Washington Homeowners Insurance Costs: How to Save on Premiums

Washington homeowners insurance costs have climbed steadily over the past few years, leaving many property owners searching for relief on their premiums.

At Aurora National Insurance, we’ve helped thousands of Washington homeowners find real savings by understanding what drives their rates and where to look for discounts. This guide walks you through the specific factors affecting your costs and the practical steps you can take to lower them.

Factors That Drive Up Washington Homeowners Insurance Premiums

Location and Weather Risk Create the Biggest Price Differences

Location matters far more than most homeowners realize. Washington sits on the Cascadia Subduction Zone, creating significant earthquake risk that standard policies exclude entirely. Western Washington faces heavy Pacific storms with wind and rainfall that damage roofs and foundations, while eastern Washington battles wildfire exposure that has driven some of the state’s billion-dollar weather disasters since 1980.

Your ZIP code alone shifts your premium by hundreds of dollars because insurers price based on local fire department proximity, wildfire risk zones, and historical claim patterns in your specific area. Within Washington, costs vary dramatically by city: Tacoma averages around $1,658 annually, Seattle around $1,505, and Spokane around $1,458 for similar coverage.

Home Age and Construction Type Affect Your Rate

Home age and construction type directly influence what insurers charge. Older homes with original electrical wiring, plumbing, and roofing systems cost more to insure because they fail more often and create fire hazards. Wood-frame homes typically cost more than brick or stone construction due to fire risk.

