Retail Fleet Auto Insurance: Managing Risk Across Your Vehicles

Retail fleet auto insurance isn’t optional for businesses with multiple vehicles on the road. One accident involving a company vehicle can expose your business to significant liability claims and repair costs that threaten your bottom line.

At Aurora National Insurance, we understand the real financial pressure fleet owners face. The right coverage protects your vehicles, drivers, and business from unexpected losses while keeping your premiums manageable.

Why Your Retail Fleet Faces Real Liability Exposure

Retail businesses operate on thin margins, and one serious accident involving a company vehicle can wipe out months of profit. Commercial auto claims in the United States have logged 13 consecutive years of underwriting losses, and liability claim severity has risen due to social inflation and nuclear verdicts. When a delivery driver or service technician injures someone or damages property, your business becomes the defendant-and settlements routinely exceed what many retail owners expect. A single bodily injury verdict can reach six or seven figures, especially if the injured party pursues litigation. Without proper fleet coverage, you face personal liability for these costs, and your business assets are at risk.

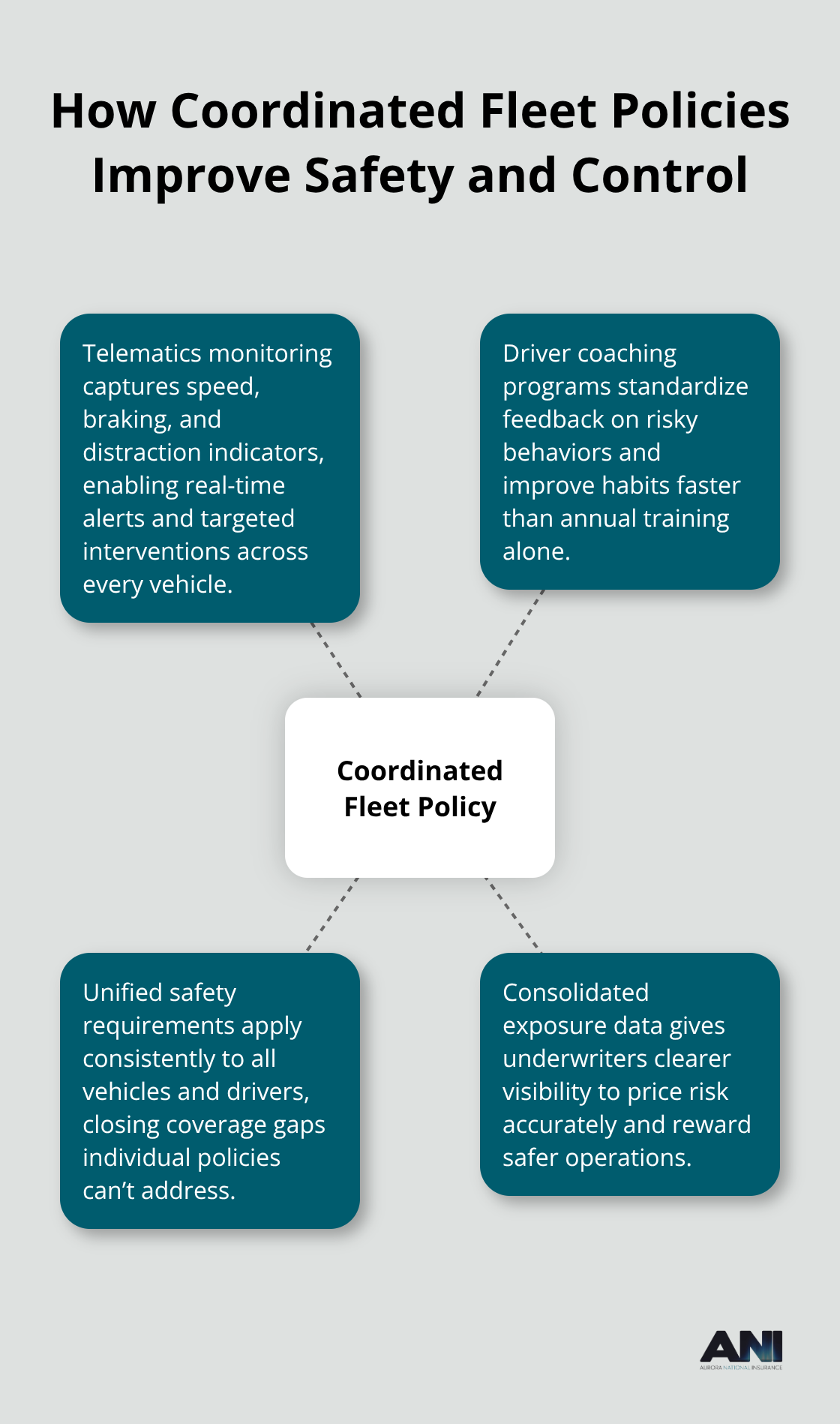

Why Multiple Vehicles Demand Coordinated Coverage

Individual auto policies for each company vehicle create inefficiency and leave gaps in protection. A fleet policy consolidates all your vehicles under one agreement, simplifies administrative overhead, and ensures consistent coverage across your entire operation. More importantly, it gives insurers visibility into your complete driving exposure-vehicle types, driver profiles, mileage patterns, and accident history. This transparency allows underwriters to price your risk accurately rather than treating each vehicle in isolation.

Retail fleets with delivery vans, service trucks, or company cars need coverage that accounts for how drivers actually use these vehicles. Distracted driving alone causes over 3,000 deaths and 424,000 injuries annually in the United States, according to the Centers for Disease Control and Prevention, and retail delivery drivers face constant temptation to check phones while navigating traffic. Fleet policies let you implement telematics monitoring, driver coaching programs, and safety requirements across all vehicles simultaneously-something individual policies cannot do.

Repair Costs Rise Faster Than Your Revenue

Vehicle repair costs have climbed steadily due to advanced safety technology, supply chain disruptions, and inflation. Physical damage costs are rising because of these factors, leading to higher repair bills and longer claim resolution times. Retail businesses cannot absorb these costs from operating cash flow.

A single collision involving a modern vehicle with lane-detection systems, autonomous-braking components, and electronic stability control can cost $15,000 to $30,000 or more to repair-far beyond what most small business owners budget for. Comprehensive and collision coverage protects you from these shocks, but only if your policy limits match current repair costs. You should review your coverage limits annually and adjust them upward if vehicle values or repair costs in your market have increased.

These rising costs make the next step-understanding what coverage options actually protect your fleet-more important than ever.

