Seattle Commercial Vehicle Insurance: Protecting Your Fleet in the Pacific Northwest

Running a fleet in Seattle means navigating busy streets, strict regulations, and real financial risks. One accident or liability claim can cost thousands-or even shut down your business.

At Aurora National Insurance, we help fleet owners across the Pacific Northwest protect their operations with Seattle commercial vehicle insurance that actually covers what matters. The right policy isn’t just a legal requirement; it’s your safety net against the unexpected.

Why Seattle Fleets Face Real Insurance Risks

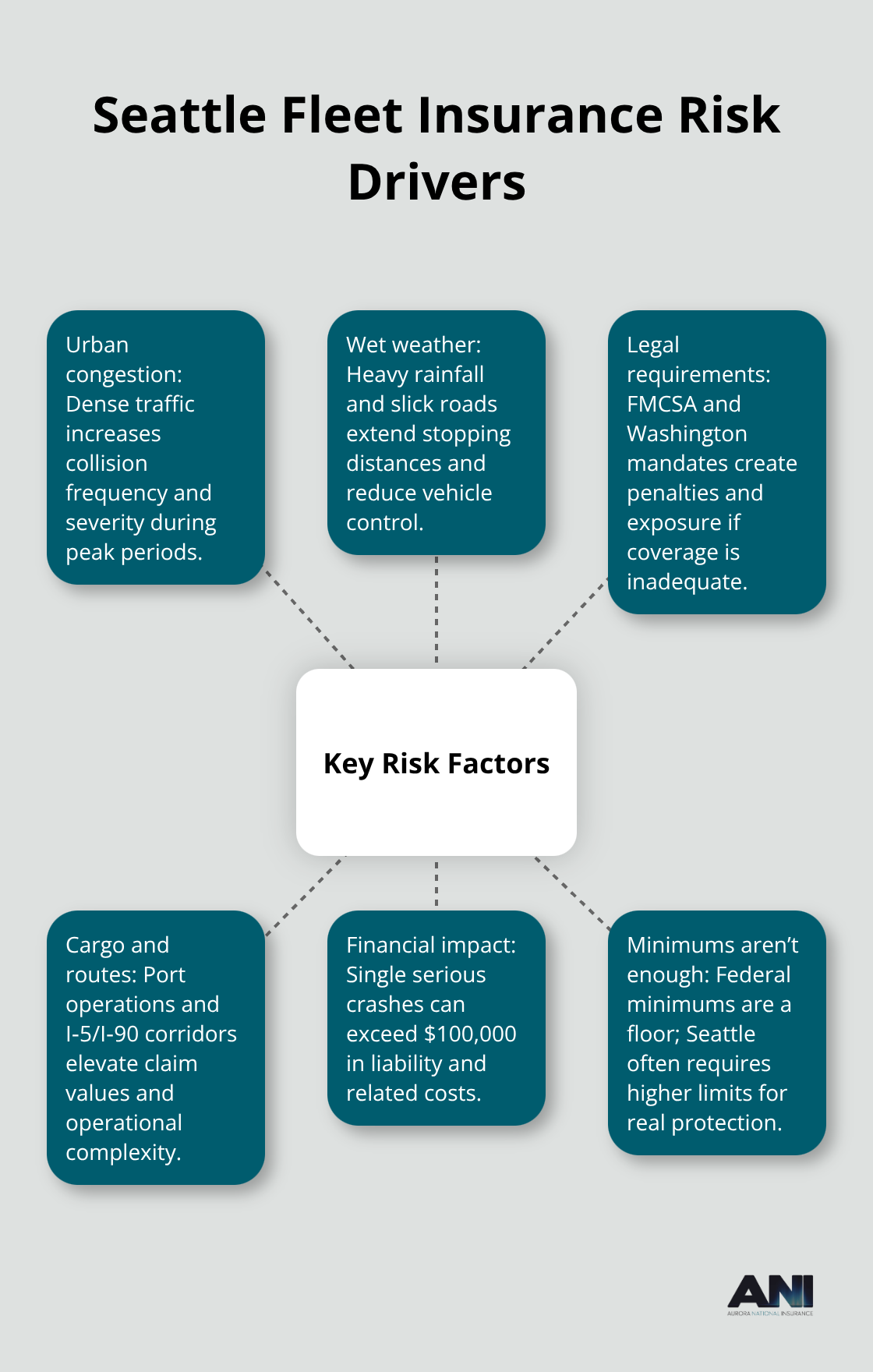

Seattle’s traffic ranks among the worst in the nation. The Seattle area experiences some of the heaviest congestion in America, with commute times regularly exceeding 40 minutes during peak hours according to transportation data. When your fleet operates in this environment, accident odds spike dramatically. Urban congestion forces more vehicles into tight spaces, creates more frequent stops and starts, puts more distracted drivers on crowded streets, and multiplies collision opportunities.

