Portland Fleet Auto Insurance: Streamlined Coverage for Your Vehicles

Running multiple vehicles for your Portland business means managing separate insurance policies, tracking different coverage limits, and juggling renewal dates. Portland fleet auto insurance consolidates all of this into one manageable policy that protects your entire operation.

At Aurora National Insurance, we’ve helped Portland businesses cut through the complexity of vehicle coverage. A single fleet policy saves time, reduces administrative headaches, and often costs less than insuring each vehicle separately.

What Your Fleet Policy Actually Covers

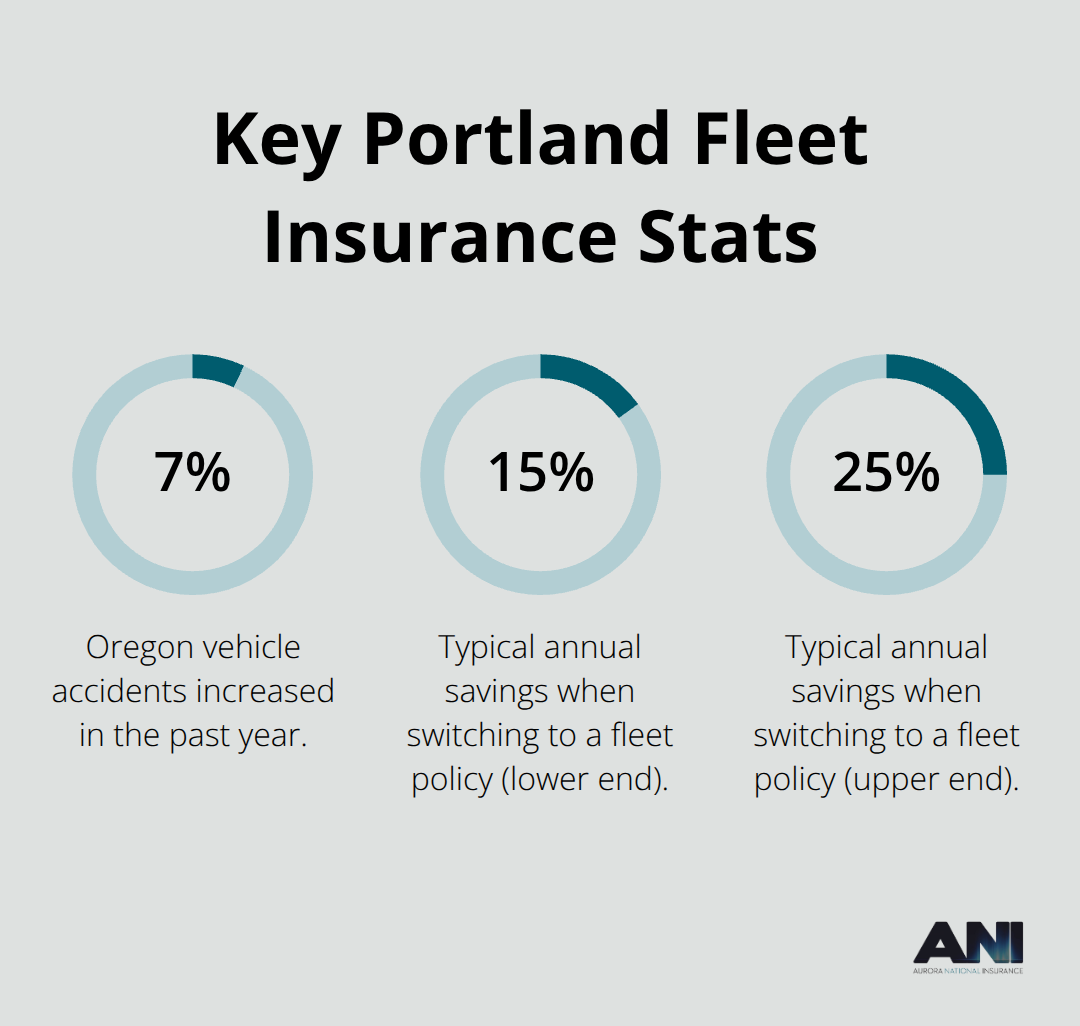

Fleet auto insurance protects your vehicles and drivers across multiple coverage types that work together to handle accidents, damage, and liability claims. The Bureau of Transportation Statistics reported over 11 million fleet vehicles in service as of 2013, and Oregon saw a 7% increase in vehicle accidents in the past year, making comprehensive coverage essential for Portland operations. A single fleet policy typically covers owned vehicles, leased vehicles, and sometimes non-owned vehicles used for business purposes, all under one agreement. This means any employee can drive any vehicle in your fleet unless you specifically exclude them, which eliminates coverage gaps that arise when you manage separate policies for each vehicle.

