Earthquake Home Insurance Alaska: Safeguarding Homes in Seismic Regions

Alaska experiences more earthquakes than any other U.S. state, with thousands occurring annually. Most homeowners don’t realize their standard policies leave them completely unprotected against seismic damage.

Earthquake home insurance in Alaska isn’t optional if you want real financial protection. We at Aurora National Insurance help homeowners understand what coverage they actually need and how to get it affordably.

Why Earthquake Insurance Matters in Alaska

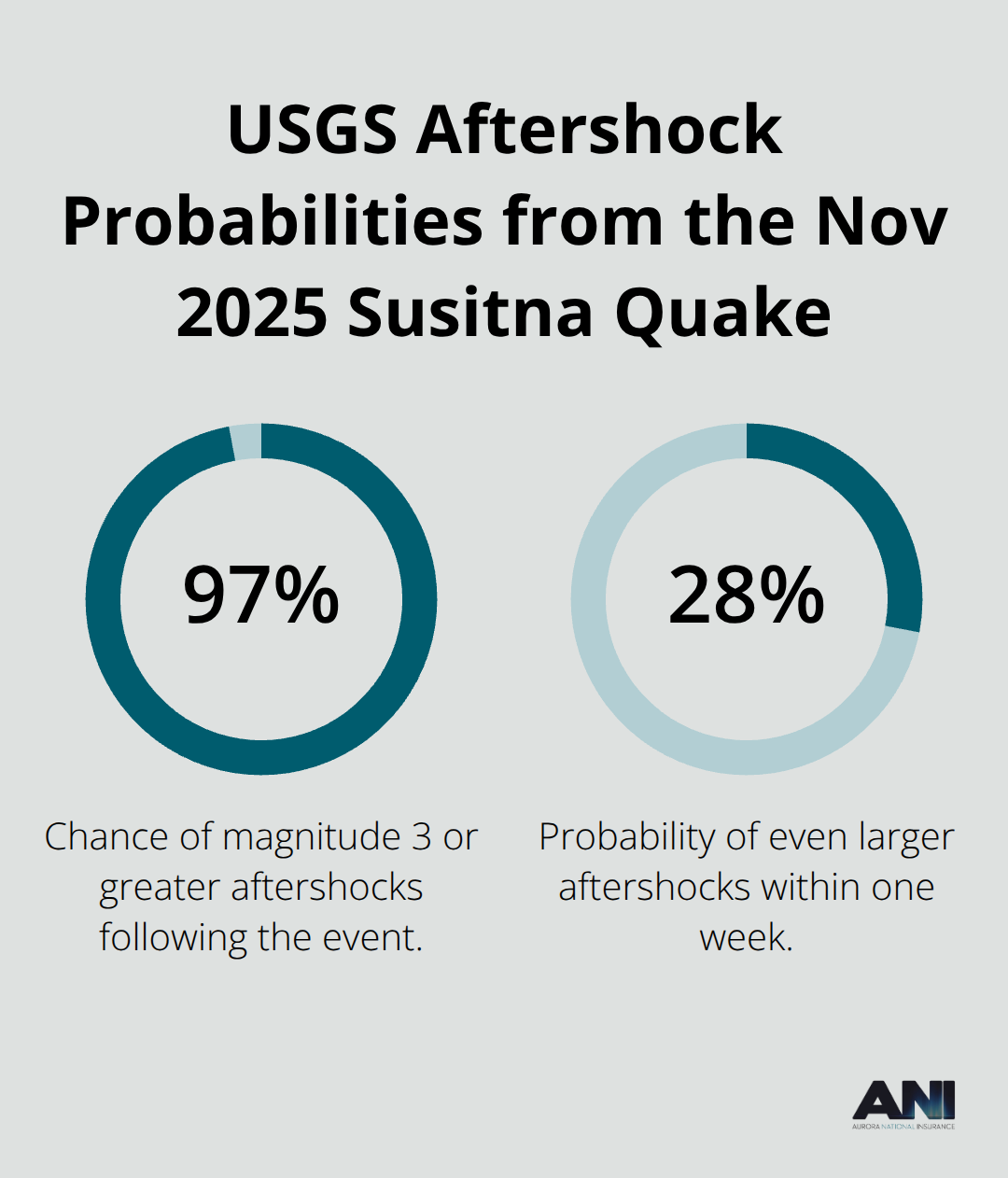

Alaska sits on one of the world’s most seismically active territories, with tens of thousands of earthquakes occurring annually. The November 2025 magnitude 6.0 quake near Susitna, located 37 miles from Anchorage, demonstrated this reality when shaking reached across the state-as far north as Fairbanks, roughly 350 miles away. The U.S. Geological Survey estimated a 97 percent chance of magnitude 3 or greater aftershocks following that event, with a 28 percent probability of even larger ones within a week. This isn’t theoretical risk; it’s your neighborhood’s baseline seismic environment.

