Alaska Home Insurance Rates: What Impacts Your Premium

Alaska home insurance rates vary significantly based on where you live and how you protect your property. At Aurora National Insurance, we’ve seen firsthand how small changes in your home or coverage choices can shift what you pay each month.

This guide walks you through the specific factors that shape your premium and shows you concrete ways to reduce your costs without sacrificing protection.

What Pushes Your Alaska Premium Higher

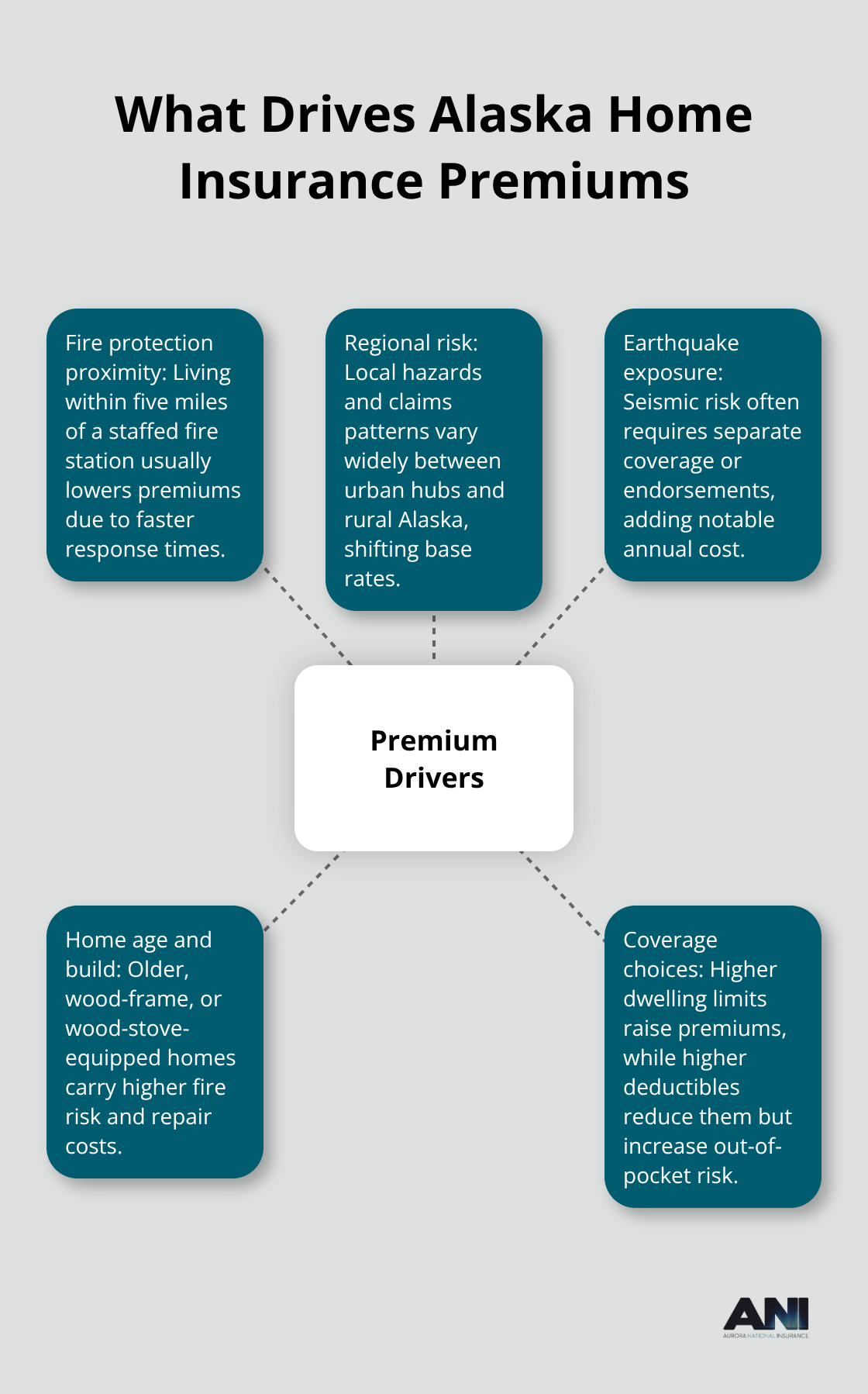

Where you live in Alaska matters more than most homeowners realize. If your house sits within five miles of a fire station, you’ll pay significantly less than someone farther away-and that gap only widens in rural areas where fire protection is nonexistent or severely limited. This isn’t theoretical; it’s a direct calculation insurers make based on response times and property risk.

