Oregon Commercial Auto Quotes: Compare Top Auto Coverage

Running a business in Oregon means protecting more than just your vehicles-you’re protecting your employees, your reputation, and your bottom line. Commercial auto insurance works differently than personal coverage, with higher limits and specialized protections that standard policies simply don’t offer.

At Aurora National Insurance, we help business owners find Oregon commercial auto quotes that actually match their risk. The right policy can mean the difference between a manageable claim and a financial crisis for your company.

Why Commercial Auto Coverage Costs More Than Personal Policies

Oregon law requires minimum liability coverage of 25/50/20 for personal vehicles, but commercial auto policies operate under completely different rules. Business owners often face a harsh reality: their personal auto policy excludes any claim related to business use-even a single delivery or client visit can void coverage. Commercial policies aren’t just personal coverage with higher numbers; they’re built to handle the realities of business operations.

Oregon requires commercial vehicles to carry the same 25/50/20 minimum, but that’s genuinely inadequate for most businesses. A single lawsuit from a serious accident can easily exceed $100,000, and if you operate without proper coverage, your personal assets become vulnerable. Most businesses should evaluate whether higher limits like 100/300/100 make financial sense for their operation. Progressive often offers these elevated limits for only modestly more than minimum coverage.

Vehicle-Specific Coverage Protects Your Business Assets

Commercial policies protect the tools, equipment, and materials permanently attached to your vehicles. If you operate a construction truck with mounted equipment or a delivery vehicle with expensive tools, standard collision and comprehensive coverage won’t protect those assets. You should explicitly list any expensive attachments with your insurer, as unattached items like generators or toolboxes fall outside standard coverage.

Hired and Non-Owned Vehicle Coverage Fills a Critical Gap

Hired and non-owned vehicle coverage becomes critical if your employees drive personal vehicles for work tasks. Without this coverage, you face significant liability if an employee’s personal vehicle is involved in a work-related accident.

This coverage protects you against medical costs and legal fees but doesn’t cover damage to the employee’s personal vehicle itself. The distinction matters because your business bears the financial risk even though you don’t own the vehicle.

Employee Safety and Driver Verification

Commercial policies let you list multiple drivers, and you should verify that anyone operating company vehicles has a clean driving record and proper training. Your business bears liability for their actions on the road, which means a single employee with a poor driving history can substantially increase your premiums and expose your company to significant claims. Proper driver vetting and training programs reduce both your insurance costs and your actual accident risk on Oregon roads.

