Alaska Homeowners Coverage Needs: Tailor Your Policy

Alaska homeowners face distinct insurance challenges that differ significantly from the lower 48 states. Extreme cold, earthquakes, and wildfires create coverage gaps that standard policies often miss.

At Aurora National Insurance, we’ve helped countless Alaska homeowners understand their unique coverage needs and build policies that actually protect their homes. This guide walks you through the specific risks in your region and how to structure your coverage accordingly.

Alaska’s True Weather Threats and How to Cover Them

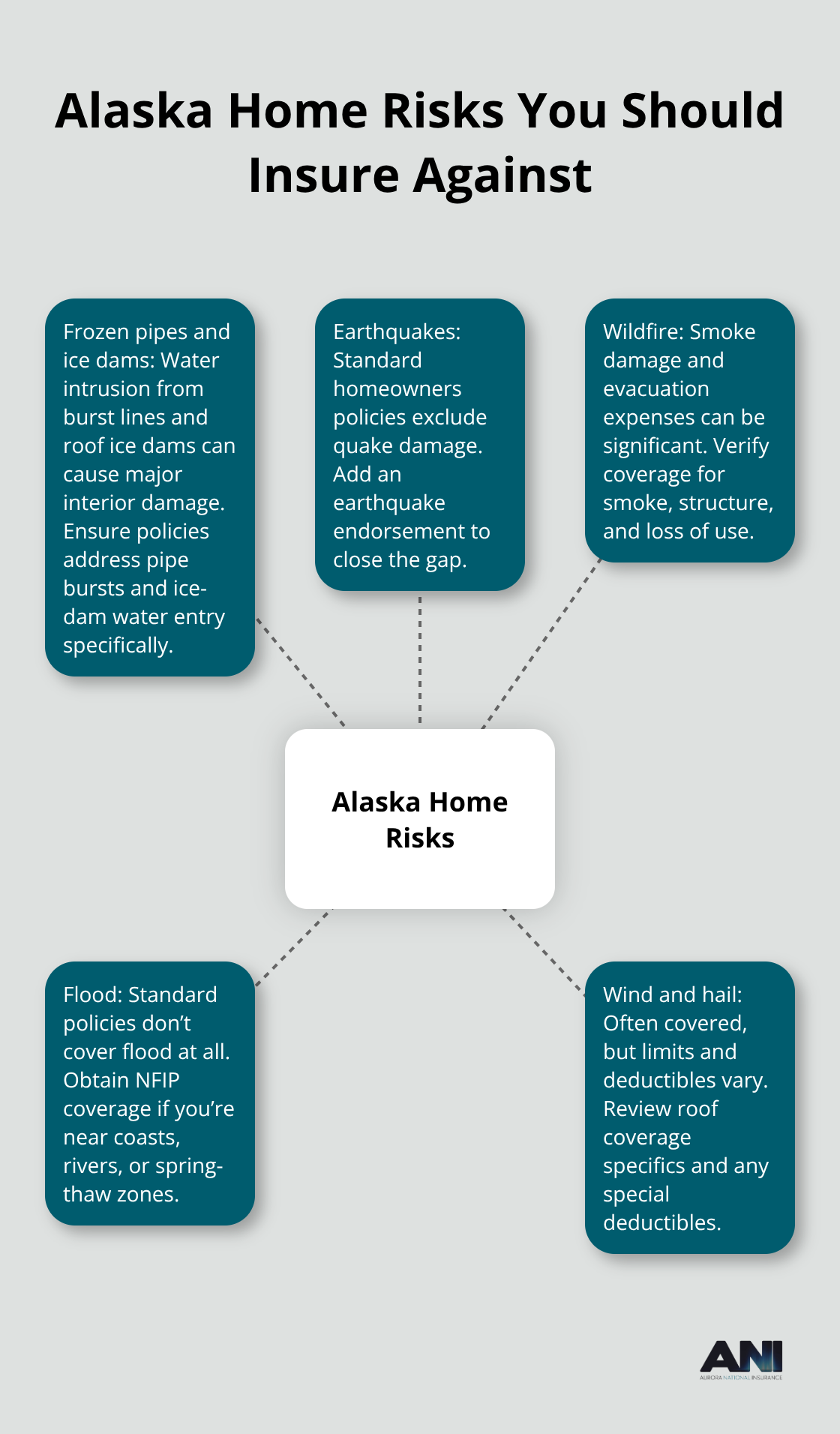

Frozen Pipes and Ice Dam Damage

Frozen pipes represent the most expensive weather-related claim in Alaska. Frozen pipes and ice dam damage coverage typically includes structural damage, personal property damage, and temporary living expenses under standard homeowners policies as long as heat remains on in the home. Ice dams create a separate problem-warm air from your attic melts snow on the roof, which then refreezes at the eaves and forces water back into your home. Proper attic insulation and roof drainage reduce this risk significantly, but your coverage should explicitly address water intrusion from ice dams. Standard policies usually cover wind and hail damage to your roof, though you need to review your specific policy limits and any deductibles that apply.

