Portland Homeowners Insurance Quotes: Fast Local Quotes for Your Home

Portland homeowners face real risks from heavy rainfall, windstorms, and occasional earthquakes. Getting Portland homeowners insurance quotes from multiple providers is the fastest way to find coverage that fits your needs and budget.

At Aurora National Insurance, we help homeowners understand what protection actually costs in your area. This guide walks you through getting quotes quickly and spotting coverage gaps that could leave you exposed.

Why Portland Homeowners Need Insurance Quotes

Real Risks Shape Local Insurance Costs

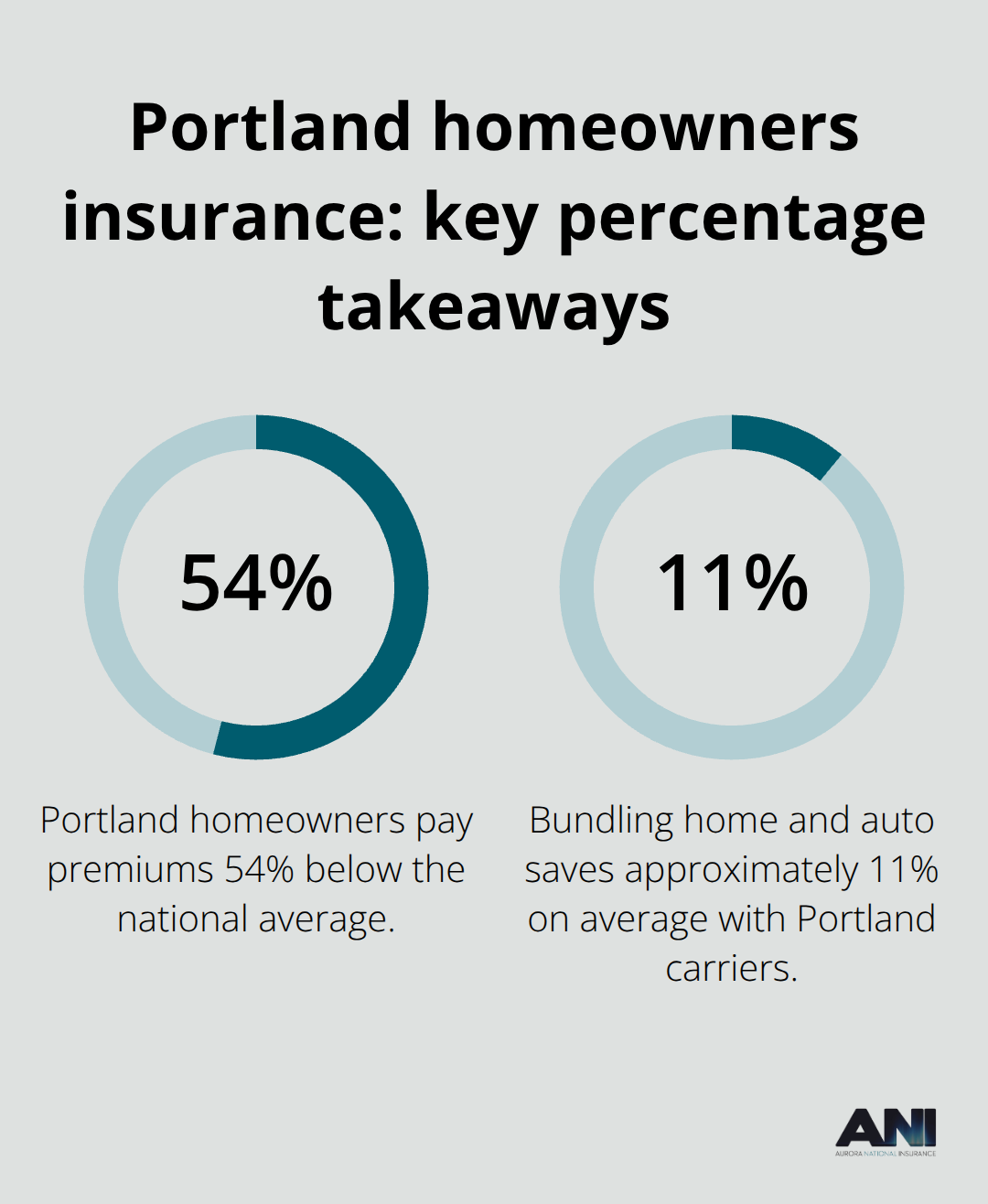

Portland’s weather patterns create genuine insurance needs that most homeowners underestimate. Heavy rainfall causes water damage, windstorms topple trees and damage roofs, and occasional earthquakes threaten structural integrity. The risk isn’t theoretical-it’s baked into local premiums. Portland homeowners pay an average of $801 per year for coverage, which is 54% below the national average but still represents a significant expense that deserves careful attention.

Why Quotes Vary So Dramatically

Different insurers price these regional risks differently, meaning two quotes for identical homes can vary by hundreds of dollars annually. Multiple quotes reveal which carriers actually understand Portland’s specific hazards versus those applying generic pricing. The cheapest option in Portland comes from Mutual of Enumclaw Insurance at around $397 per year, while Allstate averages $1,034 per year for similar coverage-a $637 annual difference for the same protection level.

Coverage Gaps That Cost You Money