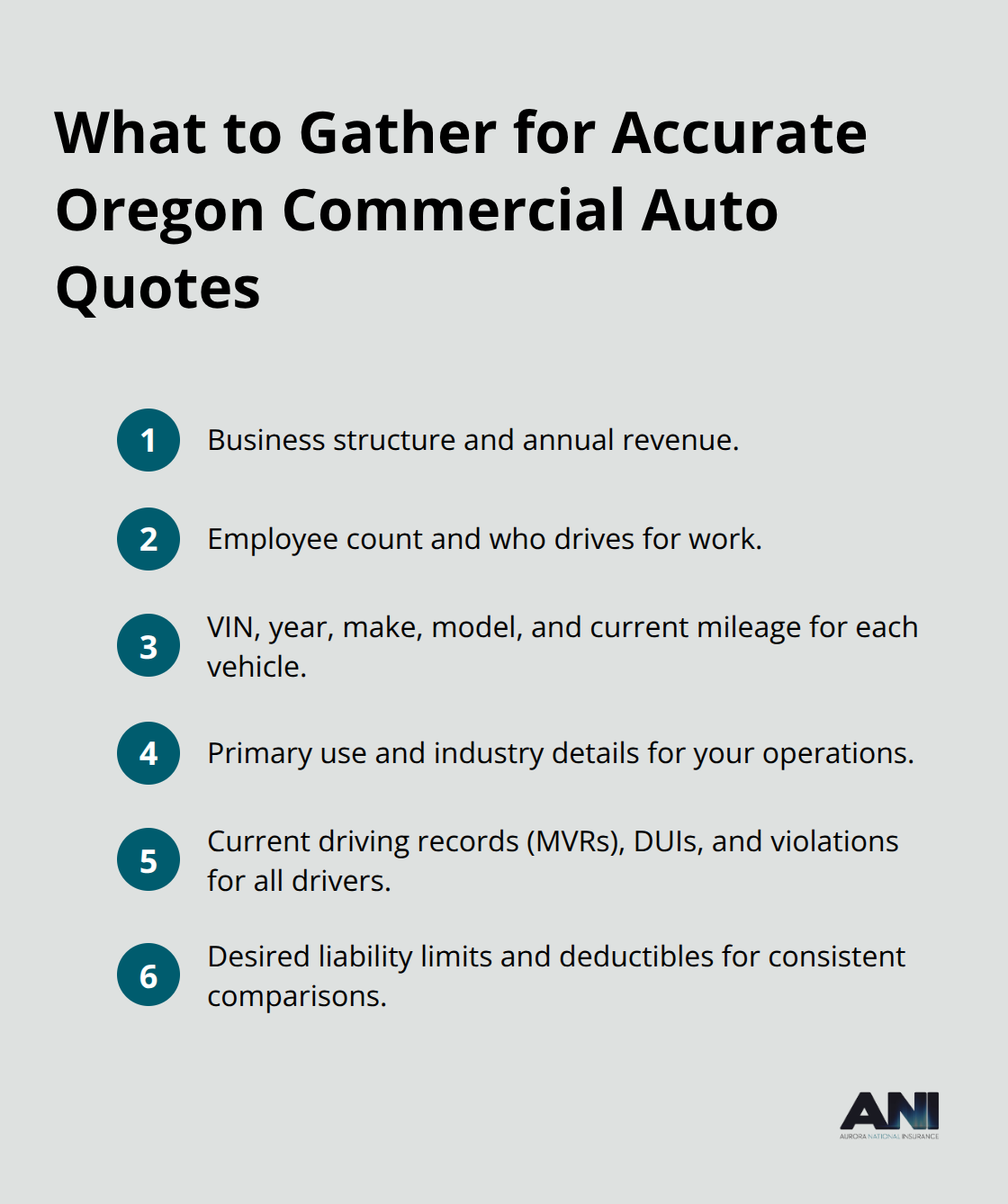

Getting Oregon Commercial Auto Quotes Without Wasting Time

Collecting accurate information upfront saves hours later and prevents quote rejections that force you to start over. You need your business structure, annual revenue, number of employees, and the specific vehicles you want to insure, including the Vehicle Identification Number, year, make, model, and current mileage for each. Most carriers also ask about your industry and primary use-whether you’re doing deliveries, construction, client transport, or something else entirely.

Have your current driving records ready for any employees who operate company vehicles, since a driver with a DUI or multiple violations can spike your rates substantially or even disqualify your company from certain carriers. Oregon’s average commercial auto insurance costs about $184 per month, but your actual premium depends heavily on these specific details, so vague information leads to inaccurate quotes that don’t reflect your real costs.

