Alaska Commercial Auto Insurance: Key Considerations for Remote States

Running a business in Alaska means dealing with unique insurance challenges that most of the lower 48 states never face. Remote locations, brutal winters, and limited competition create a complex landscape for Alaska commercial auto insurance.

At Aurora National Insurance, we’ve worked with countless Alaska business owners navigating these obstacles. This guide walks you through the coverage types you actually need and practical ways to reduce your premiums without sacrificing protection.

Alaska’s Remote Landscape Drives Higher Commercial Auto Costs

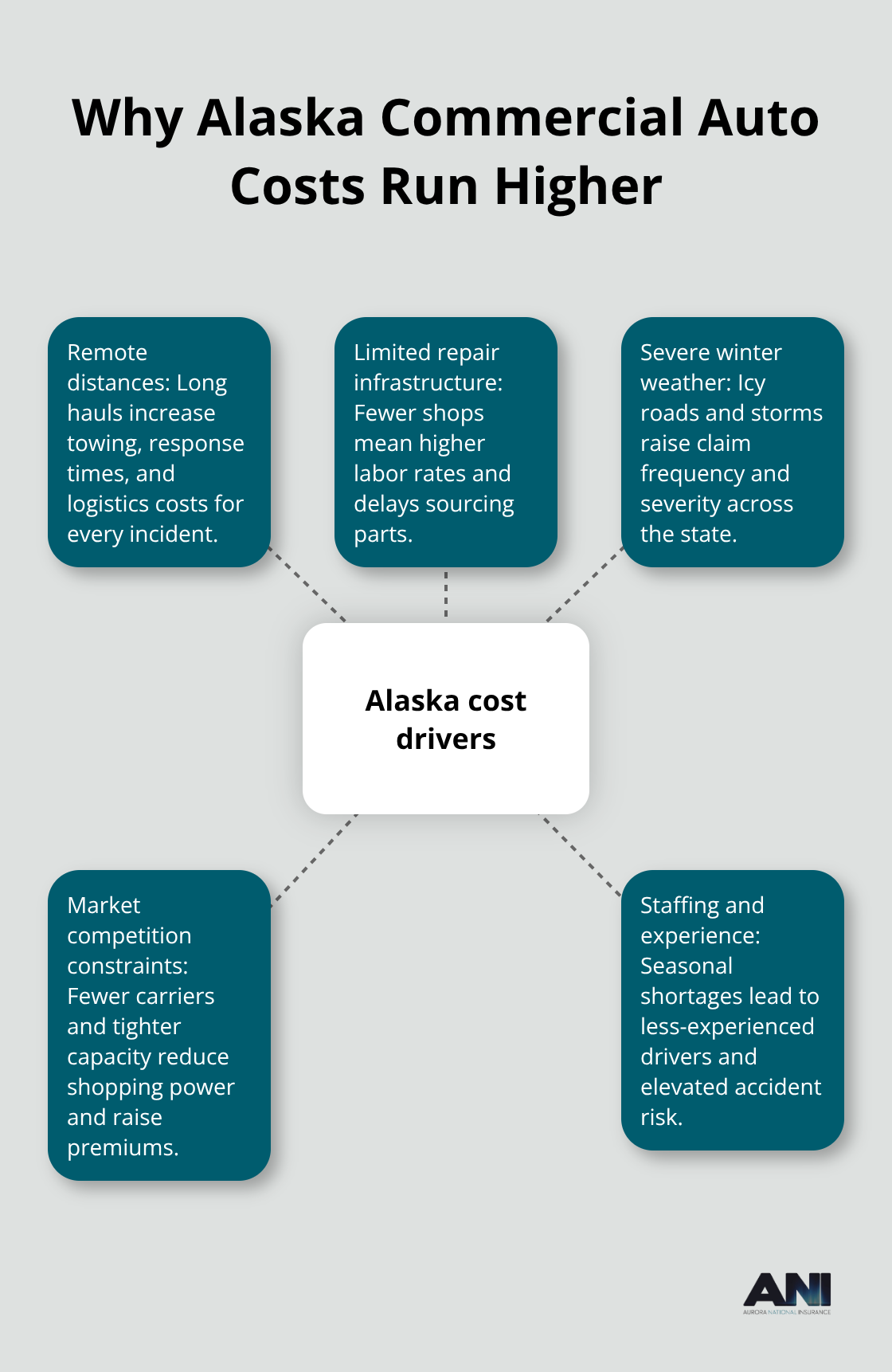

Alaska’s geography creates insurance problems that flat-rate pricing models simply cannot handle. The state’s vast distances between towns, combined with limited repair infrastructure and long response times for emergency services, push claims costs significantly higher than the national average. When a vehicle breaks down 200 miles from Anchorage, the towing and repair expenses multiply quickly-and your insurance premiums reflect this reality. According to industry data, auto insurance rates in Alaska have experienced significant year-over-year changes, with harsh winter conditions and remote roads driving both claim frequency and severity upward. This is not a temporary trend. The structural challenges of Alaska’s environment mean your baseline premiums will always exceed what a comparable business pays in the lower 48 states.