A single accident involving one of your commercial vehicles can result in liability claims exceeding $100,000 or more, depending on injury severity and property damage.

Wet Weather Multiplies Your Exposure

The Pacific Northwest experiences heavy rainfall and winter storms that increase accident risk significantly. NOAA data shows the Seattle area receives roughly 38 inches of rain annually, with wet conditions persisting from fall through spring. Wet pavement reduces tire grip, increases stopping distances, and makes vehicles harder to control-especially larger commercial trucks and vans. Fleet operators who fail to account for weather-related risk in their coverage often find themselves underinsured when accidents happen in poor conditions. Weather-aware routing and proactive vehicle maintenance help reduce these incidents, but proper insurance coverage remains your financial backstop when weather claims occur.

Legal Requirements Aren’t Optional

Washington state requires all commercial vehicles to carry minimum liability coverage of $750,000 for most interstate operations, according to FMCSA standards. This isn’t a suggestion-it’s a legal mandate. Operating without adequate coverage exposes your business to fines, license suspension, and personal liability that could devastate your operation. Beyond federal minimums, Seattle’s urban environment and complex traffic patterns make higher liability limits a practical necessity. Many fleet operators discover too late that minimum coverage falls short when claims exceed state requirements.

Why Minimum Coverage Falls Short

Federal FMCSA requirements set a floor, not a ceiling. Most Seattle fleets operate in conditions that demand more protection than the bare minimum provides. Urban density, weather exposure, and the value of cargo moving through the region (especially through the Port of Tacoma and along I-90) mean that a single serious accident can generate claims well above $750,000. Higher liability limits cost more upfront but protect your business when claims actually happen. Operating legally means understanding both federal FMCSA requirements and Washington state regulations, then building coverage that actually protects your business rather than just meeting the bare minimum.

What Comes Next

Understanding the risks Seattle fleets face is the first step. The next critical decision involves selecting the right coverage types to address these specific threats-and that choice determines whether your insurance actually protects your operation or leaves you exposed when you need it most.

What Coverage Actually Protects Your Seattle Fleet

Liability Coverage Forms Your Foundation

Liability coverage forms the foundation of any commercial vehicle policy, and Seattle’s dense urban environment demands limits well above the federal minimum. The FMCSA requires $750,000 in liability coverage for interstate operations, but that threshold reflects a baseline, not best practice for Seattle fleet owners. A single serious accident involving multiple vehicles or pedestrians in downtown Seattle or along the I-5 corridor generates bodily injury claims exceeding $500,000 alone. Seattle fleets should carry liability limits of at least $1,000,000 per accident to account for the region’s urban complexity, medical costs, and litigation expenses. When another driver or pedestrian suffers severe injuries in an accident your vehicle causes, liability coverage pays their medical bills, lost wages, and pain-and-suffering damages up to your policy limit. Without adequate limits, your business absorbs any claims beyond coverage, which can mean personal bankruptcy for fleet owners. Property damage liability protects you when your vehicle damages someone else’s vehicle, building, or infrastructure-critical coverage in Seattle where bridge repairs and vehicle damage claims routinely exceed $50,000.