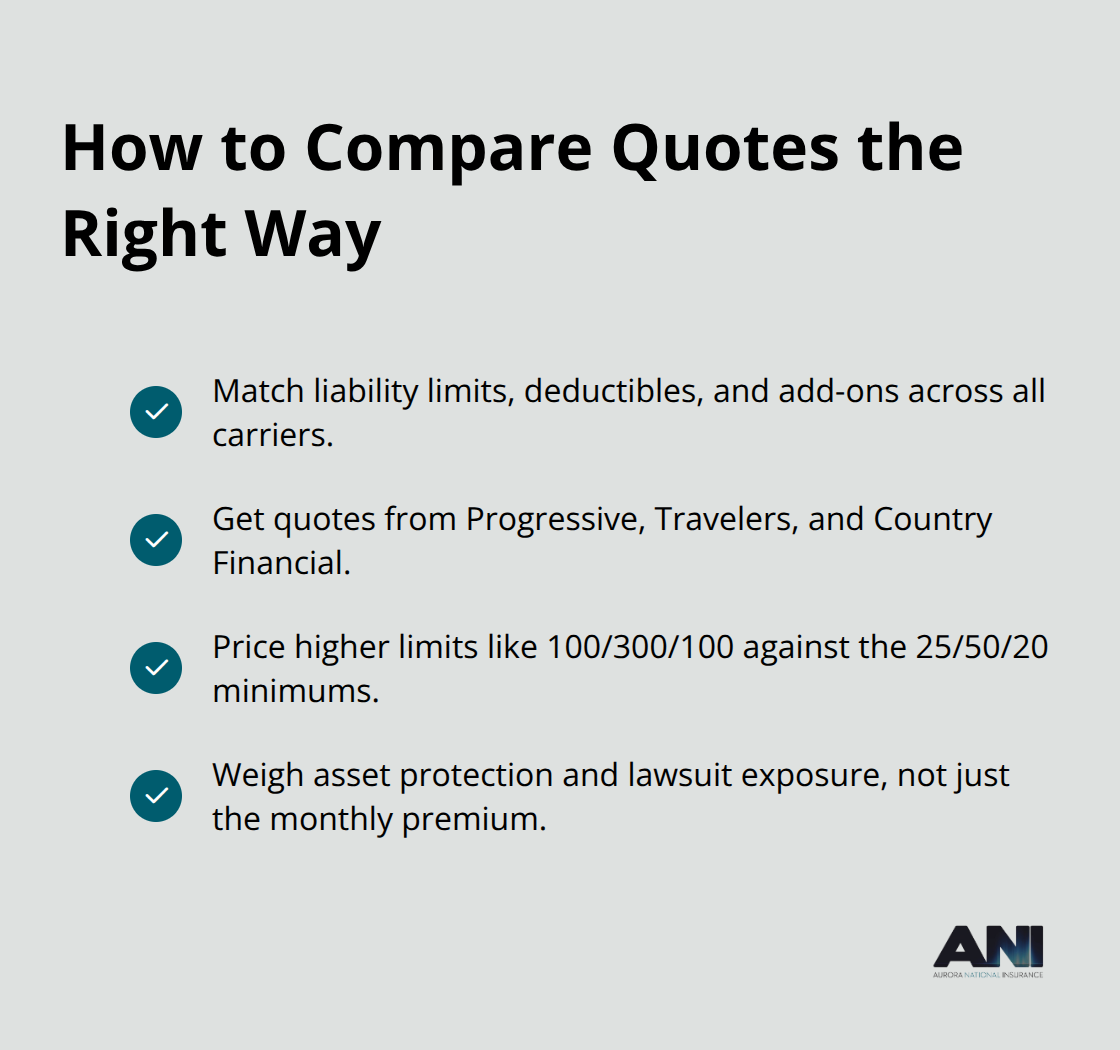

Compare Coverage Across Multiple Carriers

Comparing quotes requires identical coverage across carriers to matter at all. Request the same liability limits, deductibles, and additional coverages from each insurer so you’re genuinely comparing apples to apples. Progressive, Travelers, and Country Financial rank among Oregon’s top-rated commercial auto carriers, and getting quotes from all three takes less than an hour online.

Higher liability limits like 100/300/100 often cost only slightly more than the state minimum of 25/50/20, so calculate what makes financial sense for your business assets and potential lawsuit exposure rather than defaulting to minimum coverage.

Review Policy Language and Ask Direct Questions

Once you receive quotes, the real work begins-reviewing the actual policy language matters far more than fixating on the monthly premium. Ask each carrier directly whether hired and non-owned vehicle coverage is included or costs extra, how they handle permanently attached equipment, and whether your specific industry faces any exclusions or restrictions. Some carriers exclude certain high-risk uses or require additional training certifications, so clarifying these details prevents coverage denials when you actually need the protection.

Verify Coverage Details Before Commitment

Request a certificate of insurance in writing before you commit, and verify that the policy effective date aligns with when you need coverage active on your vehicles. This step protects your business from operating without proper protection and confirms that the carrier has accepted your application with the exact terms you negotiated. With quotes compared and policies reviewed, you’re ready to identify the coverage gaps that most Oregon business owners overlook.