Your coverage choices matter equally. Standard homeowners policies protect against fire, wind damage, and theft, but they don’t cover flooding-a critical gap given Portland’s rainfall patterns. Water backup coverage, which handles damage from sewage or storm drain backups, is especially valuable for Portland-area properties and often costs just $50 to $100 annually to add. Earthquake coverage is optional but worth considering given Oregon’s seismic activity, though it requires a separate endorsement since standard policies exclude it.

How Your Home’s Details Drive Price

Dwelling coverage directly drives premiums upward. Deductible selection dramatically impacts your annual cost. Choosing a $1,000 deductible instead of $500 saves roughly $100 annually, and jumping to $2,000 saves another $80. The trade-off is clear: higher deductibles lower your monthly burden but increase what you pay out-of-pocket if you file a claim.

Your home’s age and construction matter too. Older homes cost more to insure because replacement materials and labor are more expensive. Bundling home and auto insurance saves approximately 11% on average across Portland carriers, which translates to hundreds of dollars annually. Comparing quotes forces you to articulate what coverage actually matters for your situation. Many Portland homeowners discover they’re either overinsured for their needs or carrying dangerous gaps.

What Fast Quotes Actually Reveal

This isn’t about finding the cheapest option-it’s about matching protection to your home’s actual value and your financial capacity to handle losses. Once you understand how your specific home influences price, you’re ready to move forward with the actual quote process.

