Seattle Landlord Insurance: Protecting Your Rental Property With Local Help

Owning rental property in Seattle comes with real financial exposure. Tenants, natural disasters, and liability claims can drain your savings fast if you’re not properly protected.

At Aurora National Insurance, we’ve helped countless Seattle landlords build coverage that actually matches their properties and local risks. The right Seattle landlord insurance policy stops small problems from becoming expensive disasters.

What Landlord Insurance Actually Covers

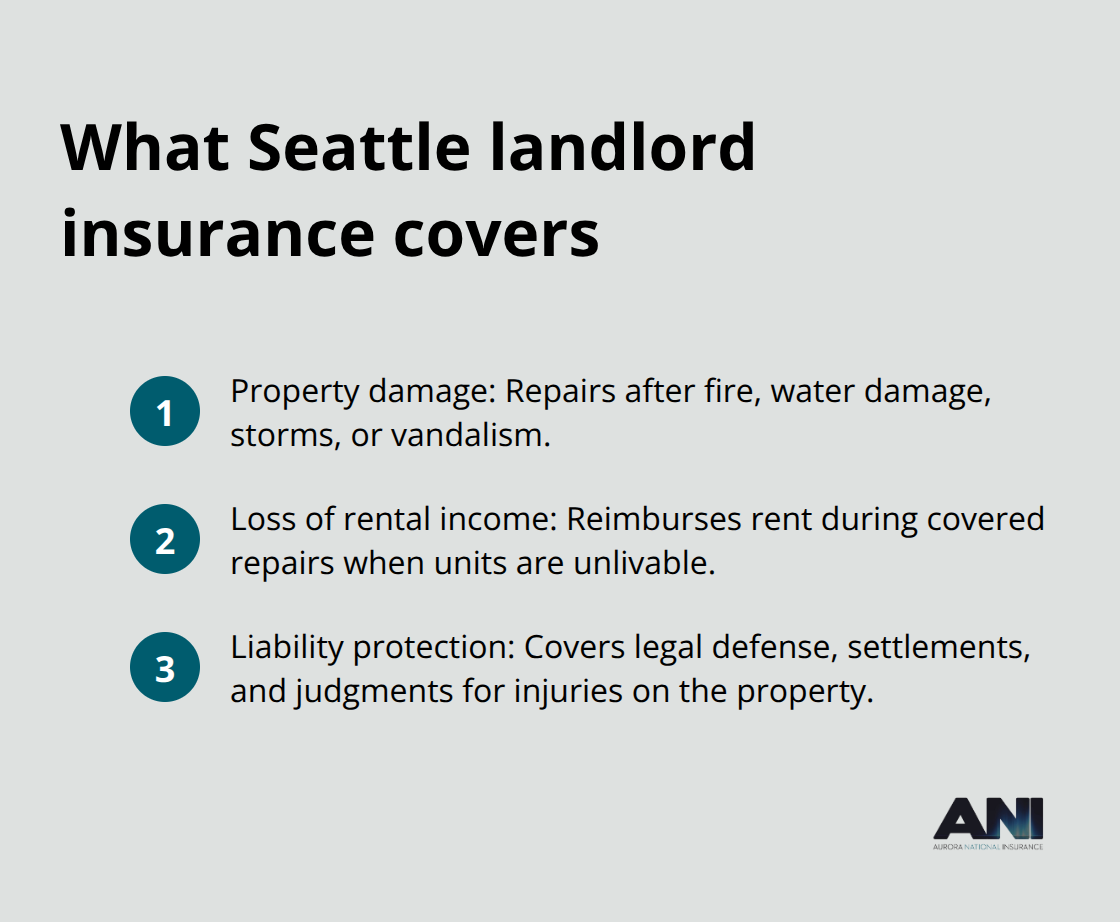

Landlord insurance protects the building itself, your rental income, and your liability exposure when someone gets injured on the property. This differs fundamentally from homeowners insurance, which stops working the moment you convert your home to a rental. Standard homeowners policies exclude tenant-caused damage, loss of rental income, and liability related to tenant injuries. Property owners often assume their existing homeowners policy will cover their rental, only to face a denied claim when disaster strikes. Property damage coverage pays for repairs after fire, water damage, storms, or vandalism. Loss of rental income coverage reimburses the rent you would have collected during repairs after a covered event, protecting your cash flow when the property is temporarily unlivable. Liability protection covers legal costs, settlements, and judgments if a tenant or guest is injured on the property-tenant injury claims can exceed $100,000 in medical and legal costs alone.