The 2018 Anchorage earthquake remains the most costly recent event in Alaska, causing approximately $150 million in insured losses-about $193 million in today’s dollars-with damage concentrated in municipal infrastructure, schools, utilities and transportation networks. Standard homeowners policies do not cover earthquake damage from ground shaking, leaving most Alaska homeowners financially exposed when these events occur.

Standard Homeowners Insurance Leaves You Unprotected

Your homeowners policy covers fire, wind, theft and many other perils, but earthquake damage remains excluded. If your home sustains structural cracking, your roof collapses, or your foundation shifts from seismic shaking, your standard policy pays nothing. Water damage from burst pipes caused by an earthquake or fire ignited by the quake itself may receive coverage under certain circumstances, but earthquake insurance covers repairs needed because of earthquake damage like shaking. This gap exists because earthquake risk is unpredictable and potentially catastrophic across entire regions simultaneously, making it impossible for insurers to pool risk the way they do with other perils. Earthquake endorsements become essential if your property sits in high-risk zones like Anchorage or southern coastal areas, though these require separate policies. Premiums vary based on your home’s location, age, construction type and proximity to known fault lines, but coverage remains affordable in Alaska compared to California rates.

Earthquake Damage Extends Far Beyond Visible Cracks

Earthquake damage reaches beyond visible structural cracks. The ground movement shifts your foundation, damages utility connections, requires soil stabilization work, and necessitates debris removal before repairs start. If your home becomes uninhabitable during reconstruction, additional living expenses-hotel costs, meals, temporary housing-add significantly to your financial burden. The Northridge earthquake in 1994 caused $33.99 billion in insured losses across Southern California, with individual homeowners facing repair bills ranging from tens of thousands to over $500,000. While Alaska has not experienced a comparable magnitude event in recent decades, the 2018 Anchorage earthquake showed that even moderate seismic activity creates widespread damage requiring extended repairs. Securing earthquake insurance now protects you from depleting savings or taking on debt when the next significant quake strikes your region.

Understanding Your Coverage Options

Earthquake insurance policies offer different coverage levels depending on your needs and budget. You can purchase coverage for your home’s structure alone, or add protection for personal property, other structures (such as detached garages), and additional living expenses if you cannot occupy your home during repairs. Coverage limits should reflect the actual cost to repair or rebuild your home, not just its appraised value or loan amount, to avoid underinsurance in a total loss. Many homeowners overlook this detail and end up with insufficient protection when they need it most. Earthquake and flood insurance will require a separate policy, and our licensed agents help you compare multiple carriers and identify the right coverage limits and deductible options for your specific situation and budget.

Understanding what earthquake insurance actually covers-and what it doesn’t-determines whether you have real protection or just a false sense of security. The next section explains exactly what these policies cover, how much they cost in Alaska, and how to obtain accurate quotes from multiple carriers.

