Alaska Rental Property Insurance: Protect Your Investment Locally

Alaska’s rental market demands insurance built for extreme conditions. Harsh winters, remote locations, and seasonal vacancy patterns create risks that standard policies simply don’t address.

At Aurora National Insurance, we’ve seen firsthand how Alaska rental property insurance needs differ from the lower 48. This guide walks you through the coverage types that actually protect your investment in Alaska’s unique environment.

Why Alaska Rental Properties Cost More to Insure and Protect

Alaska’s rental market sits in a fundamentally different risk category than properties in the lower 48, and your insurance costs reflect that reality. The state’s extreme weather patterns, geographic isolation, and seasonal occupancy swings create genuine expenses that drive premiums up. This isn’t market fluctuation or insurance company overreach-it’s the actual cost of labor, materials, and severe weather exposure in Alaska. A property in Anchorage or Fairbanks faces replacement costs that dwarf national averages because shipping materials into remote areas costs significantly more, and skilled contractors charge premium rates for work during brutal winters. You’ll pay more because repairs take longer when temperatures drop to minus 30 degrees and roads become impassable. Standard policies designed for southern climates simply don’t account for ice jams that flood properties during spring breakups, foundation damage from permafrost shifts, or the months-long repair timelines that result from Alaska’s geography.

Earthquake and Flood Risks Demand Active Coverage Decisions

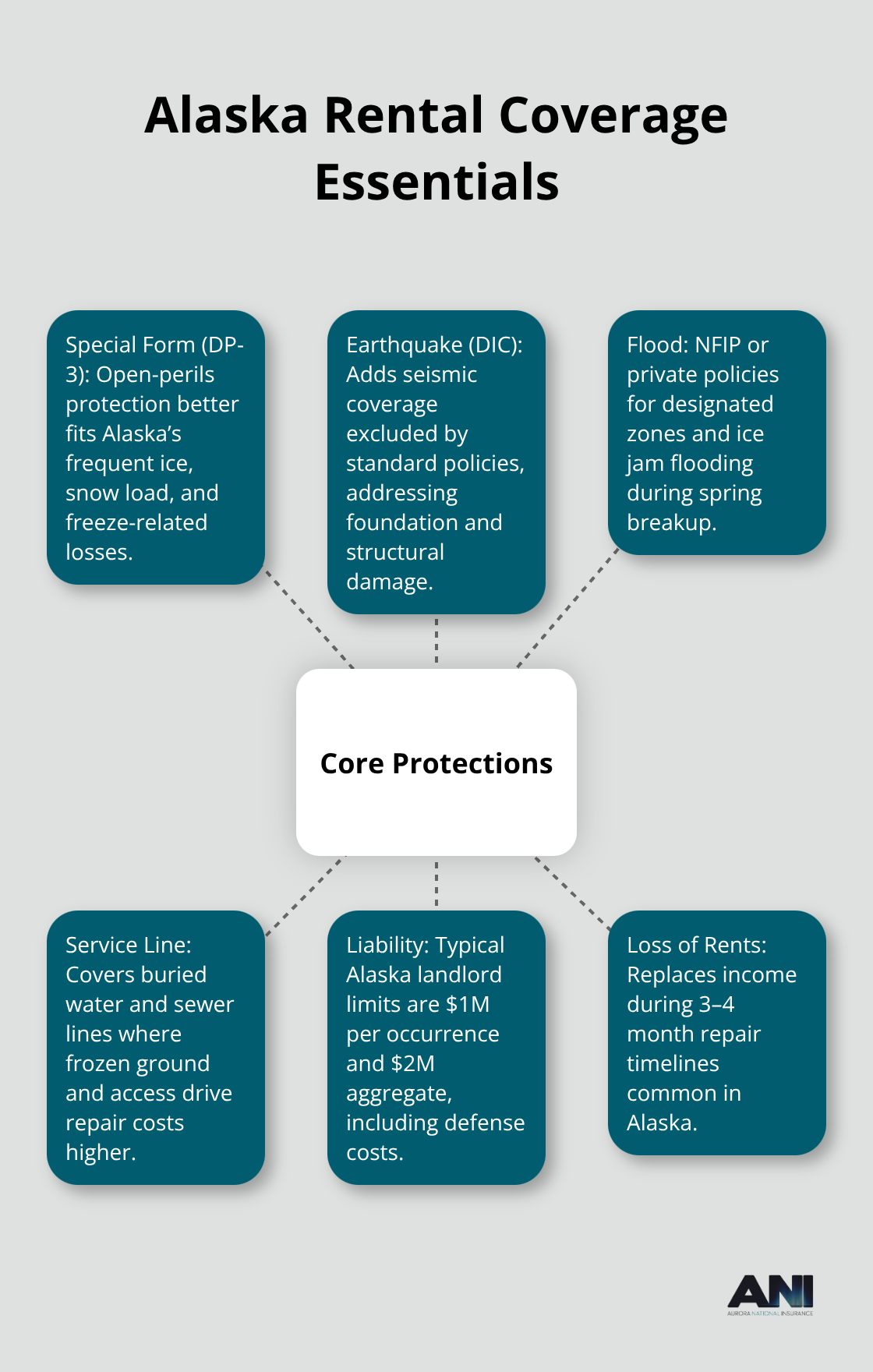

Alaska sits on active seismic zones, yet earthquake damage is automatically excluded from standard landlord policies. You must specifically add a Difference in Conditions endorsement to cover seismic foundation damage-a step many landlords skip only to face devastating losses after a claim. Flood risk amplifies through ice jams and spring breakups, so properties in designated flood zones typically require National Flood Insurance Program coverage or a private flood policy rather than standard dwelling protection. The real cost trap emerges when landlords use generic insurance agencies unfamiliar with Alaska risks and overpay while simultaneously underbuying critical endorsements.

Replacement Cost Estimates Prevent Coinsurance Penalties

A professional rebuild estimate every 2–3 years protects you from coinsurance penalties that can cost thousands out of pocket after a major loss. You must insure to actual replacement cost, not a percentage or national average, to avoid these penalties. Loss of rents coverage reimburses income if the property becomes uninhabitable during repairs and typically costs about $1 per $1,000 of annual rent-a modest expense that prevents cash flow collapse during Alaska’s extended repair seasons when contractors book out months in advance.