Coverage Limits Matter in Seattle’s High-Cost Environment

Seattle landlords should carry at least $500,000 per occurrence of liability, with $1,000,000 per occurrence recommended for larger portfolios. General liability limits of $300,000 to $500,000 per occurrence fall short in Seattle’s high-cost environment. Dwelling limits must reflect current reconstruction costs, not what you paid for the property years ago. Seattle rebuild costs run approximately $350 to $500 per square foot, so a 2,000 square foot building requires roughly $700,000 to $1,000,000 in coverage to actually rebuild after a total loss. Many landlords underestimate replacement costs and then face massive out-of-pocket expenses when a loss occurs. An umbrella liability policy of around $1,000,000 extends protection after underlying limits are exhausted; this typically costs roughly $200 to $400 per year and fills critical gaps that standard policies leave exposed.

Seattle-Specific Risks Require Specialized Coverage

Earthquake risk in the Cascadia region is significant, with about a 10 to 15 percent probability of a magnitude 9.0 event in the next 50 years according to the Washington Geological Survey. Standard landlord policies exclude earthquakes entirely, so you must add a separate endorsement if you want any protection. Flood coverage is similarly excluded from standard policies, yet a large portion of flood claims occur outside designated high-risk areas, meaning your property could flood even if flood maps suggest low risk. The National Flood Insurance Program offers flood protection, though note there is typically a 30-day waiting period before coverage takes effect. Older properties over 25 years old often require higher liability limits to obtain quotes at all, making maintenance documentation critical. Recent roof, plumbing, or electrical work can reduce premiums by about 5 to 10 percent, so obtain bids before renewal to prove risk reduction to your carrier. Multiple carriers offer different policy forms-DP-2 versus DP-3, for example, can differ by 15 to 25 percent in premium, with DP-3 typically offering broader coverage worth the extra cost for most Seattle landlords.

Next Steps in Building Your Protection Strategy

The coverage types and limits you select today directly impact how well your rental investment survives tomorrow’s unexpected events. Your property’s age, location, and tenant profile all influence which endorsements and limits make sense for your situation. A local insurance agent who understands Washington hazards and Seattle’s rental market can identify gaps that national carriers often miss, helping you avoid costly underinsurance.