What Earthquake Insurance Actually Covers in Alaska

Understanding Your Coverage Protection

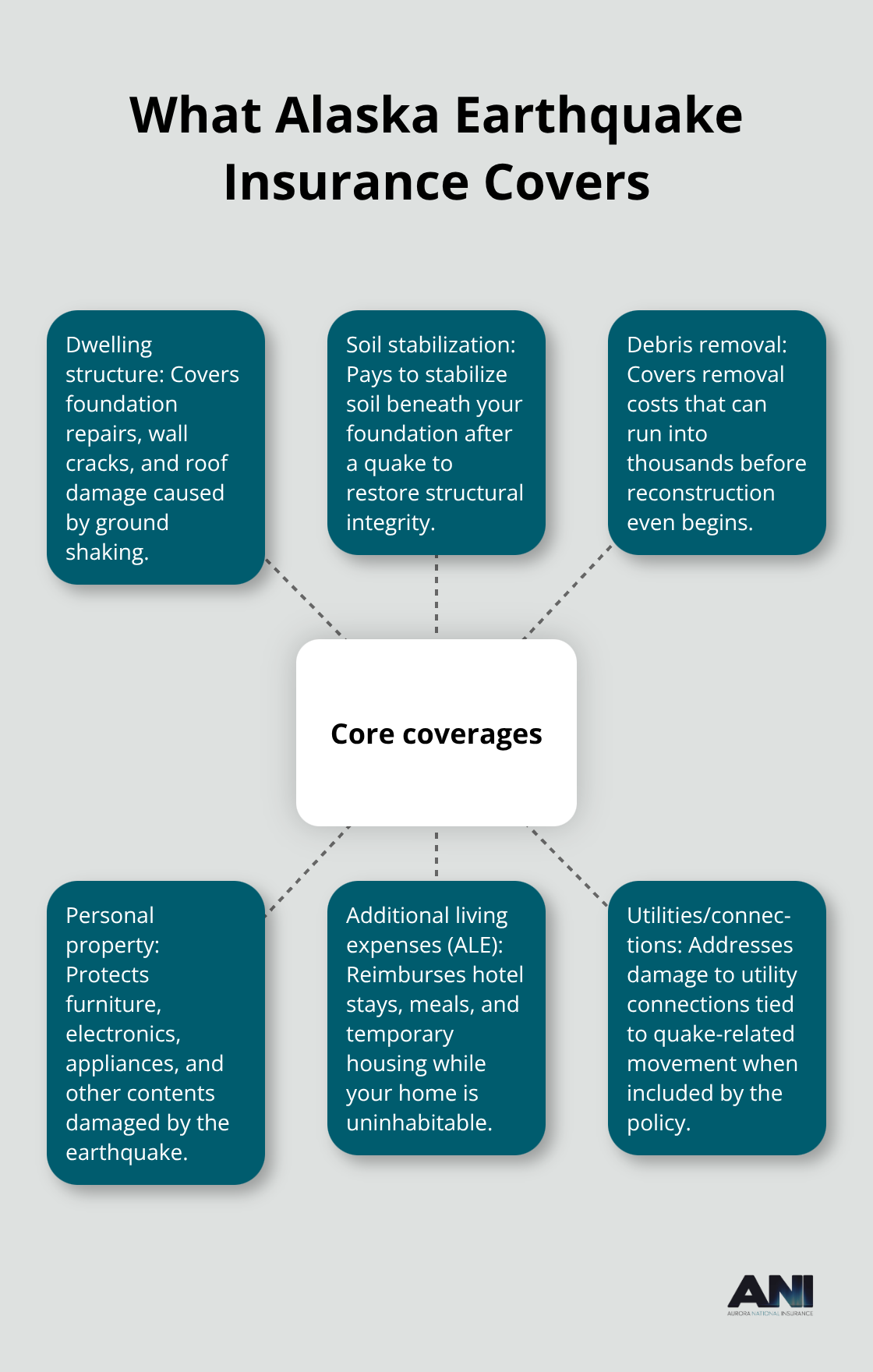

Earthquake insurance covers structural damage to your home caused by ground shaking, including foundation repairs, wall cracks, roof damage, and the cost to stabilize soil beneath your foundation after a quake. It also covers debris removal, which can run thousands of dollars before reconstruction even begins. If you add personal property coverage, your policy protects furniture, electronics, appliances and other contents damaged by the earthquake. Additional living expenses coverage reimburses hotel stays, meals and temporary housing if your home becomes uninhabitable during repairs, typically covering costs until you can return home or your policy limit is exhausted.

The 2018 Anchorage earthquake forced many families into weeks of temporary housing while repairs proceeded, making this coverage particularly valuable.

Setting Your Coverage Limits Correctly

One critical detail most homeowners miss: your coverage limit must reflect the actual cost to rebuild your home, not its appraised value or mortgage balance. If you own a home worth $400,000 to rebuild but carry only $250,000 in earthquake coverage, you absorb the remaining $150,000 in losses yourself. Alaska homeowners commonly underinsure because they focus on their loan amount rather than true reconstruction costs. You should coordinate your dwelling limit between your standard homeowners policy and earthquake endorsement to avoid gaps. This coordination prevents you from discovering insufficient protection when you need it most.

Deductibles and Premium Costs

Deductibles for earthquake insurance in Alaska typically range from 10 to 20 percent of your coverage limit, meaning a $300,000 policy with a 15 percent deductible requires you to pay $45,000 out of pocket before insurance kicks in. This differs dramatically from standard homeowners deductibles of $500 to $1,500, so you should understand your deductible structure before purchasing. Premium costs in Alaska vary significantly based on your home’s location, age, construction type and distance from known fault lines. A newer wood-frame home in Fairbanks costs substantially less to insure than an older masonry structure in Anchorage, where seismic risk concentrates near population centers. Alaska’s 2024 earthquake insurance premiums totaled roughly $60.9 million across the state, with major carriers including FM Global, Palomar Specialty, Zurich, State Farm, Berkshire Hathaway and Travelers competing for market share.

