Oregon Home Insurance Rates: What Impacts Your Policy Price

Your Oregon home insurance rates depend on far more than just where you live. At Aurora National Insurance, we’ve seen homeowners overpay simply because they didn’t understand what drives their premiums.

The good news? Most rate factors are within your control. This guide walks you through exactly what impacts your costs and how to find better coverage without sacrificing protection.

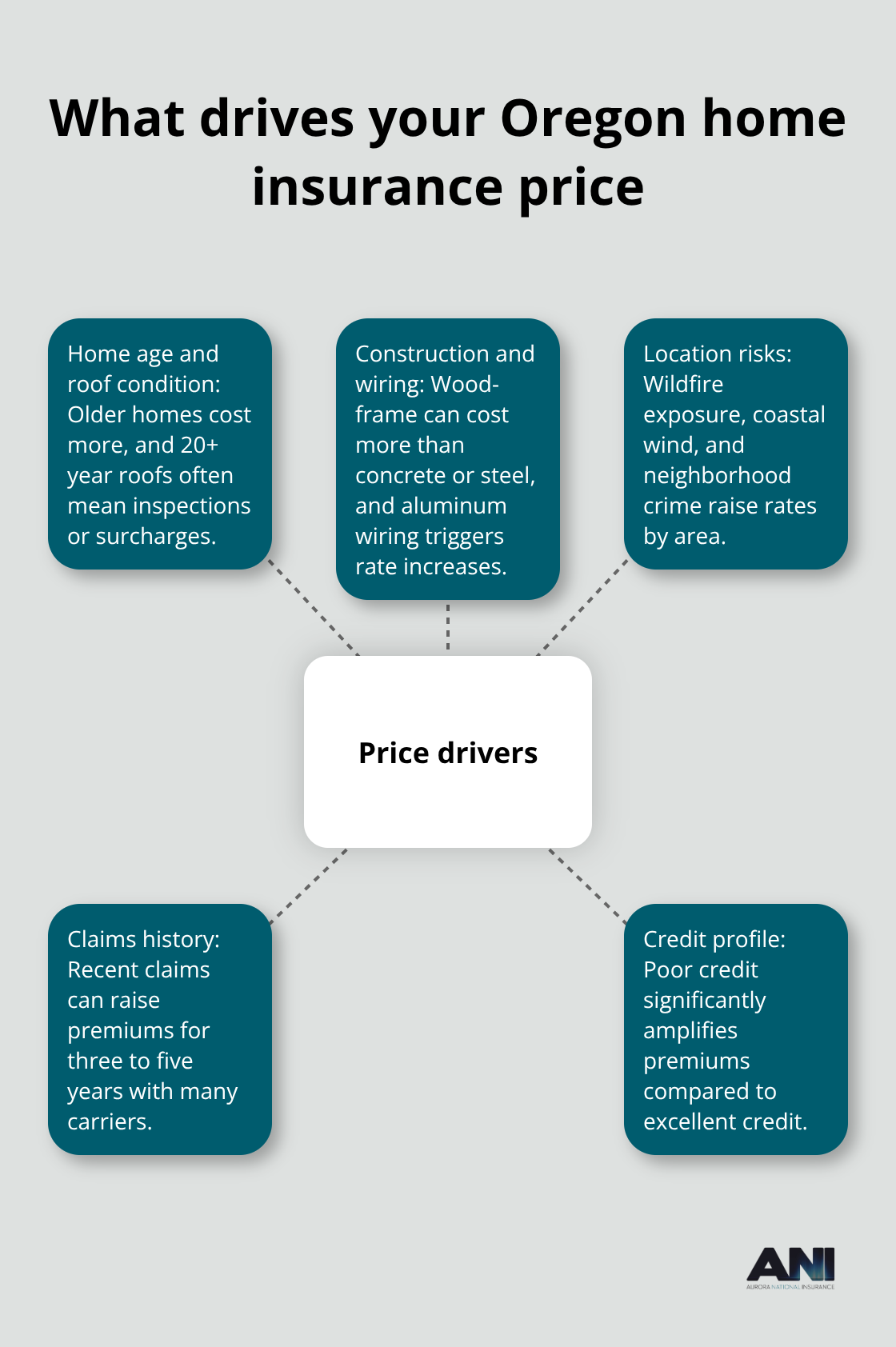

What Really Drives Your Oregon Home Insurance Price

Your home’s age and construction directly shape what insurers charge. Older homes cost significantly more to insure because rebuilding them to modern code standards requires substantial investment. If your roof exceeds 20 years old, expect higher premiums-many carriers require roof inspections or impose surcharges. Homes built before 1978 often face additional costs due to potential asbestos or outdated electrical systems. The materials matter too: wood-frame houses typically cost more to insure than those with concrete or steel, and homes with aluminum wiring trigger rate increases. If you’ve recently replaced your roof with fire-resistant materials, that upgrade becomes a genuine selling point to insurers and warrants mention when you quote.