Underestimating Replacement Costs

The real problem we see with Alaska homeowners is underestimating replacement costs when damage occurs. Rebuild costs in Alaska run substantially higher than the national average due to remote locations and limited contractor availability, so your dwelling coverage should reflect actual rebuilding expenses, not outdated valuations. Most homeowners fail to account for these regional cost differences when they select their coverage limits, leaving themselves exposed to significant out-of-pocket expenses after a loss.

Earthquake Coverage Gaps

Earthquakes present a coverage gap that most Alaska homeowners ignore entirely, even though seismic activity is a genuine risk in parts of the state. Standard homeowners policies exclude earthquake damage, which means you must add an earthquake endorsement if you want protection-this is not optional coverage you can assume is included. The cost of adding this endorsement is modest compared to the potential damage from a significant seismic event.

Wildfire and Flood Risks

Wildfire risk varies dramatically by location in Alaska, but if you live in or near a wildfire-prone area, smoke damage and evacuation costs become real concerns. Flood damage sits outside standard homeowners coverage regardless of how water enters your home, making flood insurance through the National Flood Insurance Program a necessity rather than an option if you live near coastal areas, rivers, or zones prone to spring thaw flooding. The Alaska Division of Insurance recommends assessing your specific location’s flood risk even if you’re not in a mapped high-risk zone, because rapid snow melt and heavy precipitation can create flooding outside traditional floodplain maps. Your mortgage lender will likely require flood insurance if your home sits in or near a floodplain, but even without a lender requirement, the cost of flood damage far exceeds the annual premium for protection.

Understanding these weather-specific threats shapes how you should structure your dwelling protection and personal property coverage-the next critical components of an Alaska homeowners policy.

Building Dwelling Coverage That Matches Alaska Rebuild Costs

Your dwelling coverage limit determines how much your insurer will pay to rebuild your home after a total loss, and this is where most Alaska homeowners make their first critical mistake. Standard replacement cost value policies reimburse you for rebuilding with materials of similar kind and quality, but the 80% rule that applies nationally becomes dangerous in Alaska. This guideline suggests insuring your home for at least 80% of its replacement cost to avoid penalties, yet Alaska rebuild costs run 30 to 40 percent higher than the national average due to remote locations, limited contractor availability, and transportation expenses for materials. If you base your dwelling limit on an outdated home valuation or use national cost estimates, you will face substantial out-of-pocket expenses after a claim. We recommend obtaining a current replacement cost estimate from a local Alaska contractor before selecting your dwelling coverage limit, not relying on online calculators or old appraisals. Your policy should explicitly state replacement cost value rather than actual cash value, which only reimburses depreciated amounts and leaves you severely underprotected.