Obtaining Accurate Quotes from Multiple Carriers

You should obtain accurate quotes from multiple carriers directly rather than relying on online calculators, which often underestimate Alaska-specific risk factors. Licensed agents who understand local seismic zones can access quotes from carriers writing in your area. Multiple top-rated carriers compete for your business, and you should request quotes from at least three of them. Ask specifically about any discounts for mitigation measures like securing your water heater or fastening furniture to walls, which some insurers reward with premium reductions of 5 to 15 percent. Document your home’s age, square footage, foundation type and any recent upgrades when requesting quotes, as incomplete information leads to inaccurate pricing. Once you select a policy, activation typically occurs within days of payment, providing immediate protection against the next seismic event.

Moving Forward with Your Coverage Decision

The quotes you collect from multiple carriers reveal significant price variations and coverage options that directly impact your financial protection. Comparing these options side-by-side shows you exactly what different deductible levels cost and how coverage limits affect your out-of-pocket exposure. This comparison process prepares you to make an informed decision about which policy best matches your home’s vulnerability and your financial situation-the focus of the next chapter.

How to Choose the Right Earthquake Coverage for Your Home

Assess Your Home’s Vulnerability and Location

Your home’s earthquake risk depends on three concrete factors: its location relative to known fault lines, its construction type, and its age. Homes within 30 miles of the Susitna fault zone or Cook Inlet basin faults face substantially higher risk than properties in interior Alaska, which translates directly into higher premiums. A wood-frame home built after 2000 typically costs 30 to 40 percent less to insure than a pre-1980 masonry or unreinforced concrete structure, because older construction methods fail more readily under seismic stress. You should obtain your property’s exact distance from fault lines using the U.S. Geological Survey earthquake hazard maps, then request quotes specifically mentioning this location detail to carriers. This specificity prevents underpricing that leaves you with insufficient coverage limits when you need them.

Balance Your Deductible Against Premium Costs

The deductible percentage you select directly controls your premium cost and out-of-pocket exposure, so you face a genuine trade-off. A 10 percent deductible on a $300,000 policy means you pay $30,000 before coverage activates, while a 20 percent deductible drops your premium by 15 to 25 percent but increases your out-of-pocket to $60,000. Most Alaska homeowners choose the 15 percent middle ground, which balances affordability with manageable deductibles. When requesting quotes, specify the exact coverage limits you need based on actual rebuild costs, not appraised value, and ask each carrier about mitigation discounts for securing water heaters, fastening furniture, or upgrading your home’s seismic resistance. Licensed professionals can explain in detail the different options such as deductibles, co-pays and co-insurance to help you make an informed decision.