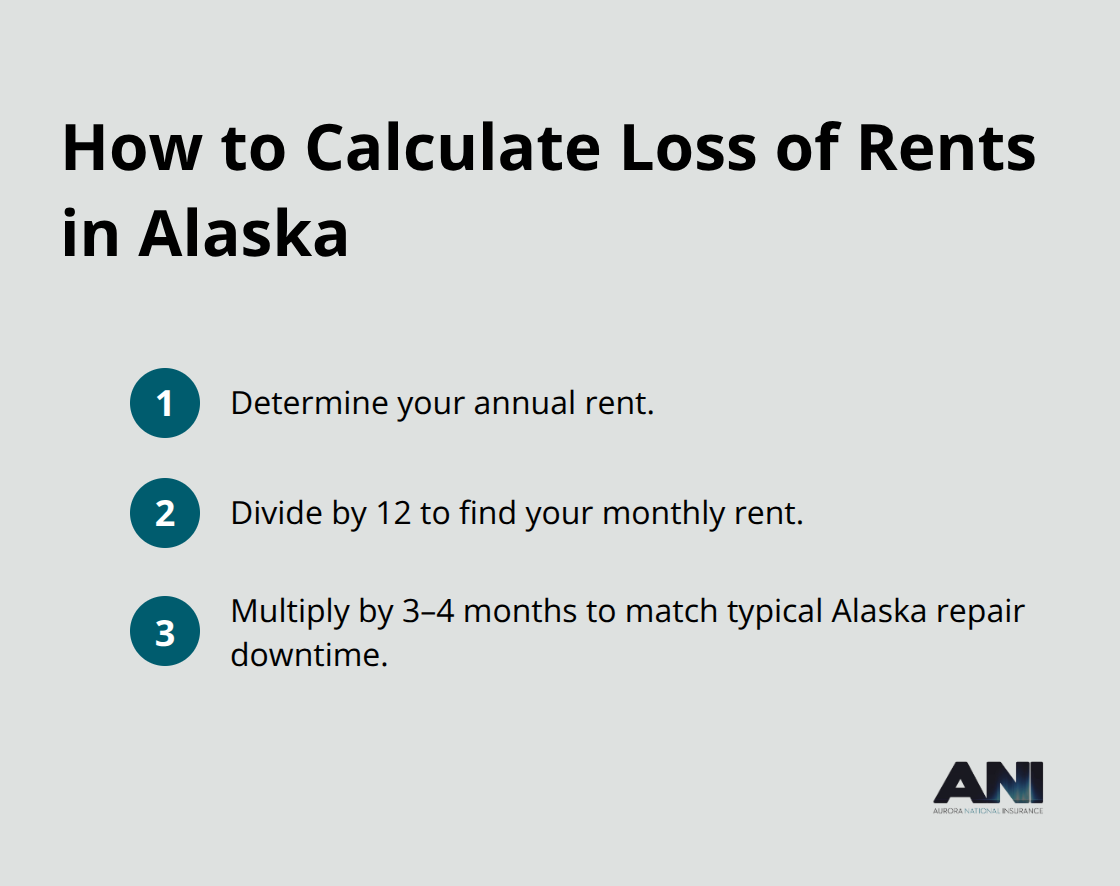

Calculate Loss of Rents Coverage for Alaska’s Repair Timeline

Seasonal vacancy patterns require you to calculate loss of rents needs accurately. Determine your annual rent, divide by 12, and multiply by the realistic number of vacant months (typically 3–4 months in Alaska during major repairs). This approach ensures you protect yourself for actual downtime rather than guessing at coverage limits. The next section walks you through assessing your specific property’s risk factors and comparing coverage options across carriers to find the right protection for your Alaska investment.

What Coverage Actually Protects Your Alaska Rental

Dwelling Fire Insurance and Special Form Protection

Dwelling fire insurance forms the foundation of Alaska rental protection, but standard coverage falls short in this market. You need Special Form coverage, often called DP-3, because it protects against open perils rather than named perils only. This distinction matters enormously in Alaska, where ice dam damage, weight of snow collapse, and frozen pipe bursts happen regularly. The dwelling limit must reflect actual replacement cost in your specific location, not a national average or percentage-based estimate. Properties in Anchorage or Fairbanks typically require $75 to $150 per square foot in replacement cost coverage depending on construction quality and age. A professional rebuild estimate every 2–3 years allows you to adjust your dwelling limit accordingly. Underinsurance triggers coinsurance penalties that reduce your payout dollar-for-dollar, meaning a $500,000 dwelling insured at only $400,000 will pay out proportionally less on any claim.

Alaska-Specific Endorsements Close Critical Coverage Gaps

