Freight Carrier Auto Insurance: Protecting Your Fleet on the Road

Running a freight operation means managing real risks on every route. Vehicle breakdowns, accidents, and cargo damage can quickly drain your budget and damage your reputation.

At Aurora National Insurance, we know that freight carrier auto insurance isn’t optional-it’s the foundation of a sustainable business. This guide walks you through the coverage types that matter, the factors that shape your rates, and how to find the right protection for your fleet.

What Your Freight Insurance Actually Covers

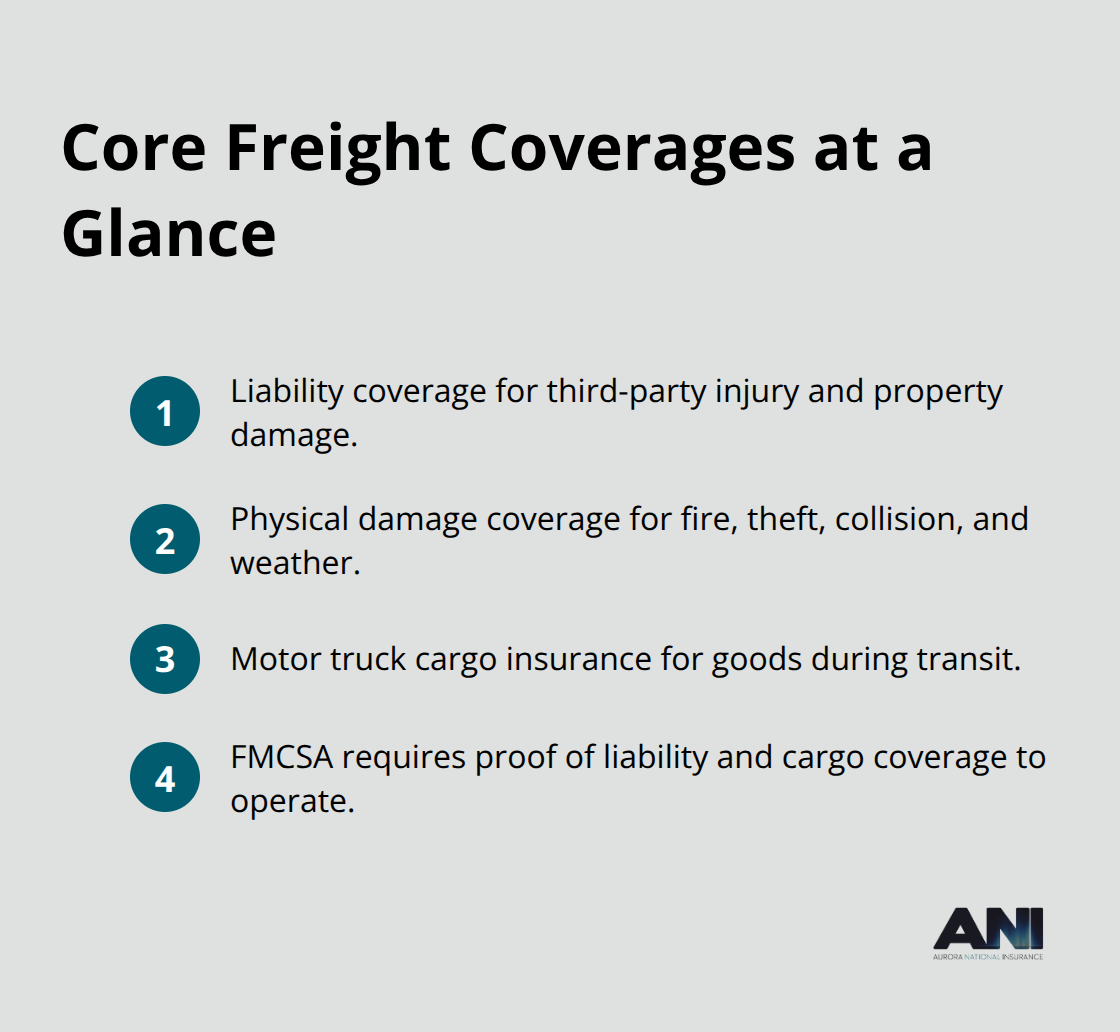

Freight carrier auto insurance isn’t one-size-fits-all. Federal law requires you to carry liability coverage with a minimum limit of $750,000 for non-hazardous freight trucks weighing over 10,001 pounds, but that’s just the baseline. Hazardous materials carriers face much steeper requirements-a $5 million policy is mandatory for trucks transporting radioactive materials, explosives, gases, or inhalation hazards. Liability coverage protects you when your truck causes injury or property damage to someone else, and it’s the first line of defense against lawsuits that can bankrupt an operation. Beyond liability, physical damage coverage protects your vehicles against fire, theft, collision, and weather events. This is voluntary coverage, but skipping it leaves your equipment vulnerable to losses that insurance could absorb. Cargo insurance is equally important and federally required when you transport household goods across state lines.