How to Get Fast Online Quotes for Portland Homes

Organize Your Home Information First

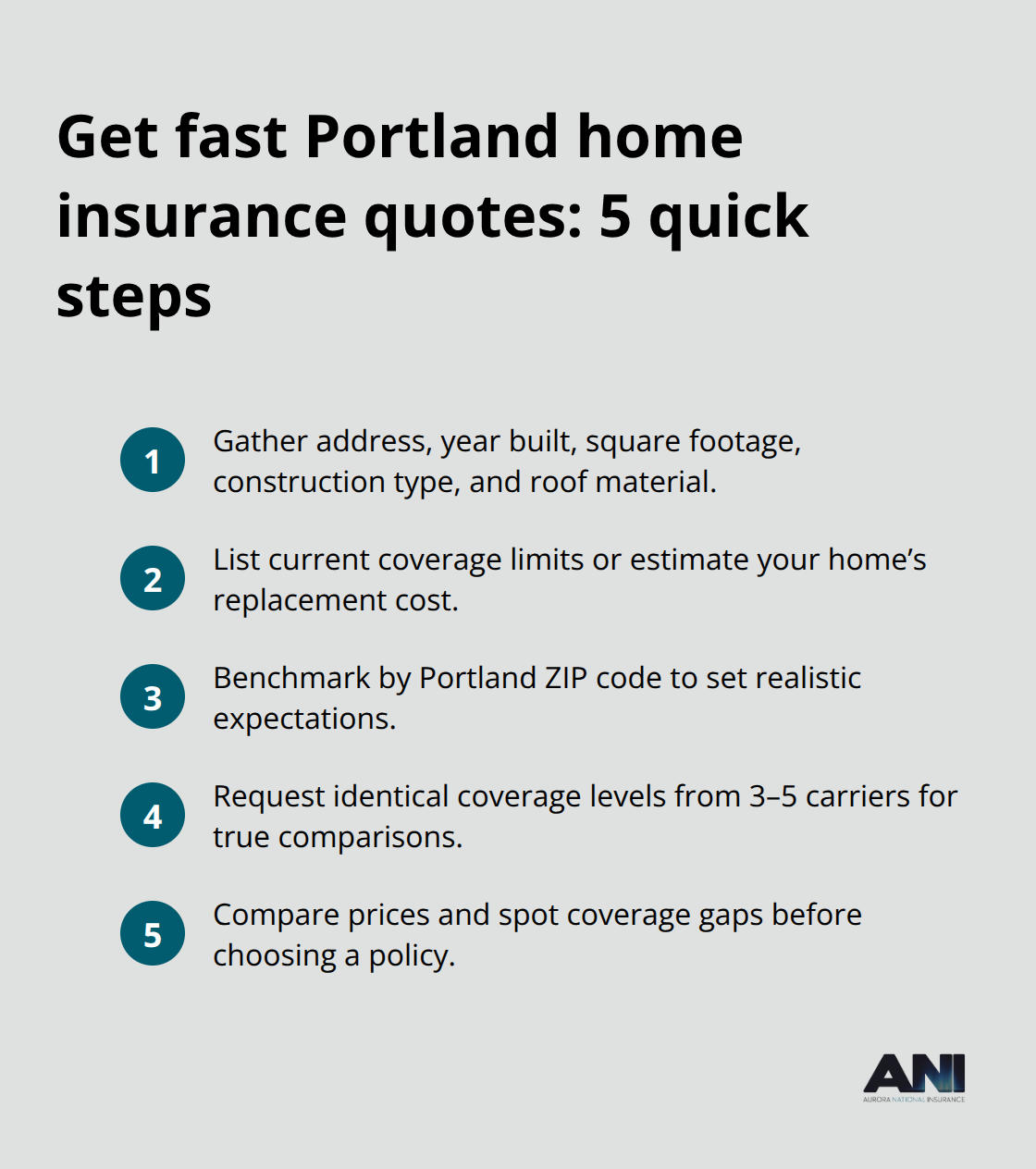

Collect your home’s address, year built, square footage, construction type (wood frame versus brick), and roof material before you request quotes. You’ll also need your current coverage limits if you’re switching insurers, or a rough estimate of your home’s replacement cost if you’re new to insurance. Most online quote tools ask for dwelling coverage amount, personal property limits, liability coverage, and your preferred deductible. Know what you’re currently paying if you have existing coverage-this context helps you spot whether a new quote represents genuine savings or just a lower coverage level.

Use Local Data to Benchmark Your Quotes

The Oregon Department of Insurance publishes statewide averages that help you benchmark quotes, but Portland-specific data matters more since ZIP code drives significant rate variation. Properties in 97217 and 97201 have different rate profiles, so checking your specific ZIP code helps set realistic expectations. Having this information upfront means you can request quotes from three to five carriers simultaneously rather than dragging the process across weeks.

Work with Local Portland Agents

Local Portland agents understand nuances that online tools miss. An agent can explain why water backup coverage costs extra but makes sense for your neighborhood’s drainage patterns, or why earthquake endorsements matter given Oregon’s seismic history. They can also identify bundling opportunities that save money when you combine home and auto policies. Most importantly, agents can access quotes from carriers you won’t find on generic comparison sites.

Request Quotes with Matching Coverage Details

Getting quotes typically takes 15 to 30 minutes per carrier when you have your information organized. Request quotes with identical coverage levels across all carriers so you’re actually comparing apples to apples-dwelling coverage, personal property, liability, and deductible amounts must match. This approach reveals which insurers genuinely price Portland’s risks lower versus those simply undercutting on coverage.

Compare Your Results and Identify Coverage Gaps

Once you have three to five quotes with matching details, you’ll notice patterns in how different carriers price your home. Some quotes will look attractive on price but offer thinner coverage, while others cost more because they include protections you actually need. This is where many Portland homeowners discover they’re either overinsured for their needs or carrying dangerous gaps that could expose them to significant financial loss.