Extended protection through endorsements addresses Alaska-specific gaps that standard policies exclude. You absolutely must add Difference in Conditions coverage for earthquake damage since seismic activity regularly affects Alaska properties and standard policies automatically exclude it. Earthquake insurance covers the cost to remove debris and pays for additional living expenses you may have while your home is being rebuilt or repaired. Flood coverage through the National Flood Insurance Program or private carriers becomes mandatory if your property sits in a designated flood zone, which includes areas vulnerable to ice jam flooding during spring breakups. Service line coverage protects buried water and sewer lines from damage, a critical addition in Alaska where repair costs run $5,000 to $15,000 per line due to frozen ground and remote access challenges.

Liability and Medical Payments Protection

Liability coverage protects you when tenants or guests suffer injuries on your property and decide to sue. Standard Alaska landlord policies typically include $1 million per occurrence and $2 million aggregate liability, which covers legal defense costs and judgments. Premises medical payments coverage, usually around $5,000 per occurrence, pays medical expenses immediately after minor injuries without requiring a lawsuit, which often prevents claims from escalating.

Loss of Rents Coverage Prevents Cash Flow Collapse

Loss of rents coverage directly replaces income when a covered peril makes the property uninhabitable during repairs. In Alaska, where repair timelines stretch to 3–4 months due to contractor availability and weather delays, this coverage prevents financial collapse during extended downtime. Calculate your need by taking annual rent, dividing by 12, multiplying by realistic vacant months, then purchasing coverage to match that figure. If you collect $12,000 annually and expect 4 months of repairs, purchase $4,000 in loss of rents coverage. This coverage typically costs about $1 per $1,000 of annual rent, making it an inexpensive way to protect cash flow.