Motor truck cargo insurance covers goods during transit from damage, loss, or theft due to collision, fire, or other covered events. The FMCSA requires proof of both liability and cargo insurance to issue operating authority-no insurance means no authorization to operate.

Standard Cargo Coverage and Its Limits

Standard cargo insurance covers lost or damaged freight, removal expenses for cleanup, and earned freight to protect you from customer charges for undelivered loads. However, this baseline protection leaves gaps that can cost you money. Common exclusions apply: art, jewelry, contraband, and items left in your truck for more than 72 hours typically aren’t covered. Live animals are generally excluded unless death occurs within 24 hours. Pharmaceuticals, tobacco, and alcohol face restrictions depending on your state and carrier. Set your coverage limit based on the sender or receiver’s requirements and choose a deductible per claim that balances cost against risk.

Expanding Protection with Cargo Plus Endorsements

Cargo Plus endorsements broaden protection to include wetness, rust, corrosion, and driver error-gaps that standard policies leave exposed. Paired with refrigeration breakdown coverage, Cargo Plus also protects temperature-related losses in reefer trucks, which matters if your operation handles perishables. For high-value shipments, higher limits are non-negotiable; underinsuring cargo exposes you to catastrophic financial loss when accidents happen. These enhanced endorsements cost more upfront but protect your revenue and customer relationships when damage occurs.

Matching Coverage to Your Cargo and Routes

The type of freight you haul directly shapes your insurance needs. Temperature-sensitive cargo requires different protection than standard dry goods, and hazardous materials demand compliance with federal regulations that go far beyond standard policies. Your routes also matter-long-haul operations across multiple states face different risks than regional deliveries. Work with your insurance provider to evaluate the specific value and nature of your goods, analyze the likelihood and impact of delays or damage, and review policy limits and exclusions. This assessment helps you tailor coverage that actually protects your operation instead of leaving you exposed when claims arise.

What Drives Your Freight Insurance Costs

Insurance premiums for freight carriers have climbed dramatically over the past decade. Car insurance rates are increasing by an average of 4.9 percent nationally, even as trucking crash numbers declined in the last four years. This disconnect reveals a hard truth: insurers price for litigation risk, not just accident frequency.