Distance Compounds Every Problem

Remote locations mean fewer repair shops, longer wait times, and higher labor costs. A collision that would cost $3,000 to fix in Seattle might cost $4,500 or more in Fairbanks simply because the shop has limited competition and must account for the cost of importing parts. Winter weather intensifies this problem-icy interior roads and heavy Anchorage traffic create accident conditions that don’t exist in milder climates. Seasonal risks matter too. Fleet staffing shortages across Alaska have forced many businesses to hire less-experienced drivers, and underwriters know this elevates accident risk. Limited competition in the insurance market compounds the problem further. Some carriers have exited Alaska entirely or tightened capacity, leaving fewer options for businesses to shop around. This means your negotiating power is weaker than it would be in states with a dozen major carriers actively competing.

An experienced broker who understands Alaska’s specific risk profile can tell your story to underwriters and navigate carrier preferences to secure better terms than you would find on your own.

Coverage Gaps Created by Alaska’s Unique Conditions

Standard commercial auto policies sometimes miss Alaska-specific exposures. Vehicles operating in remote areas face risks that traditional underwriting models underestimate, and policies written for harsh conditions may not account for seasonal layups or the extended driving distances common here. Electric vehicles bring another complication-their expensive battery components and advanced electronics drive repair costs significantly higher, affecting how carriers price coverage. You need to verify that your policy explicitly covers the types of driving your fleet actually does. If your contractors work seasonally or operate only during certain months, you should use layup credits to reduce premiums during inactive periods. If your vehicles travel into remote regions regularly, that exposure needs to be clearly documented and priced accordingly. Replacement cost values for your vehicles should reflect Alaska inflation, not national averages-underinsuring your fleet leaves you exposed after a loss.