How location multiplies your costs

Where your home sits in Oregon determines a huge portion of your premium. Wildfire losses in Oregon have caused nearly $3 billion in estimated losses in the 2020s alone, pushing rates higher across fire-prone regions. Coastal properties face wind and storm exposure that inland homes avoid. Properties near forests carry substantially higher wildfire risk premiums than those in suburban Portland. Even within the same city, your neighborhood’s crime rate affects pricing-Oregon’s burglary rate ranked in the top ten nationally in 2022, and insurers price that risk into policies for high-crime areas. A home in Hillsboro averages around $963 per year for $300,000 in dwelling coverage, while Maupin runs about $1,489 annually for identical coverage, illustrating how dramatically location shifts your actual costs.

Your claims and credit history matter more than you think

A single claim raises your rates for three to five years. Two or more claims in the past five years signals higher risk to insurers, and they price accordingly. Poor credit significantly amplifies your premium-homeowners with excellent credit pay thousands less annually than those with poor credit scores for the same coverage. Insurers view credit as a predictor of claim likelihood and payment reliability. Check your CLUE report before shopping to see what claims history follows your property, including losses from previous owners. If you’ve had no claims in five years, that fact becomes leverage when negotiating with carriers or shopping for better rates.

What happens next when you shop

Understanding these three factors positions you to make smarter decisions as you compare policies and carriers across Oregon.