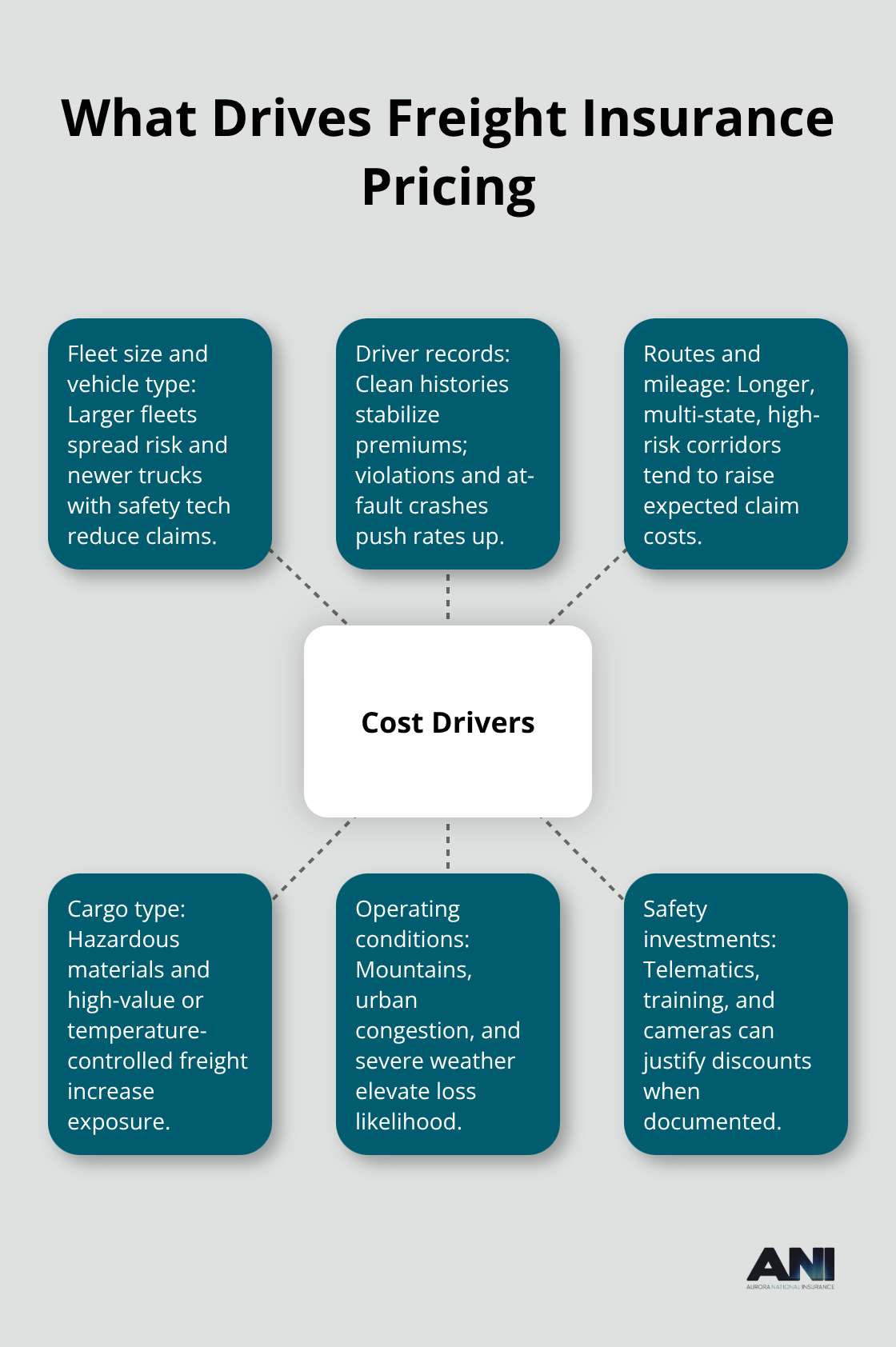

Fleet Size and Vehicle Type Shape Your Rates

Your fleet size directly influences premium calculations. A five-truck operation pays per-vehicle rates that differ substantially from a fifty-truck fleet because larger operations spread risk across more units and typically maintain more sophisticated safety programs. Vehicle type matters equally. Newer trucks with advanced safety technology command lower premiums than aging equipment because collision avoidance systems and telematics demonstrably reduce claim frequency. A tractor-trailer hauling hazardous materials costs far more to insure than a box truck moving general freight because regulatory requirements and potential liability exposure are exponentially higher.

Driver Records Determine Premium Stability

Your driver roster is where premiums either stabilize or spiral upward. Drivers with clean records and multiple years of experience receive better rates than operators with recent violations or accidents. One serious at-fault collision can increase your fleet’s premiums by thousands of dollars annually for years afterward. Insurance carriers scrutinize your hiring practices and whether you conduct regular driving license checks and monitor high-risk driver groups. Drivers who exceed average speed by 10 to 15 percent are significantly more likely to crash according to road safety research, and insurers factor this risk into their quotes.

Routes, Cargo Type, and Operating Conditions

Annual mileage and route selection directly correlate with claim costs. A regional carrier operating 50,000 miles annually across established routes in low-accident corridors pays substantially less than a long-haul operation crossing multiple states on high-risk highways. Mountainous terrain, urban congestion, and weather patterns all affect underwriting decisions.

Winter operations in northern climates increase premiums because accident rates spike during snow and ice conditions. Your cargo type influences pricing as well. Expedited freight operations with tight delivery windows face higher accident likelihood because speed pressures override safe driving practices, so liability coverage reflects this elevated risk. Temperature-controlled reefer operations command premium adjustments because mechanical failures and spoilage claims add complexity. Hazardous materials routes require compliance with federal regulations and specialized training documentation that insurers verify before quoting.