What Coverage Types Actually Protect Your Fleet

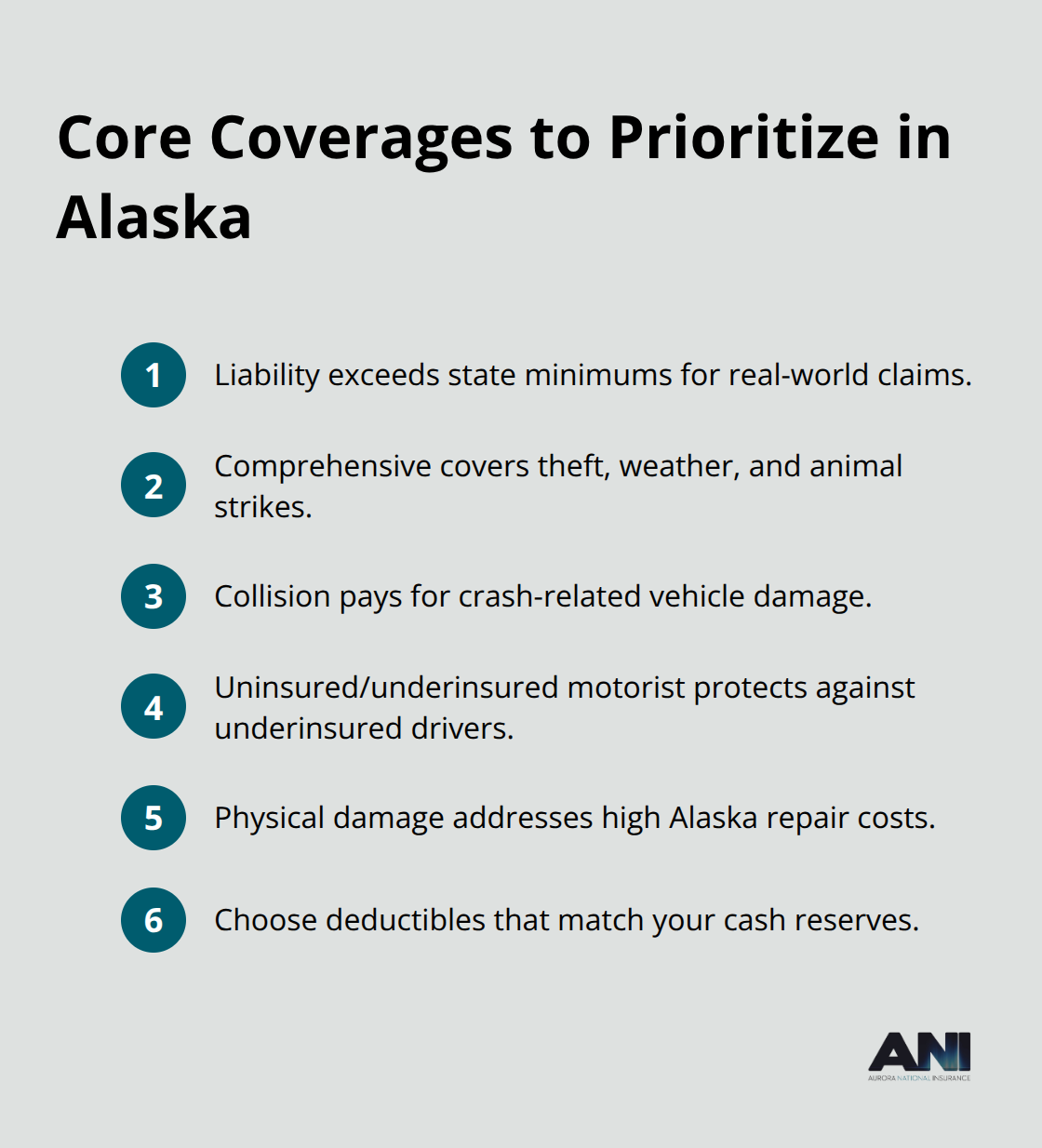

The right coverage mix depends on your specific operations and risk tolerance. Liability coverage protects you when your vehicle causes injury or property damage to others, and Alaska’s minimum limits ($50,000 per person, $100,000 per accident for bodily injury, and $25,000 for property damage) often fall short of real-world claim costs. Comprehensive and collision coverage protect your own vehicles from weather, theft, and accidents-essential in Alaska where winter conditions and remote driving create frequent claims. Uninsured and underinsured motorist coverage protects your drivers when the other party lacks adequate insurance, a real concern on Alaska’s roads. Physical damage coverage addresses the high repair costs that Alaska’s limited infrastructure creates. Each coverage type carries a deductible, and adjusting these amounts can significantly impact your premiums.

Higher deductibles lower your monthly costs but increase what you pay out of pocket after a loss. Lower deductibles cost more upfront but provide better protection when claims happen.

Understanding these coverage options positions you to make informed decisions about what your fleet actually needs, which directly affects both your protection level and your bottom line.

Coverage Types That Protect Your Alaska Fleet

Comprehensive and Collision Protection Address Alaska’s Weather Realities

Comprehensive and collision coverage protect your vehicles from the weather and road conditions that define Alaska driving. Comprehensive covers theft, vandalism, weather damage, and animal strikes-critical in a state where winter storms cause frequent claims and remote locations increase theft risk. Collision covers damage from accidents with other vehicles or objects, and in Alaska’s challenging driving conditions, this protection pays for itself quickly. Alaska’s winter weather and seasonal driving conditions heighten auto risk significantly, pushing premiums higher for fleets that operate year-round.

The question is not whether you need these coverages but what deductible level makes sense for your cash flow. A $1,000 deductible costs less monthly than a $500 deductible, but it also means you absorb more cost after each claim. Most Alaska contractors and service businesses choose $1,000 deductibles to balance affordability with manageable out-of-pocket expenses.

Uninsured and Underinsured Motorist Coverage Fills Critical Gaps

Uninsured and underinsured motorist coverage protects your drivers when another driver causes an accident but lacks sufficient insurance to cover damages. Alaska’s roads include drivers without adequate coverage, and this gap protection prevents your business from absorbing costs that should belong to the at-fault party. Physical damage coverage specifically addresses the high repair expenses that Alaska’s limited infrastructure creates. When your vehicle needs repairs in Fairbanks or remote areas, labor costs and parts availability drive expenses well above national averages.

Liability Limits Matter More Than State Minimums

Commercial general liability rounds out essential protection by covering third-party injury or property damage claims that arise from your business operations-separate from auto-specific incidents. This coverage protects you when a contractor’s equipment damages a client’s property or when a delivery driver injures a pedestrian.