Your region within Alaska shapes costs dramatically. Anchorage homeowners pay around $954 annually on average, while Juneau residents face $955, and rural Alaska climbs to $2,000–$3,500 yearly, according to The Zebra. These differences reflect actual claims data and local hazard exposure.

Earthquake Risk Adds Substantial Cost

Earthquake risk compounds this regional picture. Alaska experiences roughly 1,503 earthquakes per year, yet standard homeowners policies exclude earthquake damage entirely. Adding earthquake coverage costs about $116 annually for basic endorsements, but premiums jump substantially-Liberty Mutual’s earthquake endorsement brings the total to $598 yearly, while USAA reaches $1,011 with the same addition. You cannot ignore this gap if you live in Alaska.

How Your Home’s Age and Build Affect What You Pay

Older homes cost more to insure, and construction type explains much of the difference. Wood-frame houses carry higher fire risk than brick or masonry, so you’ll pay more for frame construction. Wood furnaces and wood stoves further raise premiums or limit coverage entirely because insurers view them as genuine fire hazards.

A metal roof qualifies for discounts up to 5–15% because it resists fire and weather damage better than asphalt shingles. The age of your home directly impacts insurability too; some insurers hesitate to cover homes beyond a certain age or restrict coverage options. Newer construction often qualifies for discounts, making a recent build a financial advantage.

Coverage Choices That Hit Your Wallet Hardest

Your dwelling coverage limit and deductible choice create the biggest swings in what you actually pay. Increasing your deductible from $500 to $2,000 drops your premium by roughly $182 annually, according to The Zebra’s Alaska data. A $5,000 deductible cuts it further to around $819 yearly. The trade-off is real-you pay more out-of-pocket on claims-but if you can absorb that cost, the savings compound over years.

Dwelling coverage amounts tell the same story. Moving from $100,000 to $250,000 in dwelling coverage adds approximately $420 yearly; jumping to $400,000 costs roughly $877 more per year. Calculate your home’s true replacement cost with your agent before choosing limits, because underinsuring leaves you exposed to catastrophic loss, while overinsuring wastes money month after month. Once you understand how these factors shape your rate, you can take action to reduce what you pay without cutting corners on protection.

Cutting Your Alaska Home Insurance Costs

Bundle Policies to Unlock Immediate Savings

Bundling your home and auto policies with the same insurer saves roughly $94 annually on average in Alaska. Insurers reward customers who consolidate coverage, and the savings compound if you add life insurance or other policies to the mix, potentially reaching 20–25% discounts across your entire portfolio. Start by requesting a multi-policy quote from your current insurer, then compare that bundled rate against competitors offering the same combination. Most homeowners leave this money on the table simply because they never ask.

Install Security and Fire Safety Systems

Security systems and fire alarms lower your premium by 10–20% in most Alaska markets. A monitored burglar alarm or fire detection system signals to insurers that you’ve reduced the likelihood of theft or fire damage, so they price your policy accordingly. Metal roofs and fire-resistant building materials qualify for additional discounts ranging from 5–15%.

If you’re considering a roof replacement anyway, the insurance savings help offset the upfront cost over time. Deadbolt locks, sprinkler systems, and winterization measures also qualify for reductions. Document these improvements with photos and receipts, then notify your insurer to confirm the discounts apply at your next renewal.

Protect Your Claims History

Your claims history directly shapes what you pay going forward. A clean record-no claims filed in the past three to five years-can earn you 10–20% loyalty discounts that accumulate over time. Multiple claims flag you as higher-risk, pushing premiums upward regardless of other factors. File claims only for losses that exceed your deductible by a meaningful margin; a $500 water damage claim against a $1,000 deductible makes no financial sense and damages your record. Instead, absorb smaller losses and reserve claims for genuine catastrophes. Alaska’s remote locations and limited contractor availability mean repair costs run higher than the Lower 48, so raising your deductible to $1,500 or $2,000 saves you money annually while protecting you against the truly expensive losses.