Ways to Cut Your Oregon Home Insurance Premiums

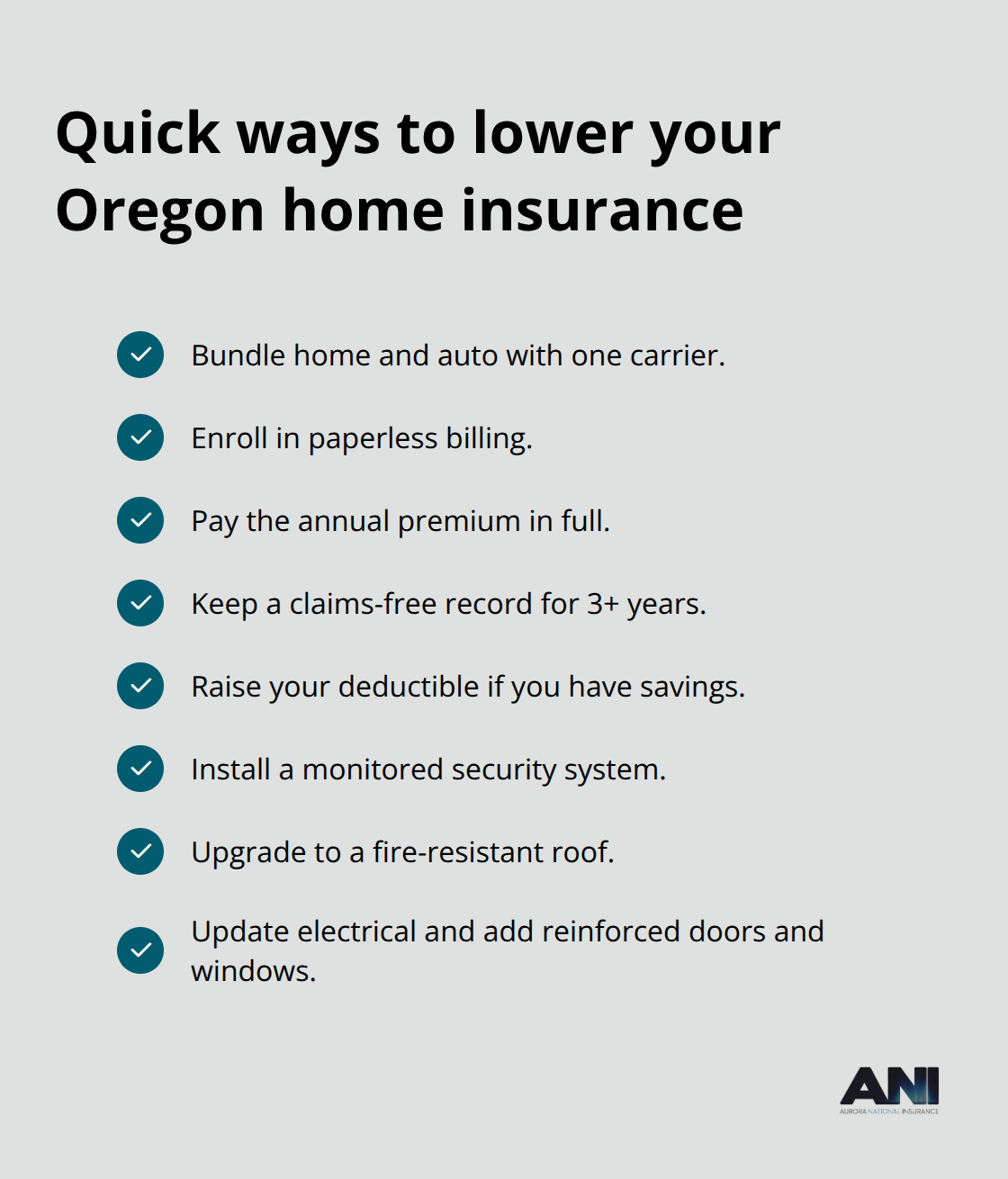

Bundling your home and auto policies with the same carrier typically saves you money on your combined premiums, making it one of the fastest ways to lower costs without sacrificing coverage. When you consolidate policies, insurers reward loyalty and reduce their administrative expenses, passing savings directly to you. If you currently split home and auto between different carriers, shopping for a bundle quote should be your first move. Many Oregon carriers also offer additional discounts for paperless billing, paying your annual premium in full upfront, or maintaining a claims-free history for three or more years. These stacked discounts compound quickly-a homeowner with bundled policies, paperless statements, and a clean claims record can easily save 30 percent or more versus baseline rates.

Raising your deductible works if you have savings

Increasing your deductible from $500 to $1,500 typically reduces your annual premium by 10 to 15 percent. Jumping to a $5,000 deductible can cut costs by 25 to 40 percent depending on your carrier and location. The catch is simple: you must have enough cash reserves to cover that deductible after a loss. If a $5,000 deductible would strain your finances, stick with $1,000 or $1,500. This strategy only works for homeowners who genuinely won’t need to file small claims. Someone filing two claims in five years erases any premium savings, so be honest about your risk tolerance and claims likelihood before committing to a higher deductible.

Home improvements deliver real rate reductions

A new roof installed with fire-resistant materials can lower your premium 5 to 15 percent, depending on your carrier and location. Updated electrical systems, reinforced garage doors, and deadbolt locks on all exterior doors also qualify for discounts with most Oregon insurers. Storm-resistant windows and doors earn additional discounts in coastal or wind-prone areas. Installing a monitored security system typically saves 5 to 10 percent annually. You must document these improvements with receipts and photos before your renewal date, then explicitly mention them when you quote with new carriers. Insurers won’t automatically discover roof replacements or security upgrades-you must tell them. If you’re planning renovations anyway, timing them before your policy renewal maximizes the financial benefit.

What to do when you’re ready to shop

These three strategies form your foundation for negotiating better rates. The next step involves comparing what different carriers actually charge for your specific situation and coverage needs.