Physical Damage Coverage Keeps Your Fleet Operational

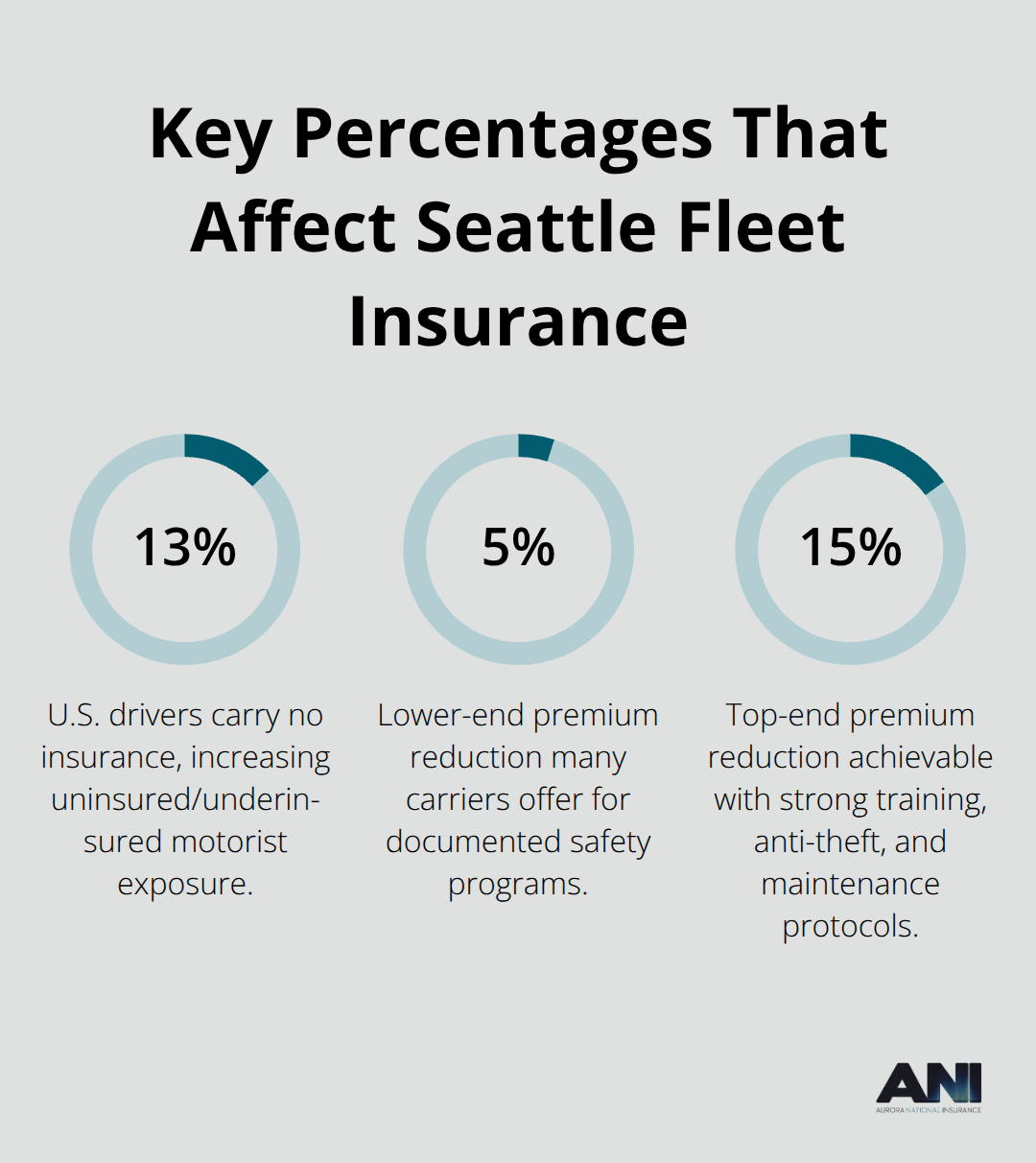

Physical damage coverage protects your own vehicles from collision, theft, weather, and vandalism-expenses that directly impact your ability to keep the fleet operational. A single commercial van replacement in Seattle costs $35,000 to $60,000 depending on equipment and customization, and a collision forces weeks of downtime while repairs complete. Comprehensive coverage (non-collision losses) addresses weather damage, theft, and vandalism that plague Seattle fleets during wet months and in urban parking environments. Collision coverage pays repair or replacement costs after accidents, with deductibles typically ranging from $500 to $2,500. Uninsured and underinsured motorist coverage protects your drivers and business when the at-fault driver lacks adequate insurance-a realistic scenario given that roughly 13 percent of drivers nationwide carry no insurance.

Medical Payments and Workers Compensation Protect Your Team

Medical payments coverage covers immediate medical expenses and funeral costs for your drivers and passengers, reducing the financial impact of injuries and keeping your operation moving forward. Workers compensation insurance protects employees injured on the job, covering medical expenses and a portion of lost wages according to Washington state requirements. Washington mandates workers compensation for most employers with employees, with rates varying by job classification and safety record. A driver with a strong safety record and formal training qualifies for lower workers compensation premiums, creating direct financial incentive for driver safety programs.