Shop Multiple Carriers Every Few Years

Shop your policy every two to three years across at least five different carriers, because rates shift as local claims data changes and insurers adjust their risk models. Liberty Mutual, Country, and Umialik consistently rank among Alaska’s most affordable options, but your specific situation may yield better quotes elsewhere. Getting multiple quotes takes time, yet the potential savings of $200–$400 annually make the effort worthwhile. Once you’ve identified your best rate and locked in discounts, the next step involves understanding what coverage gaps might still exist in your policy.

Comparing Alaska Home Insurance Quotes

Shopping for Alaska home insurance quotes requires a systematic approach, not a casual glance at one or two carriers. Most Alaskans accept whatever rate they’re quoted first, which costs them hundreds of dollars annually. The reality is that Alaska’s insurance market fragments across carriers with vastly different pricing models. Liberty Mutual averages $727 yearly in Alaska, Country sits at $801, and Umialik reaches $1,038 for identical coverage-that’s a $311 difference on the cheapest option alone.

Get Multiple Quotes from Different Carriers

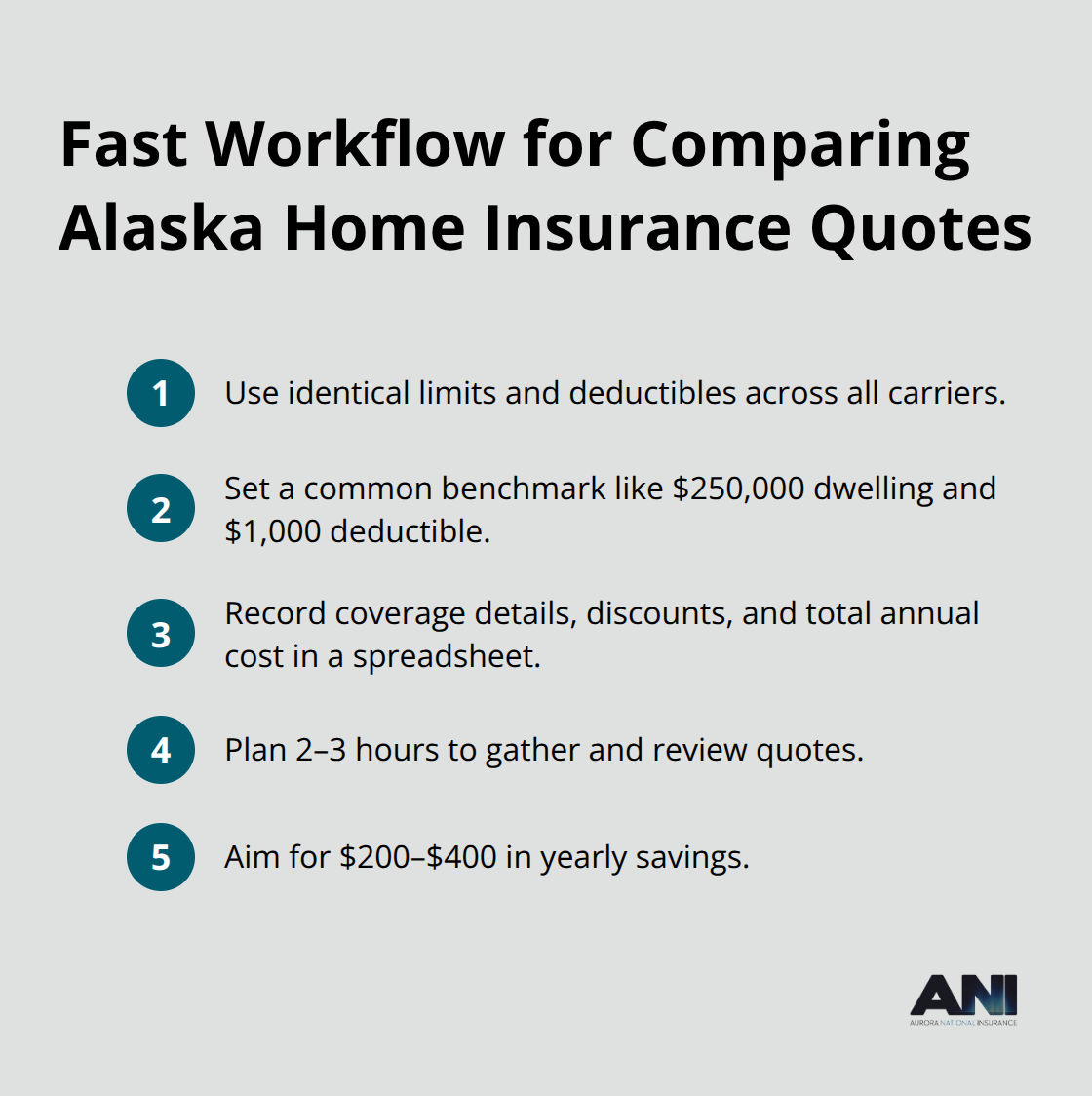

Your specific home, location, and claims history may shift these rankings entirely, which means comparing at least five quotes across different carriers becomes non-negotiable. Start with Liberty Mutual, Country, and Umialik as baseline carriers, then request quotes from State Farm, USAA if you’re military-eligible, and PEMCO. Each carrier weights earthquake risk, fire protection proximity, and home age differently, so the cheapest option for your neighbor may not be cheapest for you.

Request quotes with identical coverage limits and deductibles across all carriers so you’re comparing apples to apples-dwelling coverage of $250,000 with a $1,000 deductible works as a standard benchmark. Document each quote’s coverage details, discounts applied, and total annual cost in a spreadsheet. This process takes two to three hours but saves $200–$400 yearly for most homeowners.

Understand What Coverage You Actually Need

Calculate your home’s true replacement cost-not its market value-with your insurance agent, because replacement cost excludes land value and reflects what it costs to rebuild from scratch. Alaska replacement costs typically run around $228 per square foot, so a 2,000-square-foot home might cost $456,000 to rebuild depending on materials and location. Try targeting 125–150% of replacement cost for dwelling coverage to account for inflation and unforeseen expenses.