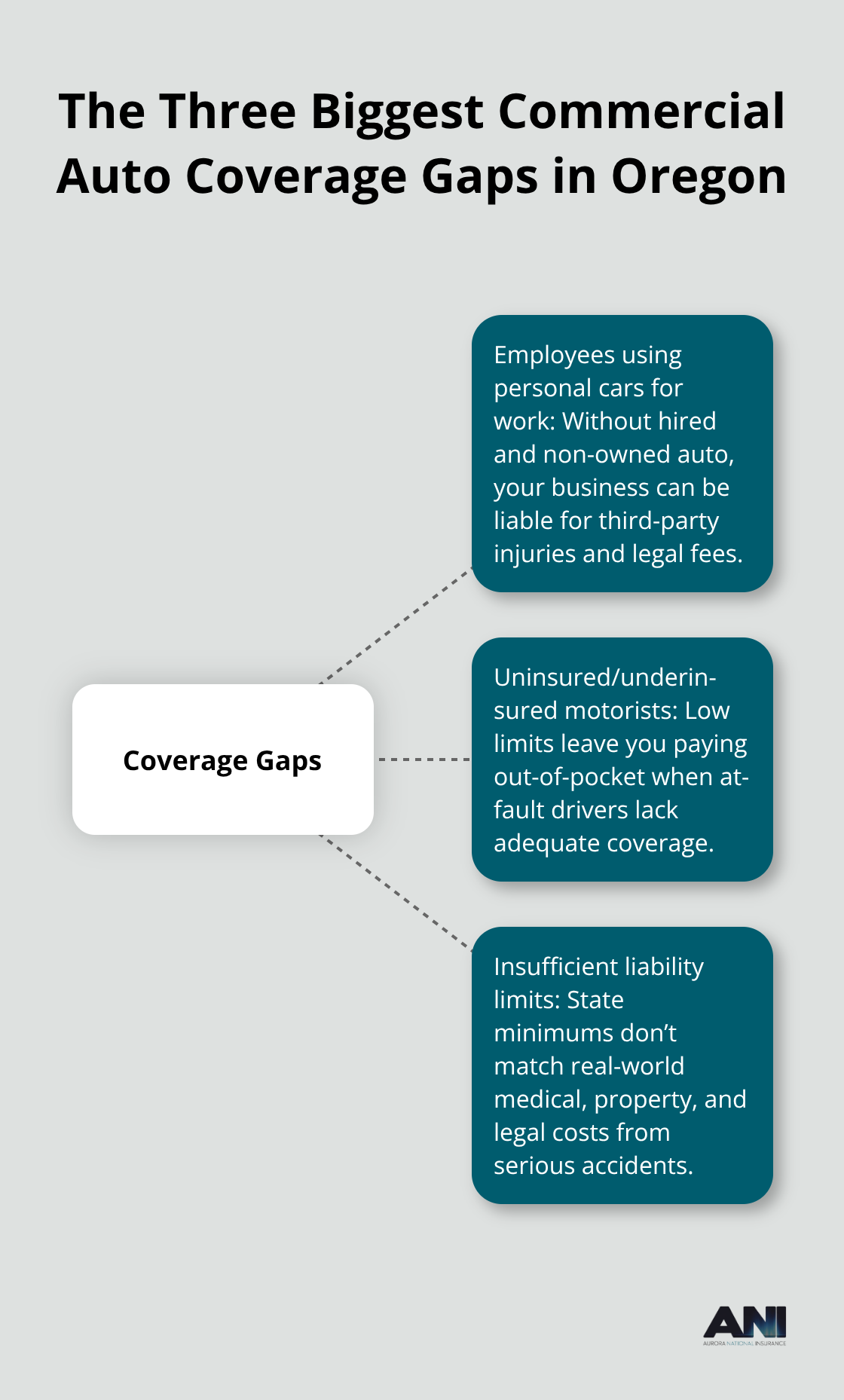

Common Coverage Gaps Business Owners Miss

Most Oregon business owners discover coverage gaps only after an accident exposes them. Your commercial auto policy may seem comprehensive, but three specific gaps create massive financial exposure that catches owners off guard. Employees driving personal vehicles for work, accidents involving uninsured drivers, and liability limits that fail to match your actual business risk represent the three biggest blind spots in Oregon commercial auto coverage.