Claims History and Credit Score Impact Your Premium

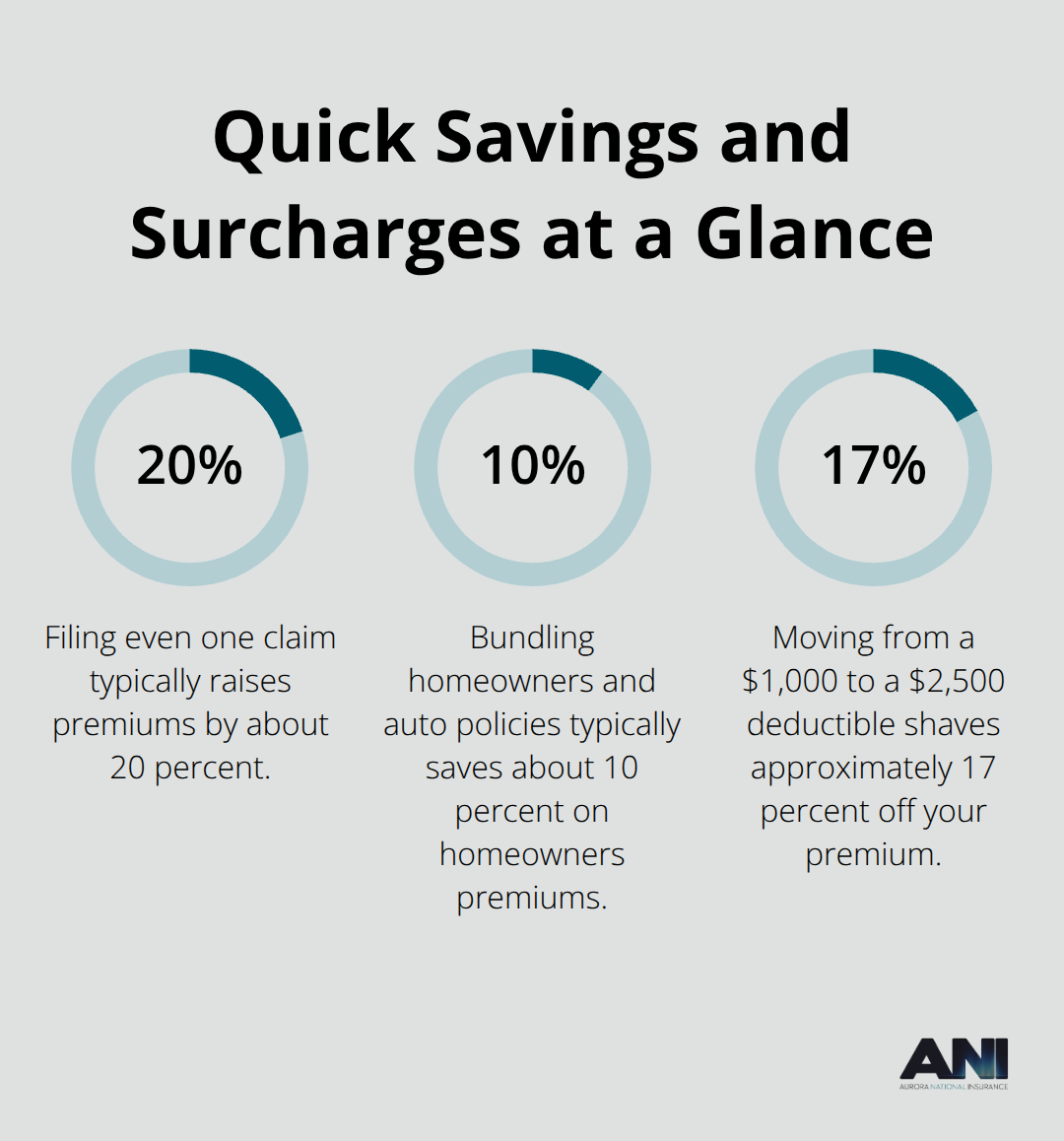

Your claims history works against you immediately: filing even one claim typically raises premiums by about 20 percent and can affect rates for years. If you’ve lived in your home for three to five years without filing claims, you qualify for loyalty discounts around 5 percent, which climb to roughly 10 percent after six years.

Your credit score influences rates as well, with better scores yielding lower premiums. Try for a FICO score above 670 and fix any errors on your credit report through Experian before shopping for quotes. Paying bills on time and keeping credit card balances below 30 percent of your limit can improve your score within three to six months, directly lowering the rates you receive from insurers.

Understanding these three factors positions you to take action-and that’s where practical strategies come into play.

How to Cut Your Washington Homeowners Insurance Costs Right Now

Compare Quotes Across Multiple Insurers

Comparing quotes across multiple insurers reveals the true scope of savings available to Washington homeowners. Rates for identical coverage vary dramatically between carriers-sometimes by hundreds of dollars annually-because each insurer weighs risk factors differently. Get quotes from at least three insurers before committing to a policy; the Insurance Information Institute reports that shopping around consistently delivers the best overall value. Most homeowners complete this process in about five minutes using online quote tools, making it one of the fastest ways to identify savings.

Bundle Strategically, But Verify the Math

Bundling your homeowners and auto policies with the same carrier typically saves about 10 percent on homeowners premiums, though bundling does not always produce the lowest total price when you factor in auto costs. Verify exactly how the bundling discount applies in your policy documents and confirm the savings actually appear on your bill before signing. If one insurer offers the best homeowners rate and another offers better auto pricing, calculate your total cost for both scenarios rather than assuming bundling wins automatically.

Raise Your Deductible to Lower Monthly Costs

Raising your deductible from $500 to $1,000 reduces annual premiums by roughly 10 to 25 percent depending on your location and rebuild cost, according to the Insurance Information Institute. Moving from $1,000 to $2,500 shaves approximately 17 percent off your premium. The key is choosing a deductible you can actually afford to pay out of pocket if you file a claim; a lower premium means nothing if you cannot cover the deductible when disaster strikes.

Install Security Systems and Storm Hardening

Home safety improvements deliver measurable premium reductions that compound over time. Installing a monitored security system with burglar alarms, smoke detectors, and deadbolts typically saves at least 5 percent and potentially 15 to 20 percent with advanced systems like monitored fire sprinklers. Storm hardening measures such as impact-resistant roofing, shatterproof glass, and storm shutters qualify for discounts in Washington, though verification requirements vary by insurer. Ask your carrier which specific mitigation upgrades qualify for credits and what proof or inspections they require before investing in improvements.