Compare Policies from Multiple Carriers

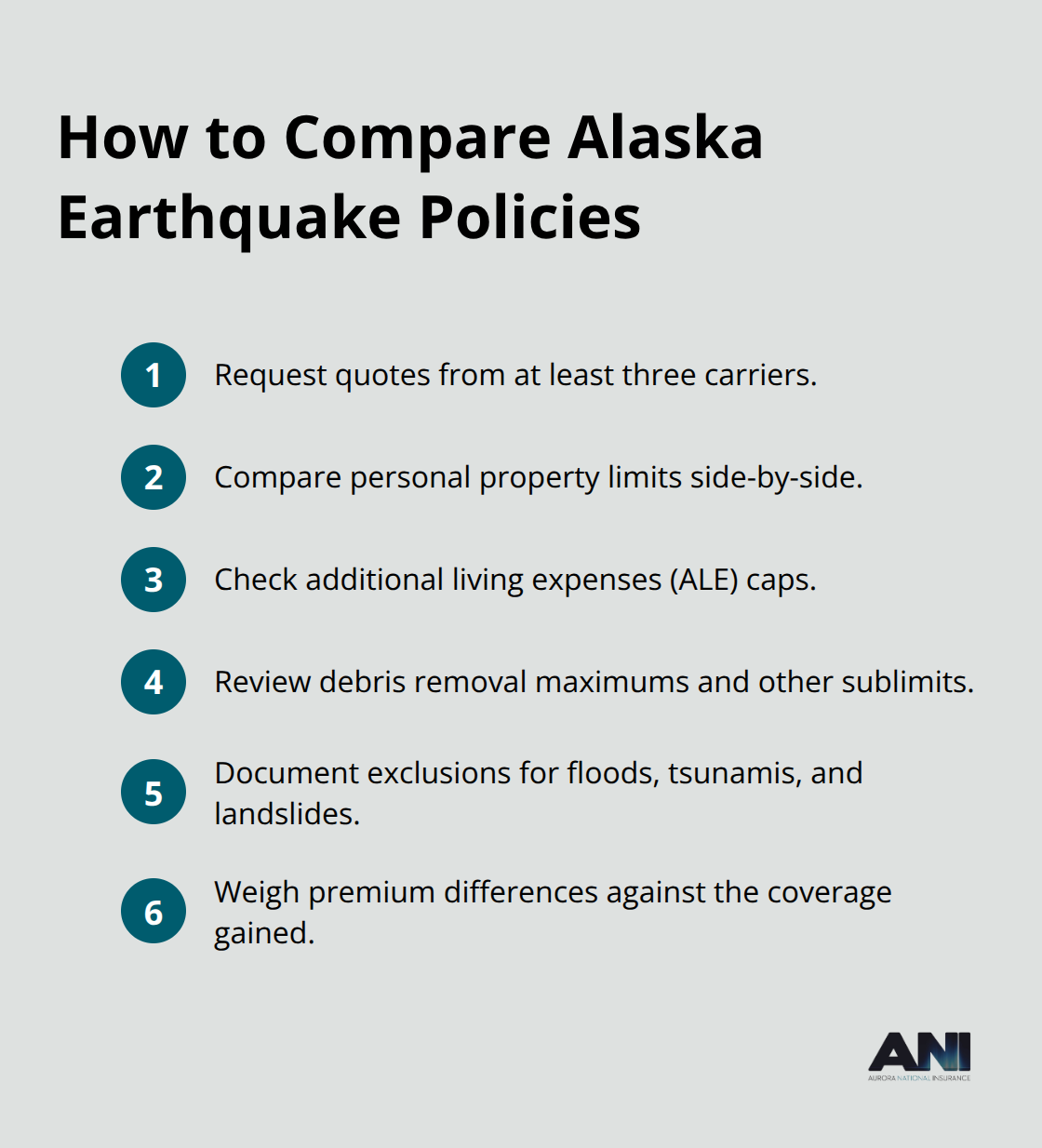

FM Global, Palomar Specialty, Zurich, State Farm, Berkshire Hathaway and Travelers all write earthquake coverage in Alaska with different underwriting standards and premium structures. Request quotes from at least three carriers and compare their coverage for personal property limits, additional living expenses caps, and debris removal maximums, since these sublimits vary substantially between insurers. A policy offering $50,000 in personal property coverage protects far less than one providing $100,000, yet the premium difference may be only 10 to 15 percent. Document each carrier’s specific exclusions regarding floods, tsunamis, and landslides caused by earthquakes, as coverage varies by insurer.

Activate Your Coverage Quickly

Once you select your policy, contact your agent or the carrier directly to activate coverage, which typically takes effect within 24 to 48 hours of payment. This rapid activation gives you immediate protection against the next seismic event in your region. Licensed agents who understand local seismic zones can access quotes from carriers writing in your area and help you navigate the comparison process efficiently.

Final Thoughts

Earthquake home insurance in Alaska protects your financial security when seismic activity strikes your region. Standard homeowners policies leave you completely exposed to ground shaking damage, foundation repairs, debris removal and additional living expenses that can reach hundreds of thousands of dollars. The November 2025 magnitude 6.0 quake near Susitna and the 2018 Anchorage earthquake demonstrated that Alaska’s seismic risk is immediate and real, not theoretical.

Obtaining your property’s exact distance from known fault lines using USGS earthquake hazard maps takes minutes, then requesting quotes from at least three carriers with your home’s age, square footage, foundation type and location details reveals significant price variations. Comparing coverage limits based on actual rebuild costs rather than appraised value and balancing your deductible percentage against premium affordability positions you to select the right protection. Ask each carrier about mitigation discounts for securing water heaters or fastening furniture, which can reduce premiums by 5 to 15 percent.

We at Aurora National Insurance help Alaska homeowners navigate this process with licensed agents who understand local seismic zones and access quotes from multiple top-rated carriers. Contact us today for instant online quotes and responsive service that matches your home’s specific vulnerability and your financial situation. Your next step is requesting quotes from multiple carriers this week, before the next significant earthquake occurs in your region.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.