What Coverage Actually Protects Your Fleet

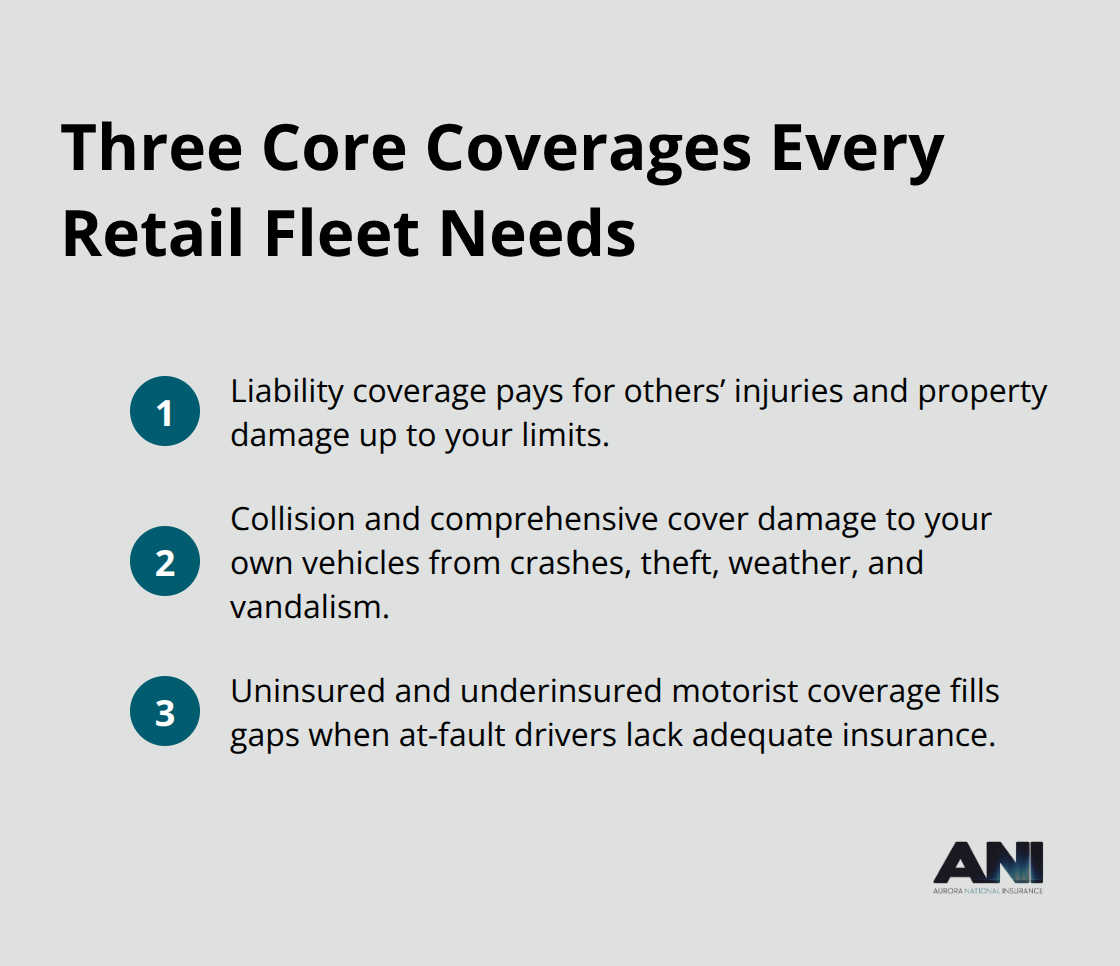

Liability Coverage: Your First Line of Defense

Liability coverage forms the legal foundation of every fleet policy, and it’s non-negotiable. When your driver injures someone or damages their property, liability coverage pays their medical bills, lost wages, and legal judgments-up to your policy limit. Most retail fleet owners set limits too low, which creates serious personal exposure. A serious injury claim routinely exceeds $100,000, and if your limit is $50,000, you personally owe the difference. Minimum limits of $250,000 per person and $500,000 per accident work better for retail fleets, though higher limits make sense if your vehicles operate in dense urban areas or carry high-value cargo. Third-party property damage claims-hitting a parked car, damaging a storefront, or destroying someone’s fence-are separate from bodily injury claims, so your liability limit must cover both exposures simultaneously.

Collision and Comprehensive Coverage: Protecting Your Assets

Collision and comprehensive coverage protects your own vehicles, and this is where repair cost inflation hits hardest. Collision covers damage from crashes, while comprehensive covers theft, weather, vandalism, and catalytic converter theft, which has become a serious problem for stationary fleets. Modern vehicles with advanced safety technology cost significantly more to repair than older models, and supply chain delays mean repair shops often wait weeks for parts, extending downtime and lost productivity.

Your deductible directly affects your premium, but choosing a $2,500 deductible just to save money on the premium creates real risk. If your van needs a $10,000 repair, you’ll pay that deductible out of pocket. Most retail fleets perform better with $1,000 or $1,500 deductibles that balance affordability with manageable out-of-pocket costs.

Uninsured and Underinsured Motorist Coverage: Filling the Gaps

Uninsured and underinsured motorist coverage protects you when another driver causes an accident but lacks adequate insurance-a real threat given that roughly one in eight drivers nationwide carries no insurance. If an uninsured driver injures your driver or damages your vehicle, this coverage steps in and covers medical expenses, lost wages, and repair costs up to your policy limit.

Underinsured motorist coverage fills the gap when the at-fault driver’s liability limit is too low to cover your damages, which happens frequently in low-income areas where drivers carry minimal coverage. This coverage is often overlooked but deserves serious attention because it protects your drivers and your bottom line when someone else’s negligence creates a protection gap.

Understanding these three coverage pillars positions you to make informed decisions about your fleet’s specific needs. The next step involves identifying which strategies actually reduce your premiums without sacrificing the protection your business requires.