These gaps exist because standard policies are built around single-vehicle operations, not the complexity of how modern businesses actually use vehicles.

When Your Employees Drive Their Own Cars for Work

Hired and non-owned vehicle coverage protects your business when employees use personal vehicles for work tasks. Without it, you face full liability if an employee’s personal car is involved in a work-related accident, even though you don’t own the vehicle. This coverage pays medical expenses and legal fees for third parties injured in the accident, but it doesn’t cover damage to the employee’s personal vehicle itself. The critical detail most owners miss is that their personal auto policy doesn’t extend coverage to business use, and their commercial auto policy doesn’t cover vehicles they don’t own.

If your employee hits another car while making a delivery in their own vehicle, your business becomes the liable party without this coverage. Adding hired and non-owned vehicle protection costs minimal amounts compared to the exposure you face. Get explicit confirmation from your insurer that this coverage is included in your quote, because some carriers charge extra or exclude it entirely depending on your industry and how frequently employees drive personal vehicles for work.

Uninsured Drivers Create Unplanned Expenses

Oregon requires uninsured motorist coverage with minimum limits of 25/50, but most business owners carry only the state minimum despite operating vehicles constantly on Oregon roads. Uninsured motorist protection covers medical expenses and lost wages when another driver without insurance hits you, and underinsured motorist coverage extends protection when the at-fault driver’s insurance limits are too low to cover your damages. The reality is stark: uninsured drivers cause significant accidents in Oregon, and if you’re hit by one, your business absorbs the costs unless you have robust protection.

Increasing your uninsured motorist limits from the state minimum to 100/300 costs very little but protects your business from catastrophic financial loss. This coverage becomes especially important if your vehicles are involved in accidents regularly or if your business depends on vehicle availability to generate revenue. You should compare quotes at these elevated limits to see the actual cost difference, which often surprises business owners with its modest increase.

Liability Limits That Actually Match Your Business Exposure

Oregon’s minimum liability requirement of 25/50/20 provides almost no protection for a business vehicle. A single serious accident involving your vehicle can generate medical bills exceeding $100,000, property damage claims above $50,000, and legal fees that push total exposure well beyond state minimums. Your personal assets face seizure if a judgment exceeds your policy limits, which happens routinely in serious injury cases.

Higher limits like 100/300/100 or 250/500/250 cost only marginally more than minimum coverage but provide genuine protection for your business. Progressive and Travelers often price these elevated limits competitively in Oregon, so comparing quotes at higher limits reveals that the cost difference is far smaller than most owners assume. Calculate your actual exposure based on your vehicle type, number of employees who drive, industry, and annual mileage, then select limits that protect both your business assets and personal wealth from a major lawsuit.

Final Thoughts

Choosing the right commercial auto coverage for your Oregon business requires matching protection to your actual risk, not defaulting to state minimums that leave you exposed. Vehicle type, industry, number of drivers, and annual mileage all shape which coverage limits make financial sense for your operation. A construction business with multiple trucks and expensive mounted equipment faces entirely different risks than a consulting firm with one vehicle used occasionally for client meetings.

Start by gathering your business details and vehicle information, then request Oregon commercial auto quotes from multiple carriers at identical coverage levels. Progressive, Travelers, and Country Financial consistently rank among Oregon’s top-rated options, and comparing their quotes takes minimal time online. Request higher liability limits like 100/300/100 alongside minimum coverage quotes so you see the actual cost difference, which often surprises business owners with its modest increase.

Verify that hired and non-owned vehicle coverage is included, confirm how permanently attached equipment is handled, and ask whether your specific industry faces any exclusions. A licensed insurance agent who understands Oregon’s commercial auto landscape makes this process faster and more reliable by catching coverage gaps you might miss and explaining policy language in plain terms. Once you’ve selected a policy, request a certificate of insurance in writing and verify the effective date aligns with when you need coverage active on your vehicles.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.