Personal Property Coverage for Alaska’s Remote Challenges

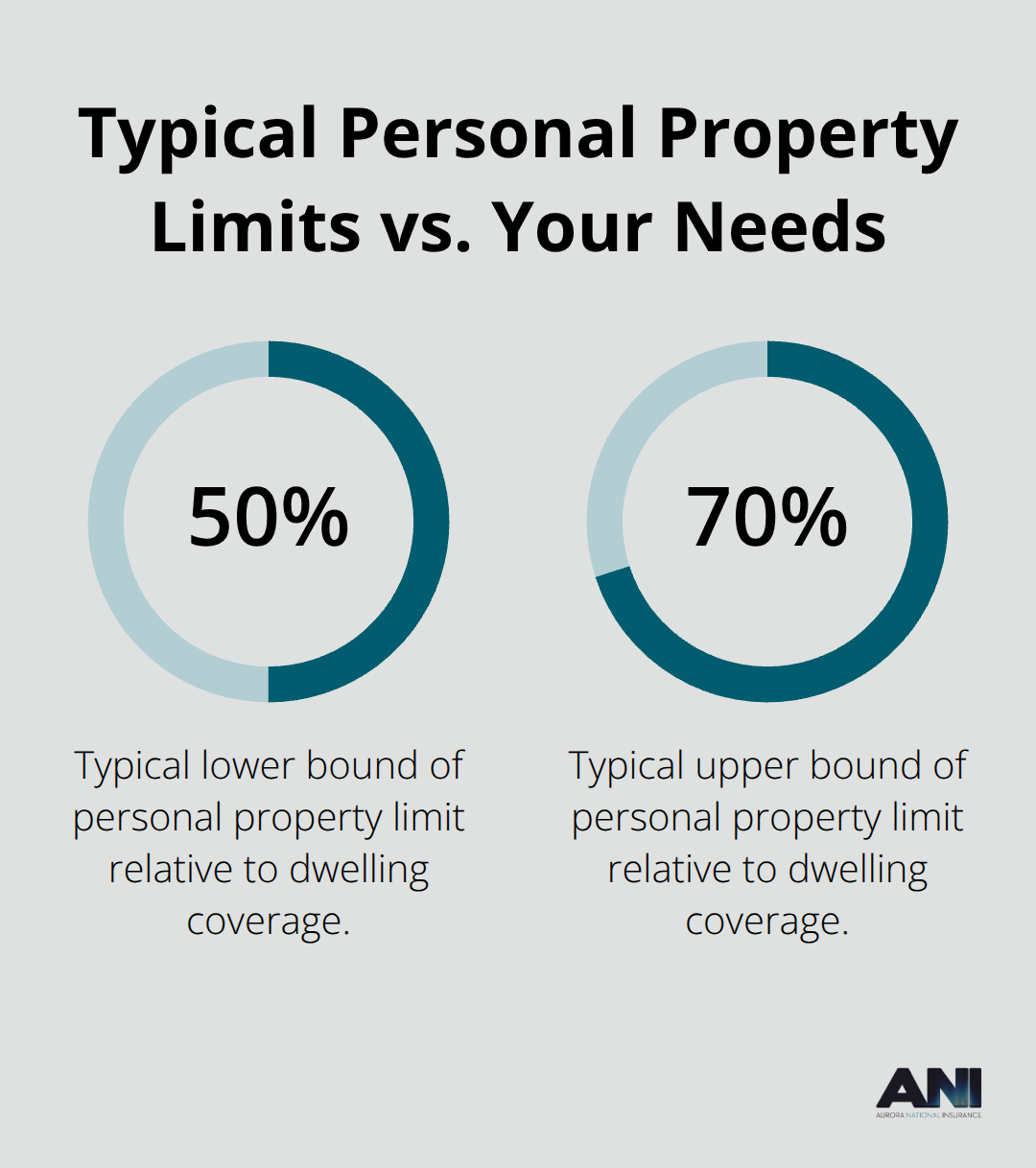

Personal property coverage protects your belongings inside the home, but remote Alaska locations create specific complications. Standard personal property limits typically cover 50 to 70 percent of your dwelling coverage amount, which proves inadequate for most households, so you should increase this limit to match your actual inventory value.

High-value items like jewelry, firearms, electronics, or collectibles require scheduled personal property endorsements to receive full replacement cost protection, since standard policies impose sub-limits on these categories that leave you significantly exposed. Alaska’s distance from major retailers means replacement costs for specialized equipment or imported goods often exceed lower 48 prices, making comprehensive personal property coverage essential rather than optional. Create a detailed home inventory documenting everything you own with photographs and receipts, then compare that total to your proposed personal property limit to identify gaps before a loss occurs.

Liability Protection When Help is Far Away

Liability coverage protects you if someone is injured on your property or you accidentally damage someone else’s property, and Alaska’s sparsely populated areas create unique considerations. Standard liability limits of 100,000 to 300,000 dollars often prove insufficient given Alaska’s higher medical costs and limited emergency services access, which can complicate injury cases and increase settlement amounts. Try liability limits of at least 300,000 dollars for most Alaska homeowners, with 500,000 dollars preferable if you have significant assets or frequently host guests. Umbrella insurance policies provide additional liability protection beyond your homeowners policy limits at modest cost, typically 150 to 300 dollars annually for one million dollars of extra coverage. If you rent out a portion of your home or operate any business from your property, your standard homeowners liability becomes insufficient and you need to discuss commercial liability endorsements with your agent before a problem occurs.