Common Coverage Gaps Portland Homeowners Miss

Flood and Water Damage Protection

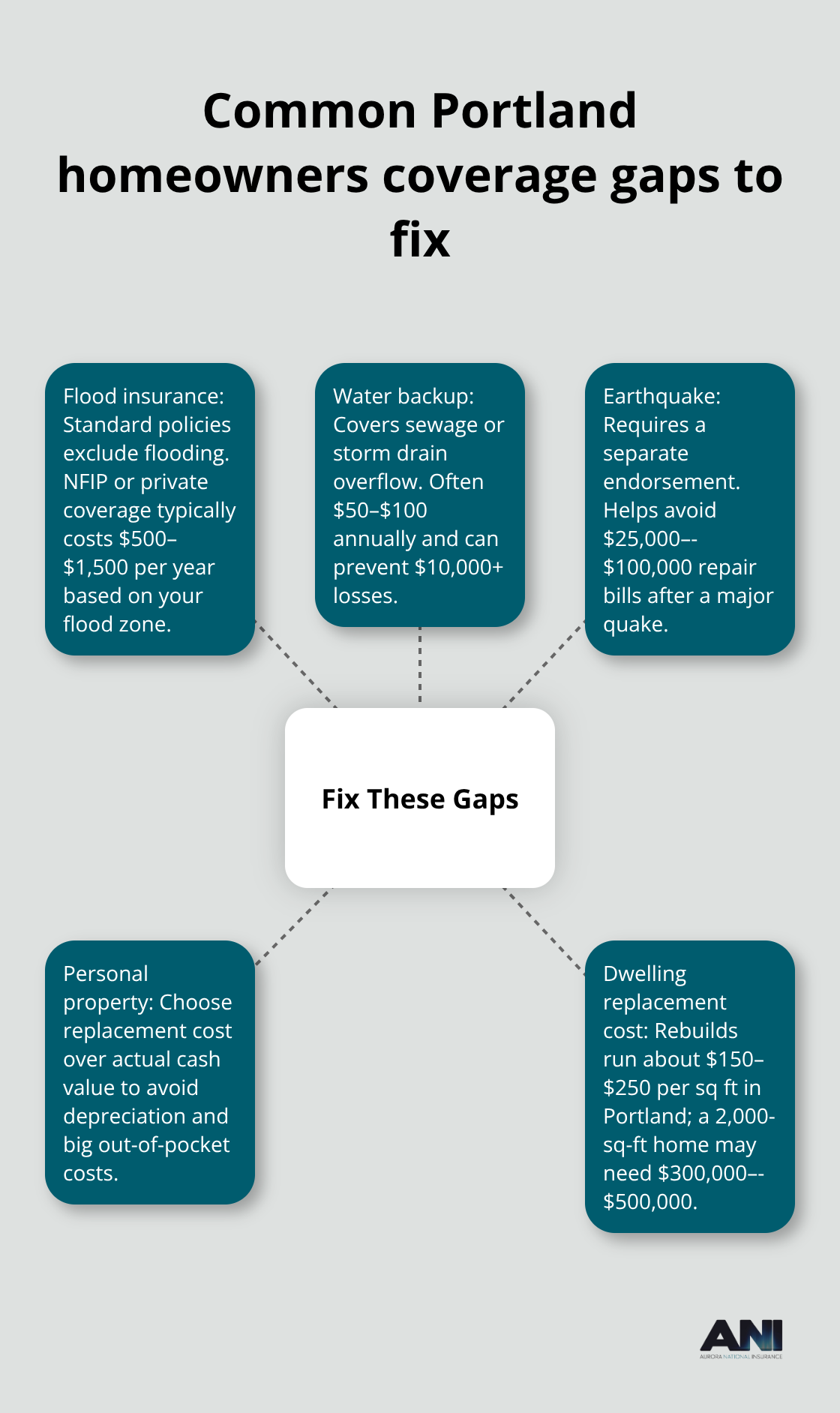

Most Portland homeowners discover their coverage gaps only after filing a claim. Standard policies protect against fire, wind, and theft, but they explicitly exclude flooding, which is the most common and costly disaster in the Pacific Northwest. Water damage from heavy rainfall costs Portland homeowners thousands annually, yet standard policies won’t cover it. Adding flood insurance requires a separate policy through the National Flood Insurance Program or private carriers, and it typically costs $500 to $1,500 annually depending on your flood zone.