Why Local Insurance Agents Understand Seattle’s Rental Market

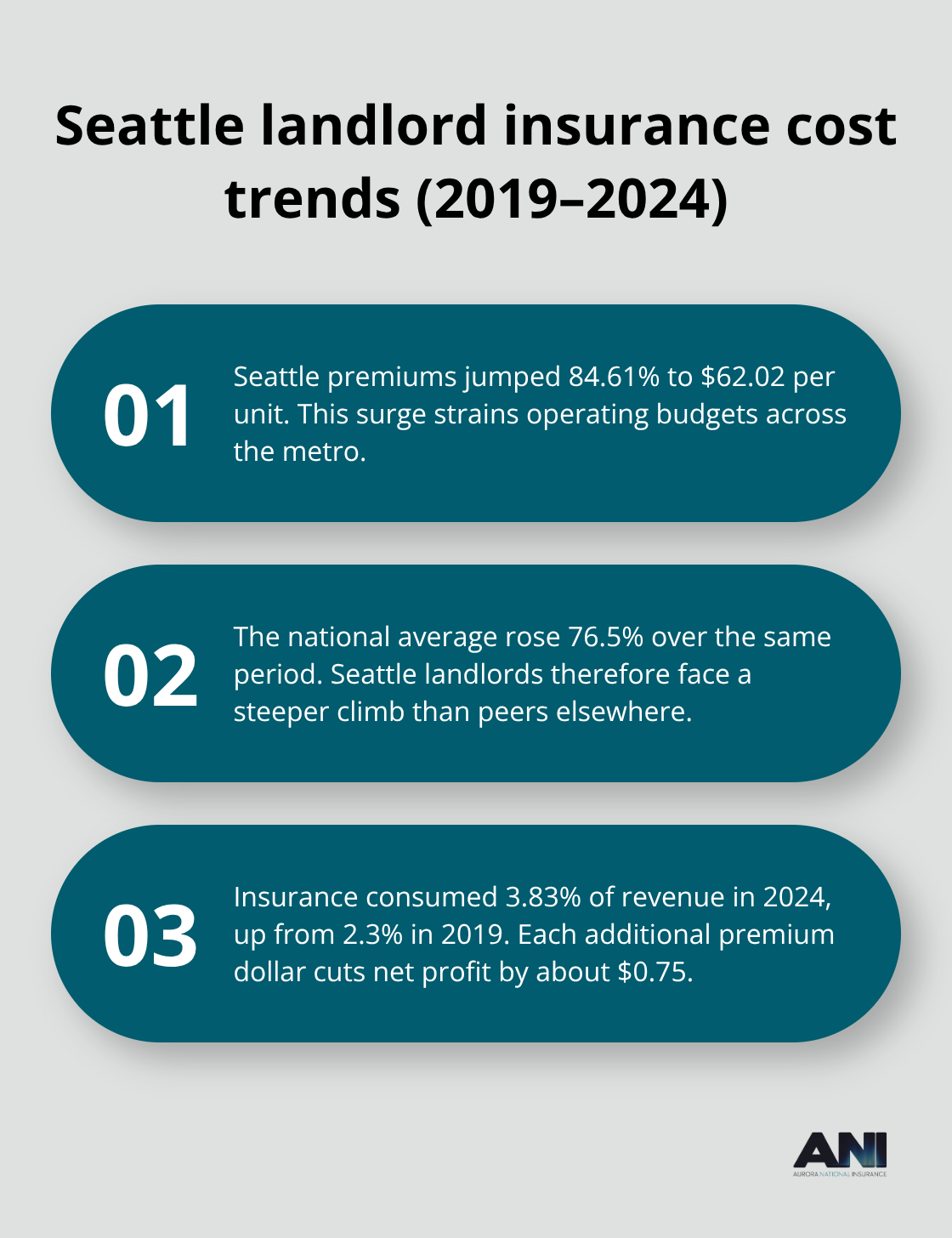

Insurance costs for Seattle landlords have skyrocketed. From 2019 to 2024, monthly insurance premiums per multifamily unit in the Seattle metro area jumped 84.61%, reaching $62.02 per unit, according to a Federal Reserve study compiled by Trepp that analyzed thousands of multifamily properties with commercial mortgage-backed securities loans. The national average rose 76.5% over the same period, meaning Seattle landlords pay significantly more than their counterparts elsewhere.

For each additional dollar spent on property insurance, a landlord’s net profit declines by about 75 cents. Insurance costs consumed 3.83% of revenue for a typical landlord in 2024, up from 2.3% in 2019. Washington State rental executives from the Washington Multifamily Housing Association attribute this spike to broader economic uncertainty and increased environmental risk. Landlords often cannot raise rents fast enough to offset these premiums due to market competitiveness, which intensifies the problem.

A national agent working from a script cannot explain why your Seattle property costs more to insure than an identical building in Phoenix, nor can they identify which specific local risks drive your quotes higher. Local agents understand that Seattle’s earthquake exposure and flood risk, aging building stock, and tenant demographics create pricing premiums that don’t apply elsewhere. They know which carriers price aggressively in Washington versus those that avoid the market entirely. They can explain why your 1970s building requires different liability limits than a new construction property, and they understand how Washington’s landlord-tenant laws affect your coverage needs.