Shopping for the Best Oregon Home Insurance Rates

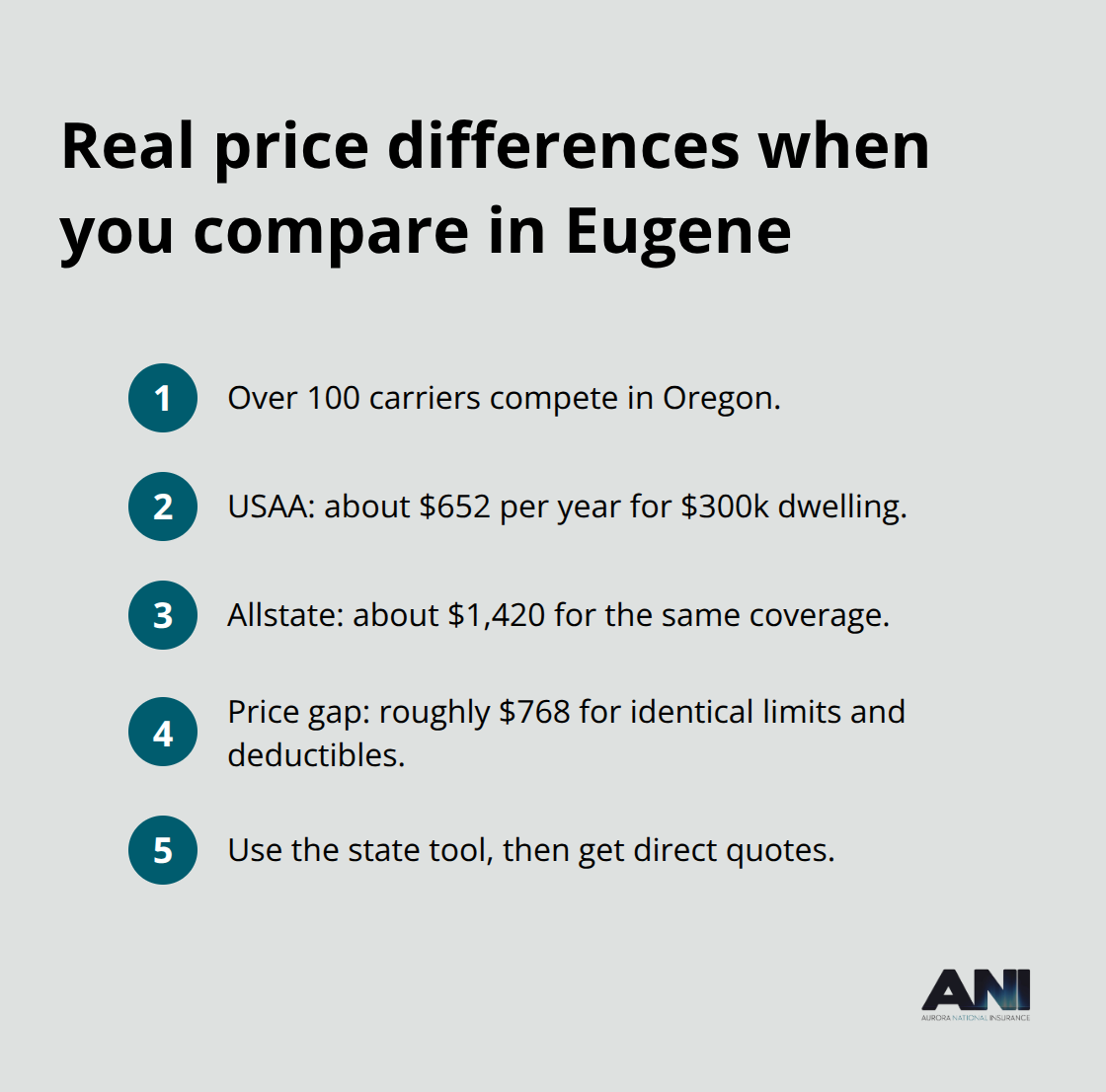

Compare quotes from multiple carriers to find real savings

Oregon has over 100 companies writing homeowners policies, and the difference between the cheapest and most expensive carrier for your exact situation can exceed $800 annually. USAA charges around $652 per year for $300,000 in dwelling coverage in Eugene, while Allstate runs approximately $1,420 for identical coverage in the same city. That $768 gap exists for the same house, same coverage, same deductible.

The Oregon Division of Financial Regulation offers a home insurance shopping tool that lets you compare multiple insurers side-by-side, eliminating the tedious process of calling ten different companies. Start there, then supplement with direct quotes from carriers not included in that tool.

When you obtain quotes, keep every variable constant: same dwelling limit, same deductible, same coverage types. Changing even one element makes comparison meaningless. Most carriers let you quote online in under five minutes, so spending 20 minutes gathering four or five quotes costs nothing but saves hundreds of dollars.

Set your coverage limits to match replacement costs

Your coverage limits directly control your premiums, and many homeowners get this wrong. Insuring your home to its full replacement value costs more upfront but protects you from financial disaster. If your home would cost $400,000 to rebuild today and you only carry $250,000 in coverage, you absorb the $150,000 gap after a total loss.

The 80 percent coinsurance rule means underinsuring your home can result in prorated claim payouts, leaving you with even less than your coverage limit suggests. Construction inflation has significantly increased rebuilding costs in recent years. Try a current replacement-cost estimate from a contractor or use your carrier’s valuation tool, then match your dwelling limit to that figure.

Choose a deductible you can actually afford

The choice between $500 and $1,500 shifts your annual premium by roughly 10 to 15 percent, while jumping to $5,000 can cut costs 25 to 40 percent. Pick the deductible you can actually afford to pay after a loss, not the one that looks good on paper. An independent broker licensed in Oregon can shop across dozens of carriers simultaneously, saving you hours and often uncovering discounts you’d miss working alone. Many brokers charge nothing since they earn commissions from insurers, making their service genuinely free.

Final Thoughts

Your Oregon home insurance rates reflect three core factors: your home’s age and construction, your location’s risk profile, and your personal claims and credit history. While you cannot change where your house sits or its original build year, you control how you maintain it and what coverage you carry. The strategies that work are straightforward: bundle policies for immediate savings, raise your deductible if you have emergency funds, and invest in improvements like new roofs or security systems that insurers reward with lower premiums.

Shopping across multiple carriers matters more than any single discount. Oregon’s competitive market means the difference between carriers for your exact situation regularly exceeds $700 annually. Spending 20 minutes to gather quotes from four or five companies costs nothing and often saves hundreds. Use the Oregon Division of Financial Regulation’s shopping tool as your starting point, then supplement with direct quotes from carriers you want to evaluate.

Set your dwelling coverage to match your home’s actual replacement cost, not an arbitrary number. Choose a deductible you can genuinely afford to pay after a loss, not one that looks attractive on paper. These decisions shape both your premium and your actual protection, making them worth the time to get right.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.