Collision and Comprehensive Protection

Collision coverage handles damage from accidents with other vehicles or objects, while comprehensive coverage protects against theft, vandalism, weather damage, and other non-collision events. The average cost per fleet incident exceeds $20,000, so skipping either type leaves your business vulnerable to substantial out-of-pocket losses. When you consolidate multiple vehicles into one fleet policy, insurers typically apply the same deductible across all vehicles, which simplifies claims processing and repair coordination. Portland’s diverse terrain, harsh winters, and heavy traffic congestion increase the odds of vehicle damage, making comprehensive coverage particularly valuable for fleets operating in the area. You should review whether your policy covers both owned and leased vehicles, since many fleets use a mix of both and need clarity on what happens if a leased vehicle is damaged.

Liability Protection Across Your Fleet

Liability coverage in a fleet policy protects your business when a driver causes injury or property damage to someone else. Oregon requires minimum liability insurance for fleets, with a minimum acceptable amount of $750,000 per accident for auto liability combined single limit. A well-structured fleet policy provides blanket coverage for all drivers and vehicles, meaning you don’t need to add individual drivers or worry about coverage lapses when staff turnover occurs. This approach proves especially valuable for industries with high driver turnover, such as delivery services and construction, where managing separate policies for each new hire becomes administratively costly. Portland businesses benefit from faster claims processing and repair coordination when all vehicles operate under one policy, which reduces downtime and keeps operations moving.

Choosing Coverage Limits That Match Your Risk

The next step involves assessing what coverage limits actually protect your business from financial loss. Most Portland fleets operate in environments where accidents happen more frequently due to congestion and weather, so your limits should reflect that reality rather than simply meeting state minimums.

Why Fleet Insurance Saves Portland Businesses Real Money

Consolidating your vehicles into a single fleet policy costs significantly less than insuring each vehicle separately, and the savings compound as your fleet grows. When you manage five or ten individual policies, you pay separate administrative fees, process multiple renewals, and miss volume discounts that insurers reserve for fleet customers. Portland businesses reduce their total annual insurance costs by 15 to 25 percent when they switch from individual vehicle policies to a fleet arrangement. The math works because insurers price fleet policies based on your overall claims history and risk profile across all vehicles, rather than penalizing you for isolated incidents on one vehicle. If one vehicle has a minor collision, your fleet premium adjusts based on the combined safety record of all vehicles, not just that one incident.

How Fleet Policies Eliminate Redundant Costs

You avoid redundant coverage that comes from managing separate policies, where overlapping liability limits and duplicate administrative costs inflate your total spend. Beyond premium reductions, fleet policies eliminate the headache of tracking different renewal dates, managing separate deductibles for each vehicle, and coordinating claims across multiple insurers. Portland construction companies, delivery services, and government agencies that operate fleets of 3 or more vehicles see the largest savings, particularly when they consolidate both owned and leased vehicles into one agreement.

Streamlined Administration Reduces Staff Time and Risk

A single fleet policy means one renewal date instead of five or ten, one deductible to track instead of multiple amounts, and one insurer to contact when claims occur. Streamlined administration directly reduces the time your staff spends on insurance management and dramatically lowers the risk of coverage gaps that could leave your business exposed. When an employee causes damage or an accident happens, you file one claim under your fleet policy instead of contacting separate insurers and managing different claim timelines.

Portland businesses with high employee turnover benefit most from this approach since blanket driver coverage means new hires are automatically protected without requiring policy amendments or endorsements for each person. The administrative simplification also reduces the likelihood that a renewal notice gets overlooked or that a policy lapses during the gap between employment dates.