Washington Tenant Laws Shape Your Coverage Requirements

Washington State imposes strict landlord responsibilities that directly impact your insurance strategy. Landlords must maintain habitable premises under Washington law, which means your policy must cover the repairs needed to restore habitability after a covered loss. Loss of rental income coverage becomes essential because you cannot legally collect rent from uninhabitable units during repairs, even if the tenant remains on site. If a tenant is injured due to your negligence in maintaining the property, Washington’s premises liability standards expose you to significant claims. A local agent knows how courts in King County and surrounding areas interpret these duties and can recommend liability limits that reflect actual exposure rather than generic minimums. They understand which endorsements strengthen your position if a tenant dispute reaches litigation. National carriers sometimes apply generic policy language that conflicts with Washington State requirements, creating coverage gaps that only surface during a claim. Local agents catch these mismatches before they cost you money.

Property-Specific Risk Assessment Requires On-the-Ground Knowledge

Your property’s actual risk profile depends on factors that national databases miss. An agent who understands Seattle’s neighborhoods knows that a rental in Ballard faces different flood exposure than one in Capitol Hill, even though both are Seattle addresses. They can evaluate whether your specific building’s age, construction type, and roof condition warrant the higher liability limits that older properties typically require. They know which maintenance improvements actually lower premiums with specific carriers and which improvements insurance companies ignore. A local agent can assess whether your property sits in a liquefaction zone or landslide area, information that affects both pricing and coverage availability. They understand tenant demographics in your building and how that influences loss history and claims frequency. They can review your current coverage and identify whether you pay for protection you don’t need or leave dangerous gaps in coverage you do need. This assessment takes a site visit or at minimum a detailed conversation about your specific property-something impossible with an online quote engine. The cost difference between a policy that matches your actual risk and one that doesn’t often exceeds $500 to $1,000 annually, making local expertise financially valuable rather than merely convenient.

How Local Agents Navigate Carrier Selection

Different insurance carriers price Seattle properties differently based on their appetite for Washington risk. Some carriers actively compete for Seattle multifamily business while others have pulled back entirely, which means your agent’s carrier relationships directly affect the quotes you receive. A local agent knows which carriers offer the best rates for older buildings, which ones specialize in higher-liability situations, and which ones provide the most responsive claims service when you need it. They can compare DP-2 versus DP-3 policy forms and explain why the 15 to 25 percent premium difference matters for your specific property. They understand how recent roof, plumbing, or electrical work affects pricing with each carrier (improvements can reduce premiums by about 5 to 10 percent). National online platforms cannot replicate this carrier knowledge because they lack the relationships and market intelligence that local agents develop over years of working in Washington. Your agent’s ability to shop multiple carriers and negotiate terms directly impacts both your premium and your coverage quality.

Moving Forward With Confidence

The right local agent transforms insurance from a confusing expense into a strategic asset that protects your rental investment. They identify coverage gaps before claims happen, explain why your Seattle property requires different protection than properties elsewhere, and help you avoid the costly mistakes that come from underinsurance or mismatched coverage. The next step involves evaluating which specific policy features and limits actually fit your property and your financial situation.

Selecting Coverage That Actually Protects Your Seattle Rental

Calculate Your True Replacement Cost

Your dwelling coverage must match what it actually costs to rebuild your property, not what you paid for it years ago. Seattle reconstruction costs can range from $100 to $500 per square foot, with the average around $150 per square foot, which means a 2,000 square foot property needs significant dwelling coverage to rebuild after total loss. Many Seattle landlords set limits based on purchase price from a decade ago, then face six-figure shortfalls when construction costs have climbed substantially since then. Contact local contractors for current rebuild estimates specific to your property’s age and condition. This single step prevents the costly mistake of underinsurance that leaves you paying tens of thousands out-of-pocket after a major loss.