The key decision is matching your coverage limits to your actual exposure rather than defaulting to Alaska’s minimums. The state requires only $50,000 per person and $100,000 per accident for bodily injury liability, but a serious injury claim easily exceeds these limits. Nuclear verdicts and escalating medical costs drive higher auto claim severity across Alaska, meaning underinsuring your fleet leaves you vulnerable to catastrophic out-of-pocket costs. Many Alaska businesses operate with $100,000 per person and $300,000 per accident limits for bodily injury, and $50,000 to $100,000 for property damage-roughly double the state minimums.

Your actual limits should reflect your vehicle types, annual mileage, and driving environments. A snow plow service operating heavy equipment in populated areas needs higher limits than a contractor making occasional local deliveries. An experienced broker can help you stress-test your coverage limits against realistic claim scenarios specific to your operations.

Strategic Bundling and Risk Management Lower Your Premiums

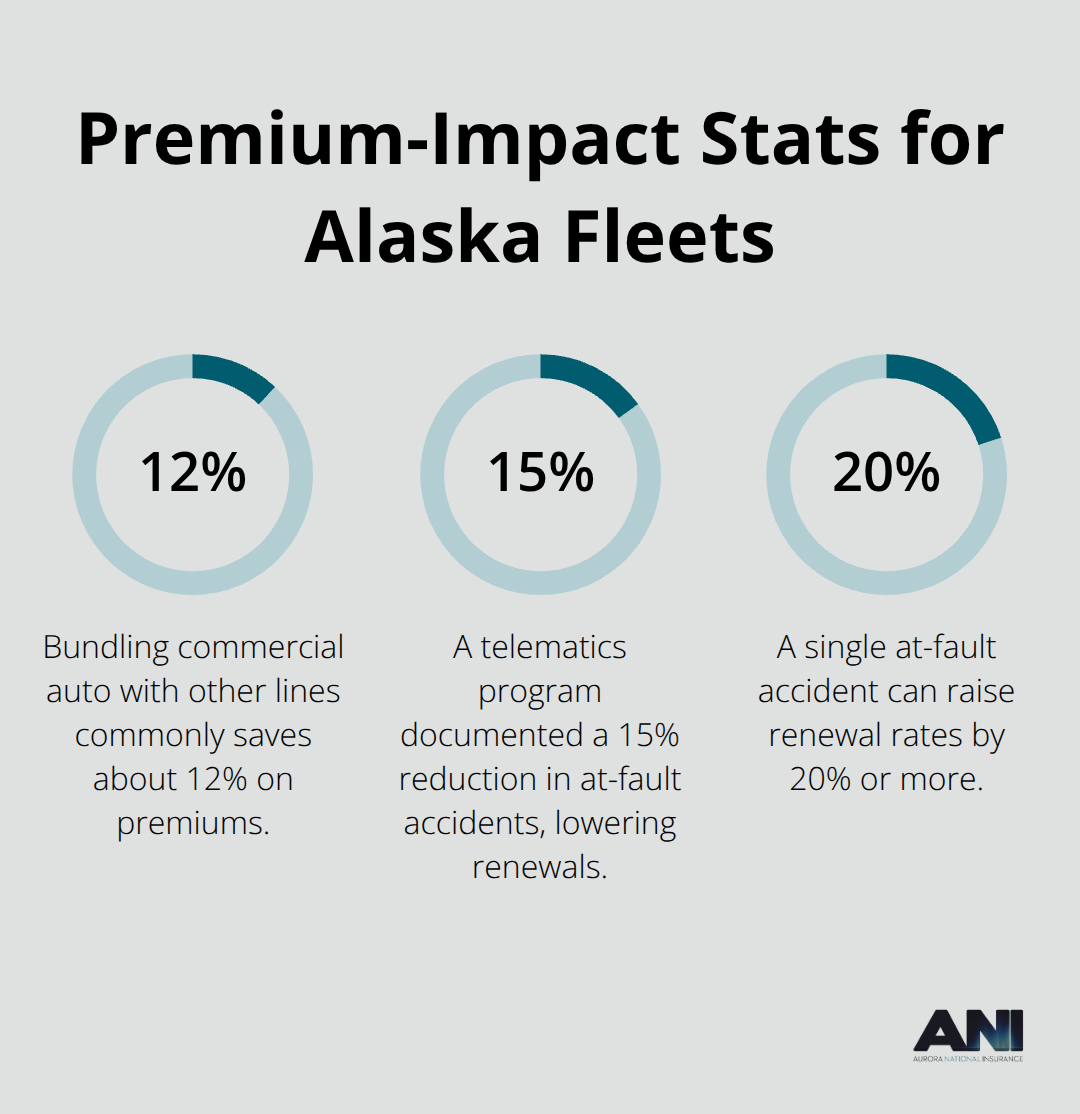

Bundling commercial auto with general liability, property coverage, and other business lines typically yields discounts around 12% or more on auto premiums-meaningful savings when Alaska base rates already run higher than national averages. Some carriers offer additional savings for clean driving records, safety equipment installations, and telematics programs that monitor driver behavior and vehicle performance. These programs reward safer operations with lower rates while providing data you can use to identify training needs and reduce future claims.

