance rates requires you to take three concrete actions. First, request quotes from at least three different carriers and compare them using identical coverage levels, since price gaps for the same protection can exceed 300 percent. Second, increase your deductible if you have emergency savings to cover it, bundle your home and auto policies, and install security systems or upgrade your roof-these moves typically save 10 to 25 percent on your premiums.

Alaska’s weather, your home’s age, and your neighborhood within Anchorage create the biggest cost drivers. You cannot change where you live or your home’s construction year, but you can control your deductible, your credit score, and which insurer you choose. Improving your credit from poor to good could save nearly $1,000 annually on the same policy.

Local expertise makes the difference between finding adequate coverage and finding the right coverage at the right price. An independent agency rooted in Alaska understands how permafrost, ice damming, and earthquake risk affect your specific property and which carriers offer the best rates in your ZIP code. Get an instant online quote to see how much you can save by working with agents who understand Anchorage’s unique risks and your budget constraints.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.