Comparing Quotes Across Carriers Reveals True Price Differences

When shopping for quotes, request identical specifications from at least three carriers, specifying the same dwelling limit, deductible, liability limit, and loss of rents amount. This prevents carriers from comparing apples to oranges and shows you true price differences. Verify each quote reflects your property’s actual replacement cost by checking the dwelling limit against a recent rebuild estimate, since underinsurance creates penalties that no coverage can fix. The next section walks you through assessing your specific property’s risk factors and selecting the right carrier for your Alaska investment.

Choosing the Right Coverage for Your Alaska Property

Assess Your Property’s Actual Risk Profile

Assessing your property’s actual risk requires moving past generic checklists and confronting the specific vulnerabilities of your rental. Start by documenting your property’s construction type, age, and square footage, then obtain a professional rebuild estimate from a local Alaska contractor who understands replacement costs in your area. This estimate becomes your baseline for dwelling coverage and prevents the coinsurance penalties that plague underinsured landlords. Next, map your property against Alaska’s specific hazards: Is it in a designated flood zone vulnerable to ice jam flooding during spring breakups? Does it sit in an earthquake zone requiring a Difference in Conditions endorsement? Are heating systems, plumbing, and weatherproofing recent upgrades that qualify for rate credits, or are they original 1970s installations that raise claim frequency?

Document any security features like alarms or cameras since these lower premiums measurably. Calculate your realistic loss of rents need by multiplying your monthly rent by 3 to 4 months, the typical repair window in Alaska when contractor schedules back up. Your property’s location matters enormously: properties in higher-crime Anchorage neighborhoods cost more to insure than rural Fairbanks rentals, while older buildings with documented upgrades often insure cheaper than newer properties without maintenance records. Gather receipts for any roof replacements, heating upgrades, or weatherproofing improvements and share these at renewal, as documented upgrades yield meaningful rate credits.