How to Cut Fleet Insurance Costs Without Cutting Safety

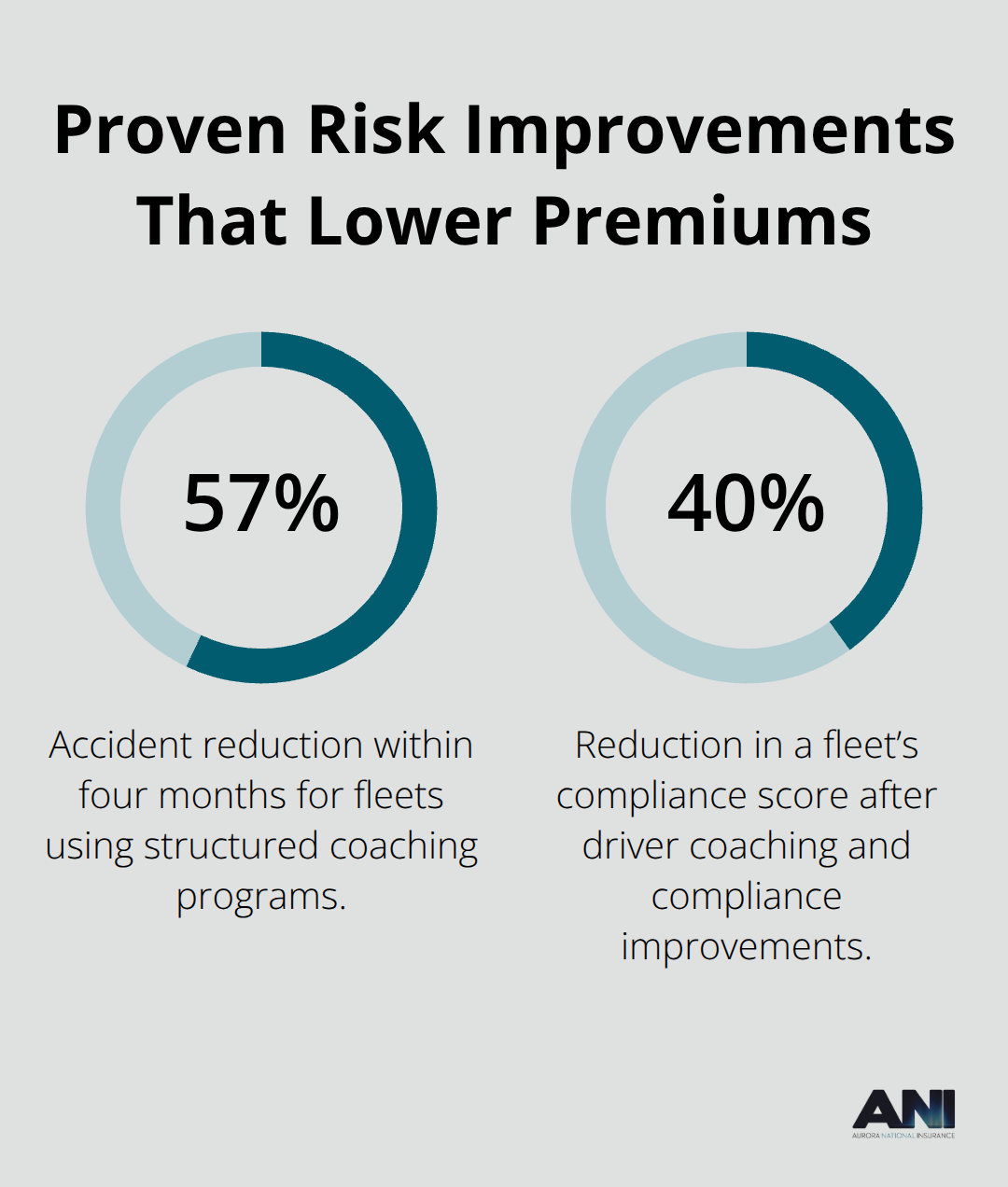

Reducing your fleet insurance premium requires hard evidence that your drivers and vehicles pose less risk than the average retail operation. Insurers do not lower rates based on promises or good intentions-they respond to measurable data showing fewer accidents, better maintenance, and safer driving habits. The most effective cost reduction strategy combines driver accountability, vehicle reliability, and real-time monitoring systems that give insurers confidence in your risk profile. A 2023 study showed that fleets using structured coaching programs saw 57% fewer accidents within four months, a reduction substantial enough to justify rate negotiations with your carrier. Before you renew your policy, you need concrete evidence of these improvements to present to your insurer and justify lower premiums.