Non-Owned Auto Coverage Closes Critical Gaps

Non-owned auto coverage extends protection when your employees drive vehicles they own or lease for business purposes, closing a gap that personal auto policies explicitly exclude. This coverage becomes essential when your operation relies on owner-operators or when drivers occasionally use personal vehicles for fleet-related tasks. The cost of this endorsement remains minimal compared to the exposure your business faces without it. Your next decision involves identifying which insurance provider can deliver these coverage types with the local expertise and claims support that Seattle fleet operations demand.

Selecting the Right Insurance Provider for Your Fleet

Compare Quotes from Multiple Carriers

Getting competitive quotes from multiple carriers matters far more than most Seattle fleet owners realize. Access to 30 or more insurance markets allows independent agents to compare coverage options and pricing that you cannot access alone, which directly impacts your bottom line. When you contact carriers individually, you receive one quote at a time with no basis for comparison-a process that wastes weeks and leaves you vulnerable to overpaying. A qualified independent agent in Washington pulls quotes from highly rated providers simultaneously, showing you side-by-side comparisons of liability limits, deductibles, and annual premiums. The difference between the cheapest and most expensive quote for identical coverage often exceeds $2,000 to $5,000 annually for Seattle fleets, according to industry data on commercial auto pricing variations.

Request quotes that specify your actual fleet operating patterns: number of vehicles, annual miles, driver ages and experience, cargo types (especially if you haul through the Port of Tacoma), and routes along I-90 or I-5. Vague quotes produce inaccurate pricing and waste your time during the selection process.