Faster Claims Resolution Keeps Operations Moving

If a vehicle is damaged and needs repairs, a streamlined fleet policy typically processes the claim faster because one insurer coordinates the entire process rather than requiring communication between multiple carriers. This faster claims resolution keeps your vehicles in service sooner and minimizes operational downtime that directly affects revenue. For Portland fleets operating in congested urban areas where vehicle incidents happen more frequently, this efficiency translates into crews staying productive and deliveries staying on schedule.

The next step involves selecting a policy that matches your specific fleet composition and operational risks.

Selecting Coverage That Fits Your Fleet’s Real Needs

Start with a complete inventory of every vehicle your business operates, including owned trucks, leased equipment, and any personally-owned vehicles employees use for work. Next to each vehicle, note its age, value, and primary use-whether it’s local delivery, long-haul transport, or construction site work. This inventory determines which coverage limits actually protect your business rather than simply meeting Oregon’s minimum requirements.

Understanding Liability Limits That Actually Protect You

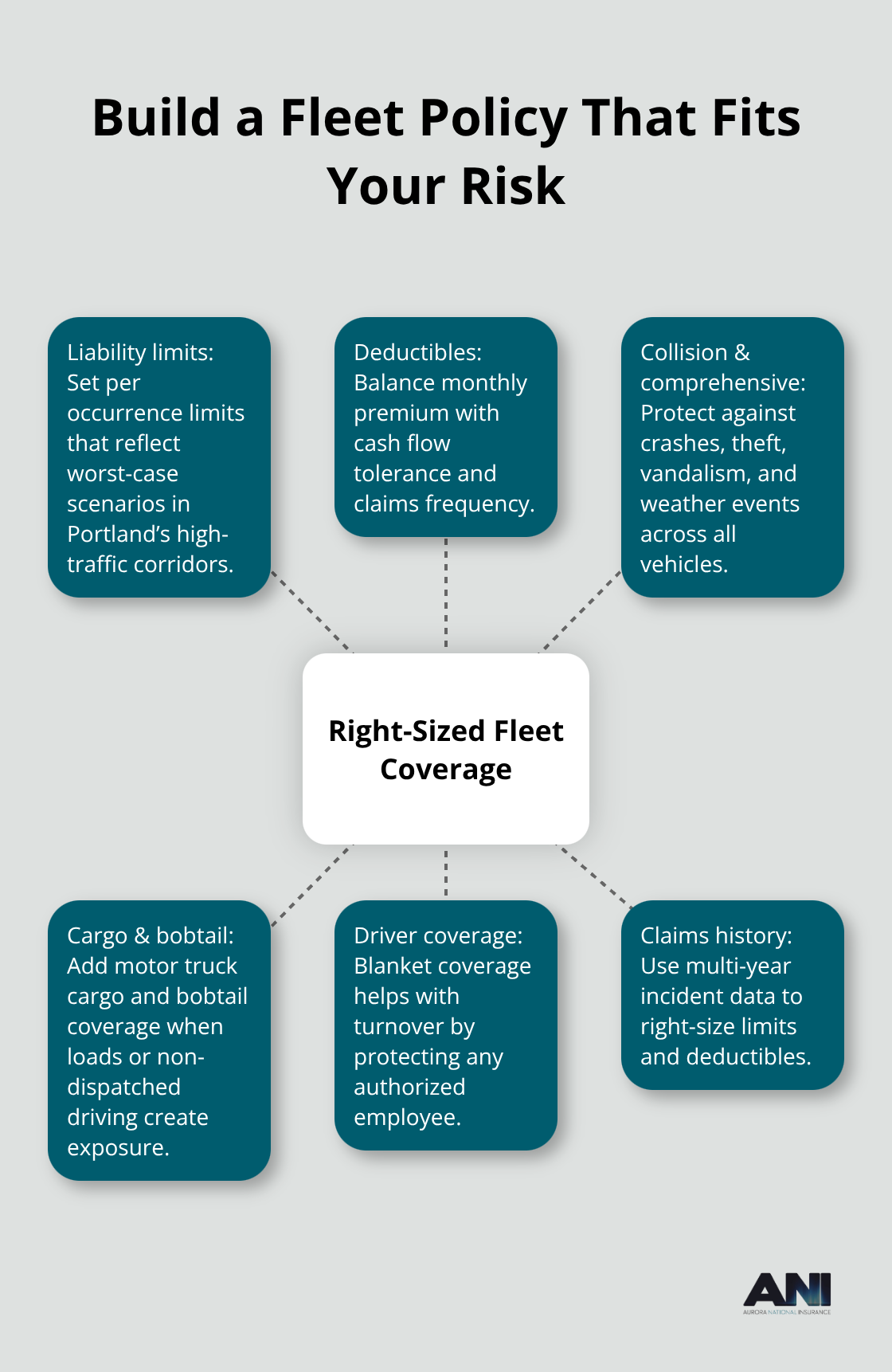

Oregon requires a minimum of $50,000 per person for death and injury, $100,000 per incident for auto liability, but that floor often leaves Portland fleets dangerously underprotected, especially if your vehicles carry valuable cargo or operate in high-traffic areas where liability claims exceed state minimums. Construction fleets transporting equipment, delivery services handling time-sensitive shipments, and government agencies managing public-facing operations should carry liability limits of $1,000,000 or higher per occurrence. The average cost per fleet incident exceeds $20,000, and a single serious accident involving multiple vehicles or pedestrians can generate claims well above state minimums.

Set your liability limit based on your worst-case scenario, not the legal minimum. If your fleet operates in Portland’s congested corridors, assume accidents will be more frequent and potentially more costly than in rural areas. Compare quotes from multiple carriers to see how limits affect your premium-often a jump from higher limits costs far less than the additional protection is worth.

Choosing Deductibles That Match Your Safety Record

Deductibles directly impact both your premium and out-of-pocket costs when claims happen. A $1,000 deductible per vehicle across a five-vehicle fleet means you absorb $5,000 in repairs before insurance covers anything, while a $500 deductible costs more monthly but reduces your financial exposure. Portland businesses with strong safety records and minimal claims history can afford higher deductibles to keep premiums low, while fleets with newer, less experienced drivers benefit from lower deductibles since accidents are more likely.