Earthquake coverage requires its own separate policy or endorsement in Alaska, not a standard add-on, and costs roughly $116 for basic endorsements though premiums climb to $300–$600 annually depending on your carrier and home value. Flood insurance comes separately through FEMA’s National Flood Insurance Program or private carriers, with NFIP limits capping at $250,000 for structure and $100,000 for personal property. Water backup coverage protects against sewer backups and sump pump failures-critical in Alaska’s wet seasons and freeze-thaw cycles. Service line coverage pays for repairs to water and sewer lines on your property, a major expense in remote areas where contractor availability limits options.

Review Your Policy Annually for Rate Changes

Review your policy annually because rates shift as local claims data changes, new discounts become available, and your home’s condition improves or deteriorates. Set a calendar reminder for your policy renewal date three months prior, then request updated quotes from three to five carriers. If your current insurer’s renewal rate jumped more than 5–10%, that signals it’s time to switch.

Alaska’s disaster risks demand this vigilance-earthquake activity, permafrost settlement, frozen pipes, and ice dams create claim patterns unique to the state, so insurers continuously adjust their pricing models based on emerging data.

Final Thoughts

Alaska home insurance rates reflect factors both inside and outside your control. Fire protection proximity, earthquake risk, and regional claims data sit beyond your influence, yet your home’s condition, coverage choices, and shopping decisions directly shape what you pay each month. The gap between the cheapest and most expensive quotes for identical coverage often exceeds $300 annually, which means accepting the first rate you receive costs you thousands over a decade.

Start by calculating your home’s true replacement cost with an agent, then request quotes from at least five carriers using identical coverage limits and deductibles. Document each quote carefully so you can compare actual pricing rather than guessing which option works best. Bundle your home and auto policies to capture immediate savings of roughly $94 yearly, then layer on security system discounts and fire-resistant building material credits. Raise your deductible to $1,500 or $2,000 if you can absorb that out-of-pocket cost, because the annual premium reduction compounds significantly over time.

Protect your claims history by filing claims only for losses that substantially exceed your deductible. Alaska’s remote locations and limited contractor availability mean repair costs run higher than the Lower 48, so a clean record matters more here than in other states. Get an instant online quote today and see how much you could save by shopping your Alaska home insurance rates properly.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.