Document Your Safety Investments Before Renewal

The most actionable step you can take is consolidating your safety data into one source of truth before renewal conversations. Track your incident history, near-miss reports, driver training completion, and telematics data showing harsh braking or excessive speed. Present this evidence to your insurer to justify rate reductions based on demonstrated risk reduction rather than accepting across-the-board increases. Carriers increasingly recognize that fleets investing in safety technology and formal training programs deserve better pricing, but you must document and communicate those investments clearly. This documentation becomes your foundation for negotiating better rates and selecting an insurance partner who values your commitment to safer operations.

Selecting an Insurance Partner That Understands Freight Operations

Finding the right freight carrier insurance provider requires more than comparing premium quotes side by side. Freight operators need insurers who understand the specific pressures of tight delivery windows, multi-state compliance requirements, and the operational complexity of managing hazardous or temperature-sensitive cargo. The insurance market for trucking has tightened considerably. According to the American Transportation Research Institute, insurance cost and availability ranked as a leading issue facing fleets, signaling that not all carriers will write freight business at any price point. This means your selection process must prioritize insurers with genuine expertise in freight operations rather than generalist commercial carriers who treat trucking as a sideline.

Start with Specialized Freight Insurers

Request quotes from at least three carriers that specialize in freight rather than those offering generic commercial auto policies. Specialized freight insurers offer dedicated risk management consultations, flexible policy options, and priority claims processing to reduce downtime when incidents occur. When comparing coverage options, don’t assume that higher limits automatically mean better protection. Instead, verify that each quote includes the specific endorsements your operation requires. If you run reefer trucks, confirm that refrigeration breakdown coverage is included or available. If you haul high-value goods, ask whether the cargo limits match your actual shipment values or whether you’ll face underinsurance penalties.

Request written explanations of what each policy excludes because gaps in coverage often reveal themselves only after a claim arises. Ask each carrier directly about their claims process timeline. How long does it take to file a claim after an incident? Do they offer 24/7 claims reporting? Will they assign a dedicated claims adjuster to your account, or will you navigate an automated phone system?

For freight operations where downtime translates directly to lost revenue, a carrier with expedited claims handling can save you thousands of dollars per incident.

Pricing That Reflects Your Safety Investments

Don’t accept a renewal quote that simply adds a percentage increase to your prior year’s premium without explanation. Request a detailed breakdown showing how your claims history, fleet composition, driver records, and safety programs influenced the calculation. Bring documentation of any safety investments you’ve made: telematics system adoption, driver training completion rates, dash cam installations, or route optimization changes. Carriers increasingly offer premium reductions for fleets that demonstrate measurable risk reduction, but you must present the evidence proactively.

Ask whether the carrier offers bundling discounts. Even if you carry property insurance elsewhere, switching to a single carrier often yields meaningful discounts. Inquire about safety technology discounts specifically. If your fleet has adopted collision avoidance systems or in-cab monitoring, some carriers will reduce premiums based on demonstrated accident prevention.

Flexibility and Partnership Approach

Confirm whether the carrier will revisit your rates mid-term if you implement safety improvements rather than waiting until renewal. This flexibility separates carriers who genuinely partner with fleet operators from those simply collecting premiums. Ask about their approach to driver safety programs. Do they provide training resources or subsidies? Will they recognize drivers with clean records through preferred rates? Carriers that invest in your operational success beyond just underwriting claims tend to maintain more stable pricing and offer better service when problems arise.

Final Thoughts

Freight carrier auto insurance protects your operation’s ability to survive and grow beyond just vehicle protection. Calculate your actual cargo values, identify the routes and cargo types that define your operation, and match your coverage limits to those realities rather than accepting generic quotes. Document every safety investment your fleet makes-telematics adoption, driver training completion, collision avoidance systems, and incident reduction metrics-because this documentation becomes your negotiating foundation when renewal time arrives.

Specialized freight insurers understand the operational pressures you face daily: tight delivery windows, multi-state compliance requirements, and the financial impact of downtime. They offer dedicated risk management support, flexible policy options, and claims processes designed for speed rather than bureaucracy. When comparing carriers, ask about their approach to safety partnerships, mid-term rate adjustments for improvements, and bundling opportunities that reduce your total insurance spend.

We at Aurora National Insurance help you find freight carrier auto insurance that actually fits your operation through our network of top-rated carriers and local expertise. Our licensed agents deliver tailored comparisons and responsive service across Alaska, Washington, Oregon, and other key markets. Start with an instant online quote to see how your current coverage compares to what’s available in today’s market.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.