If you live within a quarter-mile of the Willamette River or in areas prone to storm drain backups, flood insurance becomes a financial necessity rather than an optional add-on. Water backup coverage handles damage from sewage or storm drain overflow during heavy rains and costs only $50 to $100 annually to add. This modest expense prevents losses exceeding $10,000 in a single event, making it one of the smartest investments Portland homeowners can make.

Earthquake Coverage and Structural Risk

Earthquake coverage is similarly underestimated by Portland homeowners. Oregon experiences roughly 0.9 major seismic events per year according to NOAA data, yet most Portland homeowners skip earthquake endorsements because they assume the risk is minimal. A significant earthquake could cost $25,000 to $100,000 in structural repairs, and standard policies won’t cover a penny of it. This gap exposes you to catastrophic financial loss that a modest annual endorsement fee would prevent.

Personal Property and Replacement Cost Gaps

Personal property coverage limits create another dangerous gap in most Portland policies. Most homeowners insure for $50,000 to $100,000 in personal belongings, but they rarely inventory what they actually own. Electronics, furniture, clothing, and tools add up quickly, and replacement cost coverage (which pays what items actually cost to replace today) costs significantly more than actual cash value coverage (which deducts depreciation). The difference between these two options can mean paying $5,000 out-of-pocket after a theft or fire when replacement cost coverage would have covered the full amount.

How Local Agents Spot Your Specific Gaps

Local Portland agents identify coverage gaps by asking questions that online quote tools never do. They ask whether you work from home, which affects your liability exposure and may require a home-based business endorsement. They ask about expensive hobbies like woodworking or jewelry collecting, which need separate scheduling on your policy. They ask about rental income if you have a guest house or short-term rental, which requires completely different coverage than owner-occupied homes.

Agents examine your home’s specific characteristics-whether you have an older roof that’s more vulnerable to wind damage, whether your plumbing is original copper or updated PEX, whether your electrical panel is outdated. These details directly influence what additional protections make sense. A 1950s home with original plumbing faces higher water damage risk and benefits more from water backup coverage than a 2010 home with modern systems.

Dwelling Coverage and Replacement Cost Reality

Agents also verify whether your coverage limits match your home’s actual replacement cost. Many Portland homeowners base their dwelling coverage on their mortgage balance or purchase price, which often understate what it actually costs to rebuild. Replacement cost estimates in Portland run $150 to $250 per square foot for frame construction depending on finishes and location, meaning a 2,000-square-foot home costs $300,000 to $500,000 to rebuild after a total loss. If your dwelling coverage is only $200,000, you’re carrying massive underinsurance risk.

Local agents pull building cost data specific to Portland neighborhoods and compare it against your current coverage limits, revealing exactly where you’re exposed. This analysis prevents the financial devastation that occurs when homeowners discover their coverage falls far short of actual replacement costs.

Final Thoughts

Multiple Portland homeowners insurance quotes reveal how dramatically rates vary across carriers for identical coverage. Comparing three to five quotes takes less than an hour when you organize your home information upfront, and the savings often reach $200 to $300 annually. More importantly, this comparison forces you to examine your coverage honestly and identify gaps that could leave you financially exposed after a loss.

Local agents understand how your specific neighborhood’s flood risk, seismic activity, and building characteristics influence what coverage actually makes sense for your situation. They spot gaps that online quote tools miss, like the need for water backup coverage given Portland’s rainfall patterns or earthquake endorsements given Oregon’s seismic history. They also identify bundling opportunities that save hundreds annually when you combine home and auto policies.

At Aurora National Insurance, our licensed agents help Portland homeowners navigate this process and access quotes from multiple top-rated carriers. Start by gathering your home information and requesting quotes from local Portland agents today. The time investment pays for itself many times over through better coverage at competitive prices.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.