Review your claims history over the past three years-if your fleet averaged one or fewer incidents annually, higher deductibles make financial sense. If incidents occur frequently, lower deductibles protect cash flow despite higher premiums.

Evaluating Add-On Coverage for Your Specific Operations

Add-on coverage options like comprehensive and collision protection vary significantly in cost and necessity depending on your vehicle fleet composition. A fleet of newer vehicles worth $50,000 or more each warrants comprehensive and collision coverage, while older vehicles nearing end-of-life may justify collision-only or even dropping comprehensive entirely.

Motor truck cargo insurance protects goods in transit if your fleet carries valuable shipments, and this coverage becomes essential for delivery services, construction material transport, or any operation where cargo value exceeds $10,000 per load. Bobtail insurance covers owner-operators when their truck operates without a load or isn’t dispatched for work, protecting against liability exposure during personal use or maintenance runs. Workers’ compensation coverage is mandatory if you have employees, and this coverage prevents individual drivers from bearing medical costs after work-related injuries.

Request policy reviews from multiple carriers-independent brokers can often identify coverage gaps and unnecessary add-ons that inflate your premium without adding real protection.

Final Thoughts

Portland fleet auto insurance consolidates your vehicle coverage into one manageable policy that protects your business, reduces administrative burden, and costs significantly less than managing separate policies for each vehicle. The financial benefits are real-Portland businesses typically save 15 to 25 percent annually when they switch to fleet coverage, and those savings grow as your fleet expands. Beyond cost reduction, a single fleet policy eliminates the risk of coverage gaps that arise when renewal dates slip through the cracks or new employees start without proper protection.

The right Portland fleet auto insurance policy matches your specific vehicle composition, operational risks, and financial tolerance for deductibles. Start by inventorying every vehicle your business operates, then assess whether your current coverage limits actually protect you from worst-case scenarios rather than simply meeting Oregon’s legal minimums. Compare quotes from multiple carriers to identify which add-on coverages genuinely reduce your risk and which ones inflate your premium without adding real value.

We at Aurora National Insurance help Portland fleets find the right coverage at competitive prices through tailored comparisons and expert consultation. Contact us at Aurora National Insurance to get a quote and discover how consolidating your vehicle coverage can simplify operations and protect your bottom line.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.