The cost of protecting your Alaska fleet reflects genuine risk, not arbitrary pricing. Your focus should shift to strategic coverage choices and risk management rather than chasing the lowest premium. Once you understand what coverage your fleet actually needs, the next step is identifying which carriers offer the best combination of rates, service, and willingness to write Alaska business-a decision that separates businesses that pay too much from those that find real value.

Reduce Premiums Without Sacrificing Protection

Bundle Coverage Lines for Immediate Savings

Combining commercial auto with general liability, commercial property, workers’ compensation, and cyber coverage delivers the most immediate savings available to Alaska fleets. This approach typically yields discounts around 12% or more on your auto premiums according to industry benchmarks. A contractor paying $200 monthly for standalone commercial auto saves roughly $24 per month through bundling policies, and that figure grows when you add property or workers’ comp to the package. Multiple carriers reward bundling more aggressively than others, so shopping multiple options matters significantly. The secondary benefit of bundling extends beyond discounts-consolidating policies with one carrier simplifies renewals, claims reporting, and coverage verification. When you need a certificate of insurance quickly or face a claim, managing one policy instead of three reduces administrative friction and accelerates your response time.

Implement Safety Programs That Carriers Reward

Safety programs and driver training directly influence how underwriters price your fleet, and carriers increasingly offer measurable discounts for documented risk management. Telematics programs that track speed, seatbelt usage, harsh braking, and acceleration patterns can reduce your premiums by rewarding safer operations. Some programs offer real-time feedback to drivers and monthly safety reports that identify training opportunities specific to your fleet. A plumbing company using telematics for two years documented a 15% reduction in at-fault accidents, which translated directly into lower renewal rates. Defensive driving courses for your operators cost $100 to $300 per driver but frequently qualify for 5% to 10% premium discounts that repay the training investment within months. Clean driving records matter enormously in Alaska’s tight underwriting market-a single at-fault accident or moving violation can trigger rate increases of 20% or more at renewal.

Conversely, three years without incidents positions you for preferred pricing when carriers compete for your business.

Adjust Deductibles and Values to Match Your Cash Position

Your deductible structure deserves annual review as your fleet changes and your cash reserves grow. Moving from a $500 to a $1,000 comprehensive deductible typically saves 15% to 20% on that coverage component, and increasing collision deductibles from $1,000 to $1,500 generates similar savings. The math works when you have sufficient reserves to absorb a claim without sacrificing protection. A snow plow service with $50,000 in equipment reserves can safely absorb a $1,500 deductible, while a startup contractor with $5,000 in cash should maintain lower deductibles despite higher premiums. Replacement cost values for your vehicles need annual updates to reflect Alaska inflation rather than national averages. A pickup truck worth $35,000 in Seattle costs $38,000 to $40,000 to replace in Fairbanks due to freight and local market conditions. Underinsuring your fleet by using national values leaves you exposed to significant out-of-pocket costs after a total loss.

Final Thoughts

Alaska commercial auto insurance requires decisions that differ fundamentally from what businesses in the lower 48 states face. Your fleet operates in an environment where distance, weather, and limited infrastructure create genuine cost pressures that shopping alone will not eliminate. What you control is matching your coverage to your actual operations, bundling strategically to capture available discounts, and implementing safety programs that underwriters reward with better rates.

State minimum liability limits leave you dangerously exposed when claim costs regularly exceed national averages, bundling commercial auto with other business lines typically saves 12% or more on premiums while simplifying your administrative burden, and safety programs matter more in Alaska’s tight underwriting market than in states with abundant carrier competition. A single at-fault accident triggers rate increases of 20% or more, while three years without incidents positions you for preferred pricing when carriers actively compete for your business. Local expertise matters in remote markets because underwriters outside Alaska often misunderstand your specific exposures, and a broker rooted in Alaska knows which carriers remain actively writing business and how to position your risk story to secure competitive terms.

Finding competitive Alaska commercial auto insurance quotes starts with connecting with an agency that represents multiple top-rated carriers and understands local conditions. Contact Aurora National Insurance to review your current coverage and identify savings opportunities specific to your fleet, and our licensed agents deliver the local Alaskan expertise that separates competitive pricing from overpriced protection.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.