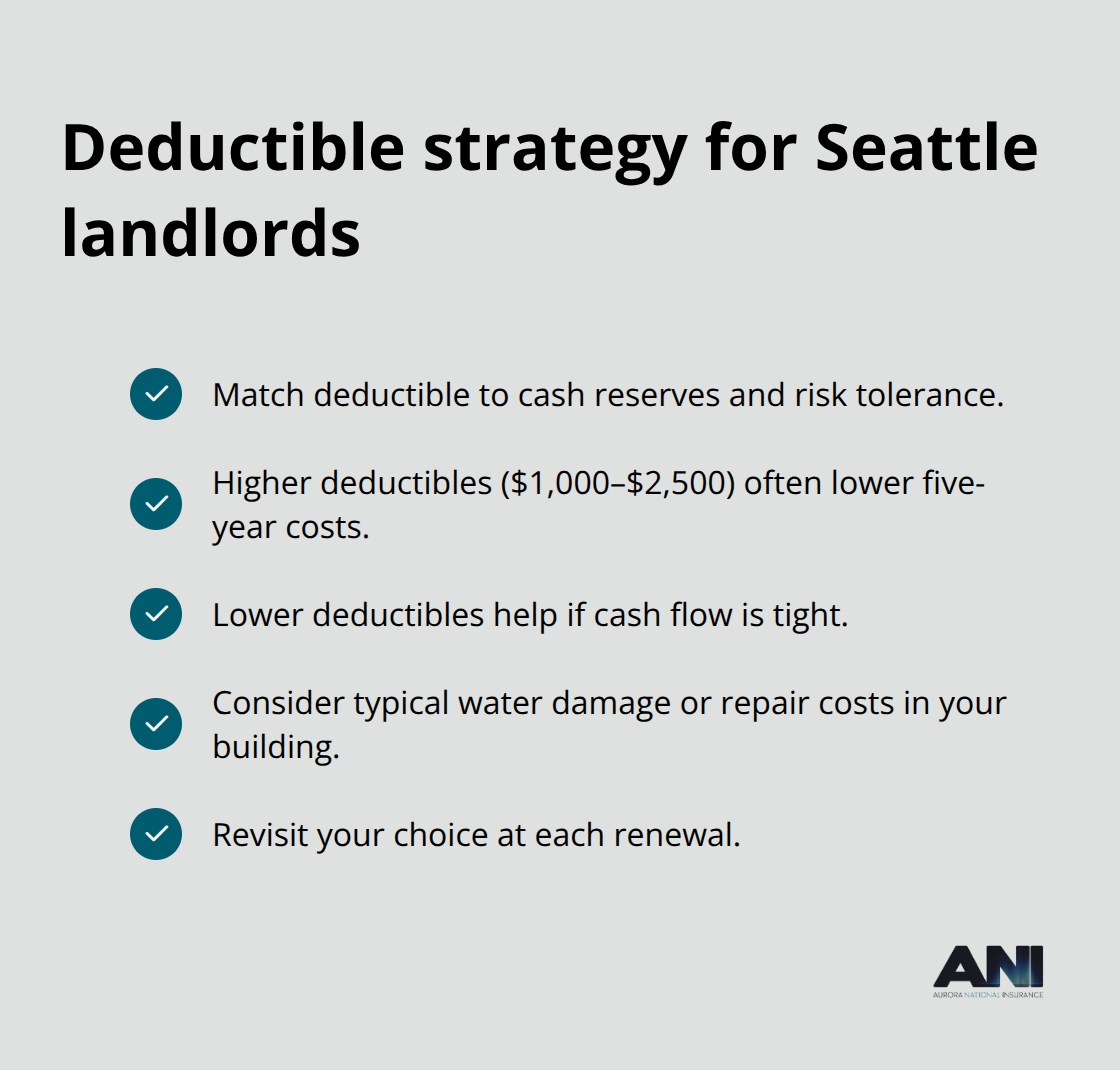

Choose Your Deductible Based on Cash Flow

Your deductible choice trades premium savings against out-of-pocket risk. A $500 deductible costs roughly 15 to 20 percent more annually than a $2,500 deductible, but after a water damage claim costing $8,000 in repairs, that premium difference vanishes in a single incident. For most Seattle landlords with adequate cash reserves, a $1,000 or $2,500 deductible makes financial sense because you save more in premiums over five years than you pay out-of-pocket in a typical claim.