Driver Training and Accountability Transform Your Risk Profile

Driver behavior directly drives your accident frequency and claim costs, which means training programs deliver measurable ROI. The most effective approach combines initial safety training with ongoing in-vehicle coaching that identifies specific risky behaviors-hard braking, speeding, distracted driving, and unsafe following distance-then corrects them in real time. Nine people in the United States are killed every day in crashes involving distracted drivers, and retail delivery drivers constantly battle phone temptation while navigating traffic. Telematics systems with in-cab coaching capabilities alert drivers when they exceed speed limits or brake too hard, creating immediate feedback that changes behavior faster than annual training sessions.

When you implement this level of accountability, document the accident reduction and share it with your insurer during renewal. Expressway Logistics achieved a 40% reduction in their compliance score and lowered insurance costs through driver coaching and compliance improvements, demonstrating that measurable risk reduction translates to premium reductions. Your insurer wants evidence that your drivers meet minimum safety standards, so enforce escalation policies for drivers who fail to meet performance benchmarks-online safety training for minor violations and removal from service for serious infractions.

Preventive Maintenance Reduces Breakdowns and Claims

Vehicle maintenance directly impacts both your downtime and your claims frequency because mechanical failures often trigger accidents. A well-maintained fleet experiences fewer breakdowns that could strand drivers on roadways or cause collision-related incidents. Track maintenance using your telematics system to identify vehicles approaching service intervals based on mileage and engine hours, then schedule maintenance before problems develop. Supply chain delays mean repair shops often wait weeks for parts, extending downtime and lost productivity, so preventive maintenance that avoids emergency repairs also avoids these delays.

Require drivers to report defects immediately using digital vehicle inspection reports that let them photograph damage and timestamp the report, streamlining your maintenance workflow and preventing small issues from becoming expensive repairs. This data also helps your insurer understand that you maintain your vehicles to manufacturer specifications, supporting your case for lower premiums at renewal. Modern vehicles with advanced safety technology cost significantly more to repair when damaged, making prevention more valuable than ever.

Telematics Data Creates Negotiating Power at Renewal

Telematics and GPS tracking systems generate the specific data insurers use to assess your actual risk, not industry averages. When you deploy these systems across your entire fleet, you capture speed, braking patterns, location, mileage, and maintenance intervals-information that proves your fleet operates more safely than carriers assume. Before renewal, compile this data into a simple report showing your accident rate compared to similar retail operations, your average speed patterns, your maintenance compliance, and any safety improvements over the past year.

Insurers benchmark fleet performance against comparable operations, so demonstrating that your accident rate falls below industry norms gives you leverage to negotiate better rates. The data also helps you identify high-risk drivers early and intervene with training before they cause expensive accidents. Real-time alerts let you reroute vehicles away from hazardous weather or high-crime areas, reducing physical damage and theft claims that inflate your premiums. Without this data, insurers rely on claims history and general assumptions about retail fleets, which often results in higher rates. With documented evidence of lower risk, you have concrete justification for premium reductions at renewal.

Final Thoughts

Retail fleet auto insurance protects your business from the financial devastation that follows a serious accident. Your vehicles represent significant capital investment, and the liability exposure they create can exceed your annual profit in a single claim. The right policy structure-combining liability, collision, comprehensive, and uninsured motorist coverage-creates a complete safety net that keeps your business solvent when accidents happen.

Your actual premium depends entirely on the risk you present to insurers, and driver training programs that reduce accidents by 57% within months, preventive maintenance that prevents breakdowns, and telematics systems that document your safety performance all translate to measurable premium reductions at renewal. Insurers respond to hard data, not promises, so compile evidence of lower accident rates, safer driving patterns, and consistent vehicle maintenance to gain real negotiating power. When you present this information at renewal, you lower your costs without sacrificing protection.

Start by documenting your current fleet composition, annual mileage, driver profiles, and accident history, then request quotes from multiple providers and ask each one how your safety improvements affect your rate. Aurora National Insurance provides instant online quotes and expert consultation to help you find the right retail fleet auto insurance protection at competitive prices. The difference between adequate coverage at a fair price and inadequate coverage at a bargain price determines whether your business survives the next accident.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.