Additional Living Expenses and Loss of Use

Additional living expenses coverage pays for temporary housing, meals, and other essentials if a covered loss makes your home uninhabitable. This coverage becomes particularly important in Alaska, where finding temporary rental housing in remote areas can prove difficult and expensive. Your policy should include adequate additional living expenses limits to cover several months of temporary housing costs, not just a few weeks. Standard policies typically limit this coverage to 20 to 30 percent of your dwelling limit, which often falls short in Alaska’s high-cost rental markets. Review your specific policy limits and verify coverage details match your needs to ensure adequate protection.

Tailoring Coverage to Your Specific Location

Alaska’s geography means your coverage needs vary dramatically based on where you live. Coastal homeowners face different flood and storm surge risks than interior residents, while those near wildfire zones need different protection than those in urban areas. Your agent should help you assess location-specific hazards and adjust your coverage accordingly, rather than applying a one-size-fits-all approach. The cost-saving strategies available to you also depend on your location and home characteristics, which makes working with someone familiar with Alaska’s regional differences essential as you move forward with finalizing your policy structure.

Cost-Saving Strategies for Alaska Home Insurance

Reducing your Alaska home insurance premium requires a strategic approach that goes beyond shopping around for quotes. Most Alaska homeowners leave significant savings on the table because they don’t understand which discounts actually apply to their situation or they fail to take the actions that trigger those savings.

Bundle Your Policies for Maximum Savings

The most effective strategy is combining your homeowners policy with auto insurance, which can save customers over $950 per year. If you’re not currently combined, getting quotes for both policies together should be your first step, since this single action produces the largest discount most people qualify for. This isn’t theoretical savings-insurers reduce your rates because bundled customers represent lower administrative costs and reduced risk across multiple policies.

Install Security and Safety Devices

A security system, burglar alarm, or fire alarm qualifies you for home security discounts that reduce your annual premium by 5 to 15 percent depending on your carrier. These devices directly reduce your insurer’s risk of loss, so they compensate you accordingly. The cost of installation typically pays for itself within two to three years through premium reductions alone.

Invest in Home Improvements That Lower Premiums

A new roof can qualify you for a roof discount that lowers premiums for the next 15 to 20 years, making this renovation particularly cost-effective from an insurance perspective. Newer homes and recently renovated homes also qualify for new construction discounts, so if you’ve recently completed major upgrades, contact your agent to ensure your policy reflects these improvements and the discounts they trigger.

Review and Adjust Coverage Annually

Your policy needs change as your home ages, your assets grow, and Alaska’s construction costs rise. Reviewing your coverage annually and adjusting limits based on actual Alaska rebuild costs rather than national averages prevents both overpaying for coverage you don’t need and underpaying with catastrophic gaps. Obtaining updated replacement cost estimates from local Alaska contractors every three to five years keeps your dwelling limit accurate. Increasing your deductible from $500 to $1,000 or $1,500 can reduce your annual premium by 10 to 25 percent, but this strategy only works if you have cash reserves to cover the higher out-of-pocket cost after a loss.

Maintain a Clean Claims History

Claims-free discounts reward you for maintaining a clean claims history, so avoiding small claims and only filing for significant losses protects your premium long-term. If you’ve gone several years without filing a claim, ask your agent whether you qualify for loyalty or claims-free discounts that should be reflected in your renewal quote. Treating your annual renewal as an opportunity to reassess your entire coverage structure rather than simply accepting a renewed quote produces both better protection and lower costs.

Final Thoughts

Alaska homeowners coverage needs differ fundamentally from those in the lower 48 states, and standard policies leave you exposed to significant financial risk. Frozen pipes, earthquakes, wildfires, and floods require deliberate coverage decisions that account for Alaska’s unique geography and climate. Your dwelling limit must reflect actual Alaska rebuild costs, your personal property coverage must match your real inventory value, and your liability limits must account for Alaska’s higher medical costs and limited emergency services.

A local insurance agent who understands Alaska’s regional differences makes the difference between a policy that sounds good and one that actually protects you. An agent familiar with your specific area identifies which coverage gaps matter most, recommends endorsements that fill the gaps standard policies leave open, and structures your policy to balance protection with cost. Working with someone who knows Alaska’s challenges prevents you from overlooking location-specific hazards that could leave you underprotected.

Start by getting a personalized quote that reflects your actual Alaska rebuild costs, location-specific hazards, and coverage priorities. Our licensed agents represent multiple top-rated carriers and can compare options to find the right protection at competitive prices. Contact us to discuss your specific situation and finalize a policy that gives you genuine peace of mind.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.