Request Identical Quotes From Multiple Carriers

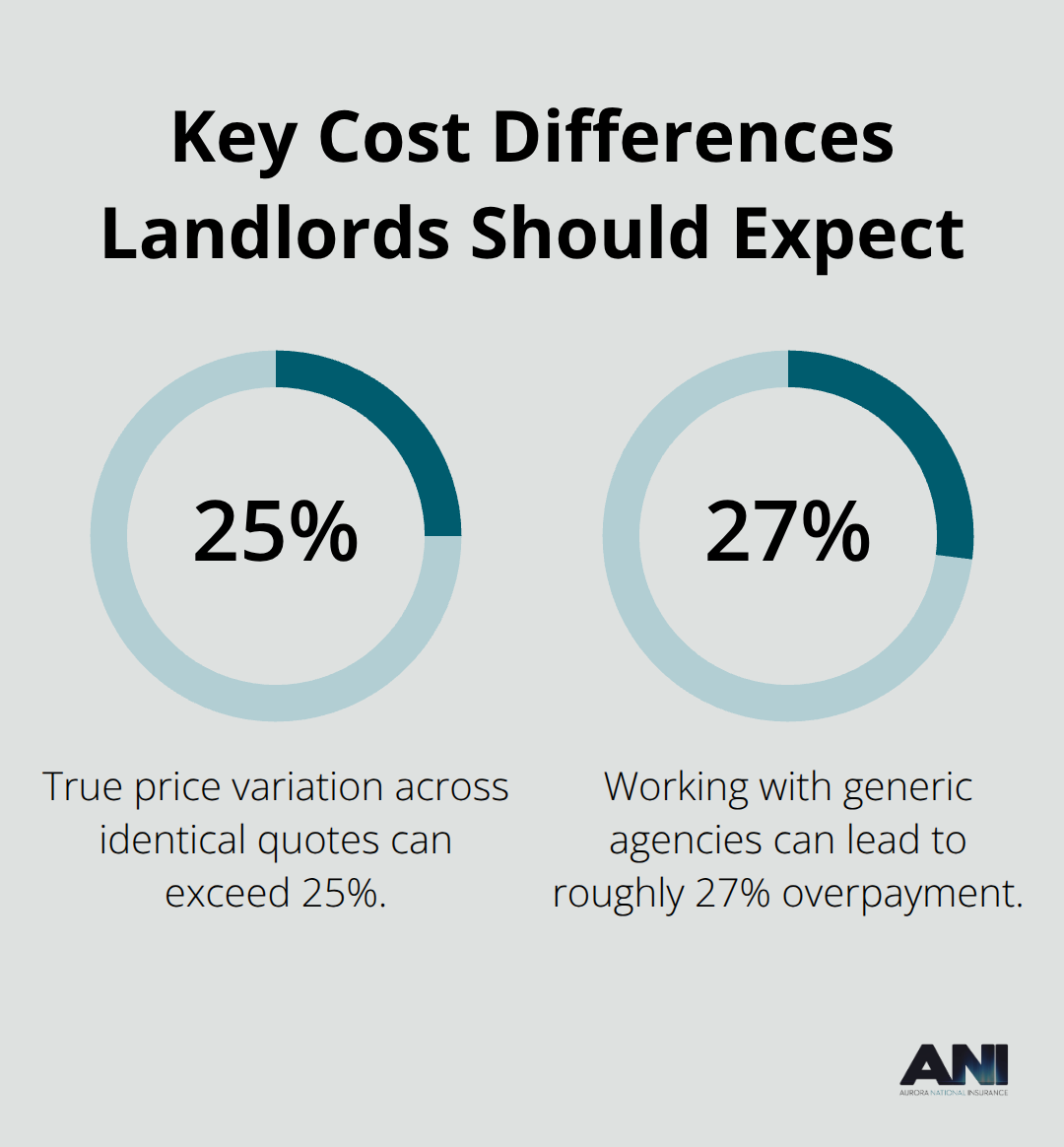

Requesting identical quotes from at least three carriers exposes the true price variation across the market, which often exceeds 25 percent for identical coverage. Contact carriers with the same specifications: your property’s actual replacement cost dwelling limit, $1 million liability, $500 deductible, and your calculated loss of rents amount.

Verify each quote reflects your specific rebuild estimate, not a national average or square footage assumption. Strong carriers maintain substantial Alaska presence and earn recognition for fast claim response.

Verify Financial Strength and Coverage Details

Request AM Best ratings of A- VIII or better, the financial strength measure that lenders require and that guarantees claims payment reliability. Ask each carrier about earthquake and flood endorsements before comparing final quotes, since these add-ons aren’t always included and their absence creates dangerous coverage gaps. Avoid month-to-month policies initially, as annual policies lock in rates and allow you to budget with certainty, though some carriers do offer flexibility for portfolio transitions. An independent agent representing multiple top-rated carriers can compare options efficiently and deliver the local expertise that prevents the roughly 27 percent overpayment that landlords often face when working with generic agencies unfamiliar with Alaska risk factors.

Final Thoughts

Alaska rental property insurance protects your investment by addressing risks that standard policies ignore. Dwelling fire insurance with Special Form protection, liability coverage, loss of rents, and Alaska-specific endorsements for earthquake and flood form the foundation of genuine protection in this market. Skipping any of these components leaves you exposed to losses that can exceed your entire annual rental income.

Local expertise prevents the roughly 27 percent overpayment that landlords face when working with generic agencies unfamiliar with Alaska’s climate and contractor availability. An independent agent representing multiple top-rated carriers compares quotes efficiently, identifies coverage gaps, and explains why your replacement cost estimate drives your dwelling limit rather than a percentage or national average. They understand that ice jam flooding requires specific flood coverage, that earthquake damage demands a Difference in Conditions endorsement, and that loss of rents calculations must account for Alaska’s extended repair timelines.

Request identical specifications from at least three carriers, specifying your property’s actual replacement cost dwelling limit, $1 million liability, your calculated loss of rents amount, and a $500 deductible. Verify each quote reflects your specific rebuild estimate and ask about AM Best ratings to confirm financial strength. Contact us today to request quotes-the difference between adequate coverage and underinsurance often exceeds thousands of dollars when a major loss occurs.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.