Modernize Your Home’s Systems and Request Renovation Discounts

Modernizing your home’s electrical wiring, plumbing, and HVAC systems also reduces premiums because newer infrastructure poses lower fire and failure risks. Home renovations completed within the past five years often qualify for dedicated discounts that you must explicitly request-insurers rarely volunteer these credits. Contact your agent to confirm which upgrades qualify and ensure the discounts appear in your policy documents before your renewal date. Once you’ve locked in these savings, the next step involves identifying and avoiding the costly mistakes that undo your progress.

Mistakes That Waste Money on Washington Homeowners Insurance

Price Alone Masks Coverage Gaps

The biggest mistake Washington homeowners make is selecting a policy based purely on the lowest price without verifying what coverage actually comes with that quote. A $1,200 annual premium means nothing if your dwelling coverage falls $150,000 short of your home’s rebuild cost or if critical perils like wind or hail carry separate deductibles you never anticipated. Homeowners discover coverage gaps only after filing a claim, when it’s far too late to adjust.

Price comparison tools make it easy to spot the cheapest option, but they obscure critical details. Your rebuild cost estimate may not match current construction expenses in your ZIP code. Your deductible may not apply uniformly across all perils. Your policy may include replacement cost coverage or actual cash value-two very different protections. The Washington Department of Insurance emphasizes that dwelling coverage must reflect the actual cost to rebuild your home, not its market value including land, because rebuild costs have climbed significantly in recent years.

Request a detailed coverage summary from each insurer showing dwelling limit, deductible structure, and whether specific perils carry separate deductibles before comparing premiums.

Annual Reviews Prevent Underinsurance and Waste

Most homeowners fail to review their coverage annually, allowing their policies to drift out of alignment with their actual possessions and home improvements. When you install a new roof, upgrade electrical systems, or add a finished basement, your rebuild cost rises but your policy limit often stays frozen at its original amount, leaving you underinsured. Conversely, if you’ve paid down your mortgage or your home’s market value has declined relative to rebuild costs, you may be overinsuring and throwing money away on excess coverage.

The Insurance Information Institute reports that reviewing your policy annually takes roughly 30 minutes and frequently uncovers opportunities to adjust coverage downward or unlock discounts you qualify for but never claimed. This simple step prevents costly surprises and identifies savings you’ve already earned.

Unclaimed Discounts Cost Thousands Over Time

Washington homeowners systematically leave money on the table by never asking about available discounts. Many insurers offer credits for home renovations completed within the past five years, loyalty discounts that climb from 5 percent after three to five years to 10 percent after six years, new-home discounts, non-smoker status, and bundling savings.

Homeowners never request these credits because they assume the quote already reflects their lowest possible rate.

Contact your agent or insurer directly and ask specifically which discounts apply to your profile, then verify each one appears in your policy documents before renewal takes effect. This conversation takes minutes but can reduce your annual premium by hundreds of dollars.

Final Thoughts

Reducing Washington homeowners insurance costs requires three concrete actions: understanding what drives your rates, comparing quotes across multiple carriers, and claiming every discount you qualify for. Location, home age, claims history, and credit score create the foundation of your premium, but they don’t determine your final bill. The gap between the highest and lowest quotes for identical coverage often exceeds several hundred dollars annually, which means shopping around delivers immediate savings without sacrificing protection.

Bundling policies, raising your deductible to $1,000, and installing a monitored security system each lower your premium by measurable amounts. These steps compound when combined-a homeowner who bundles policies, increases their deductible, installs a monitored security system, and claims loyalty discounts can reduce their annual premium by 30 to 40 percent compared to their initial quote. Annual policy reviews prevent you from overpaying for coverage you no longer need or remaining underinsured after home improvements.

Get quotes from at least three insurers, verify the coverage details match your rebuild cost and risk profile, and ask about every discount your profile qualifies for. Aurora National Insurance represents multiple top-rated carriers and can deliver tailored comparisons to help you find the right protection at competitive prices for Washington homeowners insurance costs.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.