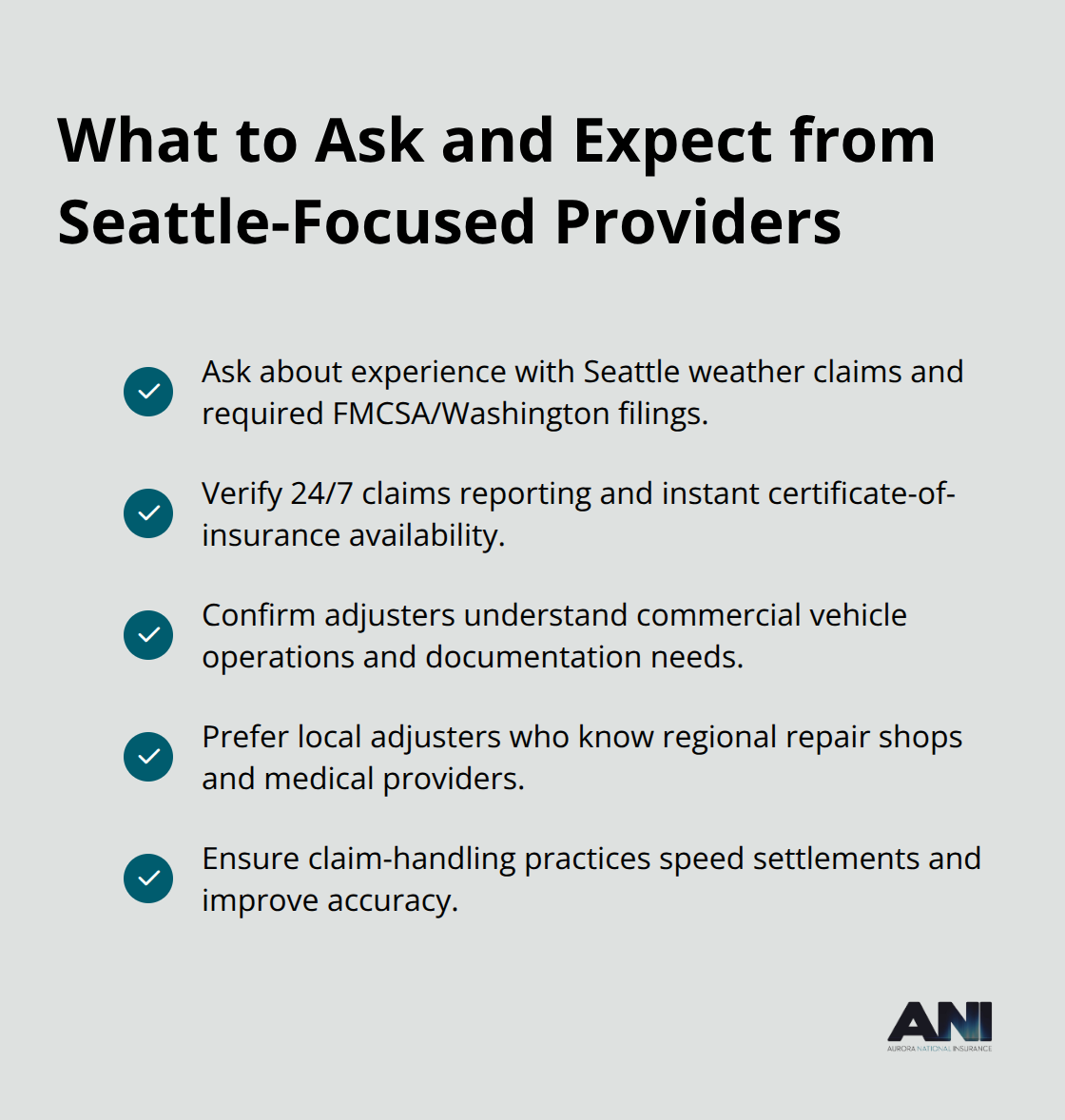

Verify Local Expertise and Claims Support

Local expertise separates providers who understand Seattle’s specific risks from those offering generic coverage. A provider with genuine Pacific Northwest experience knows that wet pavement conditions from October through April create measurable claim patterns, understands bridge crossing exposures along regional routes, and recognizes that port-related operations demand specialized cargo coverage. Agents unfamiliar with Seattle conditions often miss critical coverage gaps or recommend limits below what your actual exposure demands.

Ask potential providers about their experience with weather-related claims, their familiarity with FMCSA and Washington DOT filing requirements, and whether they’ve worked with fleets operating similar routes and cargo types to yours. Claims support matters when accidents actually happen. A provider offering 24/7 claims reporting, instant certificate-of-insurance downloads, and direct communication with adjusters who understand commercial vehicle operations will minimize your downtime and stress during claims.

Some carriers route claims through national call centers staffed by representatives unfamiliar with Seattle operations; others employ local adjusters who understand regional repair shops, medical providers, and cost structures. This distinction directly affects claim settlement speed and accuracy.

Identify Discount Opportunities

Discount opportunities exist across safety programs, fleet size, and loss history, but only if your provider actively identifies and applies them. Anti-theft devices, driver safety training programs, and formal maintenance schedules reduce claim frequency and severity, which carriers recognize through premium reductions ranging from 5 to 15 percent depending on the program. A fleet with documented driver training, telematics monitoring, and preventive maintenance records qualifies for substantially lower premiums than an identical fleet without these programs.

Request specific discount information during the quoting process and ask whether discounts apply immediately or require documentation of completed programs. Your provider should explain exactly which safety investments produce measurable premium savings.

Review Coverage Options and Endorsements

Coverage options beyond basic liability and physical damage address Seattle-specific exposures that standard policies often exclude. Inland marine coverage protects fleet equipment and tools; non-owned auto endorsements cover owner-operators; and higher uninsured motorist limits protect against the estimated 13 percent of drivers operating without adequate insurance. Verify that any quote includes medical payments coverage for your drivers, workers compensation compliance with Washington requirements, and appropriate cargo coverage if you transport goods.

The cheapest quote frequently lacks critical endorsements, which means you discover coverage gaps only after an accident occurs. A thorough review of what each quote actually covers prevents expensive surprises later.

Final Thoughts

Seattle fleet owners operate in one of America’s most challenging environments for commercial vehicles, where high traffic density, wet weather exposure, and strict regulations demand insurance coverage that exceeds federal minimums. The right Seattle commercial vehicle insurance protects your business from accidents that could otherwise devastate your operation, but selecting that coverage requires understanding both your actual risks and what different providers genuinely offer. Your next step involves gathering quotes from multiple carriers that understand Pacific Northwest conditions, since generic quotes from national providers miss Seattle-specific exposures like weather-related claims, port operations, and bridge crossing risks.

Request detailed quotes that reflect your actual fleet size, routes, cargo types, and driver experience, then compare not just premiums but what each quote actually covers-liability limits, physical damage protection, workers compensation compliance, and critical endorsements like non-owned auto coverage and uninsured motorist protection. Local agents matter because they access multiple carriers simultaneously, identify discount opportunities you’d miss alone, and understand which coverage gaps matter most for Seattle operations. An agent familiar with regional claims patterns, FMCSA and Washington DOT requirements, and local repair costs will recommend limits and endorsements that actually protect your business rather than just meeting legal minimums.

Get an instant online quote to see how competitive pricing and tailored coverage compare to what you’re currently paying for your fleet. Your fleet’s protection depends on making informed decisions now, before an accident forces you to discover what your current coverage actually covers.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.