Higher deductibles work well if you have emergency reserves to cover unexpected costs. Lower deductibles protect landlords with tight cash flow who cannot absorb sudden repair expenses.

Set Liability Limits That Match Seattle’s High-Cost Environment

Standard $300,000 to $500,000 per occurrence limits leave dangerous exposure when a tenant or guest injury claim runs $100,000 in medical costs alone plus legal defense fees. Move to $1,000,000 per occurrence, which adds roughly 10 to 15 percent to your annual premium-a modest cost for the protection gap it closes. An umbrella policy extending another $1,000,000 costs roughly $200 to $400 yearly and covers claims that exceed your underlying liability limits. This combination proves essential for landlords with multiple properties or aging buildings where injury risk runs higher.

Compare Quotes Using Identical Specifications

Comparing quotes from multiple carriers reveals dramatic price differences for identical Seattle properties. One carrier might quote $1,200 annually while another quotes $1,800 for the same building because carriers price Washington risk differently based on their claims experience and market appetite. Request quotes using identical specifications: same dwelling limit, same deductible, same liability limit, same property details. This forces apples-to-apples comparison rather than letting carriers hide premium differences in different coverage assumptions. Ask each carrier whether they offer discounts for recent roof replacement, electrical updates, or plumbing work, since these improvements can reduce premiums by 5 to 10 percent but only if the carrier applies the discount. Compare DP-2 versus DP-3 policy forms specifically because the 15 to 25 percent premium difference between them reflects real coverage gaps. DP-3 policies cover additional perils and typically offer broader protection worth the extra cost for most Seattle landlords, while DP-2 policies exclude certain water damage and weather events that regularly occur in Washington.

Work With a Local Agent to Access Better Options

A local agent who understands Seattle’s rental market can access carriers and policy forms that online quote engines never show, expanding your options beyond whatever three national carriers a website compares. They know which carriers actively compete for Seattle multifamily business versus those charging premium rates to discourage applications. They can explain why your specific property qualifies for certain discounts with one carrier but not another-information that determines whether you save $300 or $800 annually. The agent’s carrier relationships allow them to negotiate terms and sometimes secure better rates than you would receive calling the carrier directly, making their consultation financially valuable rather than merely informational.

Final Thoughts

Seattle landlord insurance protects your rental investment from the specific risks that plague this market. Rising premiums, earthquake exposure, flood risk, and Washington’s strict tenant laws create a complex insurance landscape that demands more than a generic online quote. The coverage limits you select today determine whether a major loss becomes a manageable claim or a financial catastrophe that wipes out years of rental income.

Your Seattle rental property requires dwelling limits that reflect current reconstruction costs, liability protection scaled to the high-cost environment, and specialized endorsements for earthquake and flood exposure. A $1,000,000 umbrella policy costs roughly $200 to $400 annually and fills critical gaps that standard policies leave exposed. Comparing quotes from multiple carriers using identical specifications reveals dramatic price differences-sometimes $600 or more annually for the same building.

A local insurance agent who understands Seattle’s neighborhoods, building stock, and tenant demographics identifies coverage gaps that national carriers miss. They know which improvements reduce premiums by 5 to 10 percent with specific carriers and which ones insurance companies ignore. Contact a local agent to review your current coverage and identify whether you pay for protection you don’t need or leave dangerous gaps in coverage you do need, or reach out to Aurora National Insurance to connect with licensed agents who help Seattle landlords find the right protection at competitive prices.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.