Oil Service Vehicle Insurance: Insuring Your Specialized Fleet

Oil service vehicles face risks that standard commercial auto policies simply don’t cover. From specialized equipment to hazardous cargo, your fleet operates in a different category than typical business vehicles.

At Aurora National Insurance, we understand that oil service vehicle insurance requires tailored protection. This guide walks you through the coverage options, cost factors, and strategies that keep your operations protected.

Why Oil Service Vehicles Need Different Insurance

Standard commercial auto policies exclude most of what makes your oil service operation run. A typical business auto policy won’t cover hazardous materials transport, specialized equipment mounted on vehicles, or the liability exposure that comes with servicing oil and gas operations. Oil service fleets operate in high-risk environments where standard coverage creates dangerous gaps. Clients who purchase generic commercial auto policies often discover mid-claim that their equipment damage, cargo loss, or pollution liability falls outside their coverage.

The equipment and cargo problem

Your vehicles carry expensive specialized equipment and hazardous cargo that standard policies treat as invisible. A well truck hauling completion fluids, a service rig with downhole tools, or a transport vehicle carrying diesel and chemicals represents significant asset value that generic commercial auto won’t protect. If your truck catches fire or gets stolen, standard collision and comprehensive coverage caps out at the vehicle itself-not the equipment mounted on it.

Pollution liability becomes critical here too. If your vehicle leaks hydraulic fluid or hazmat cargo spills during transport, you face cleanup costs, regulatory fines, and third-party claims. Oil service fleets need dedicated pollution liability coverage as a separate rider, not an afterthought. Physical damage coverage for oil service vehicles must account for equipment value separately from vehicle value, or you’ll face massive out-of-pocket losses on total loss events.

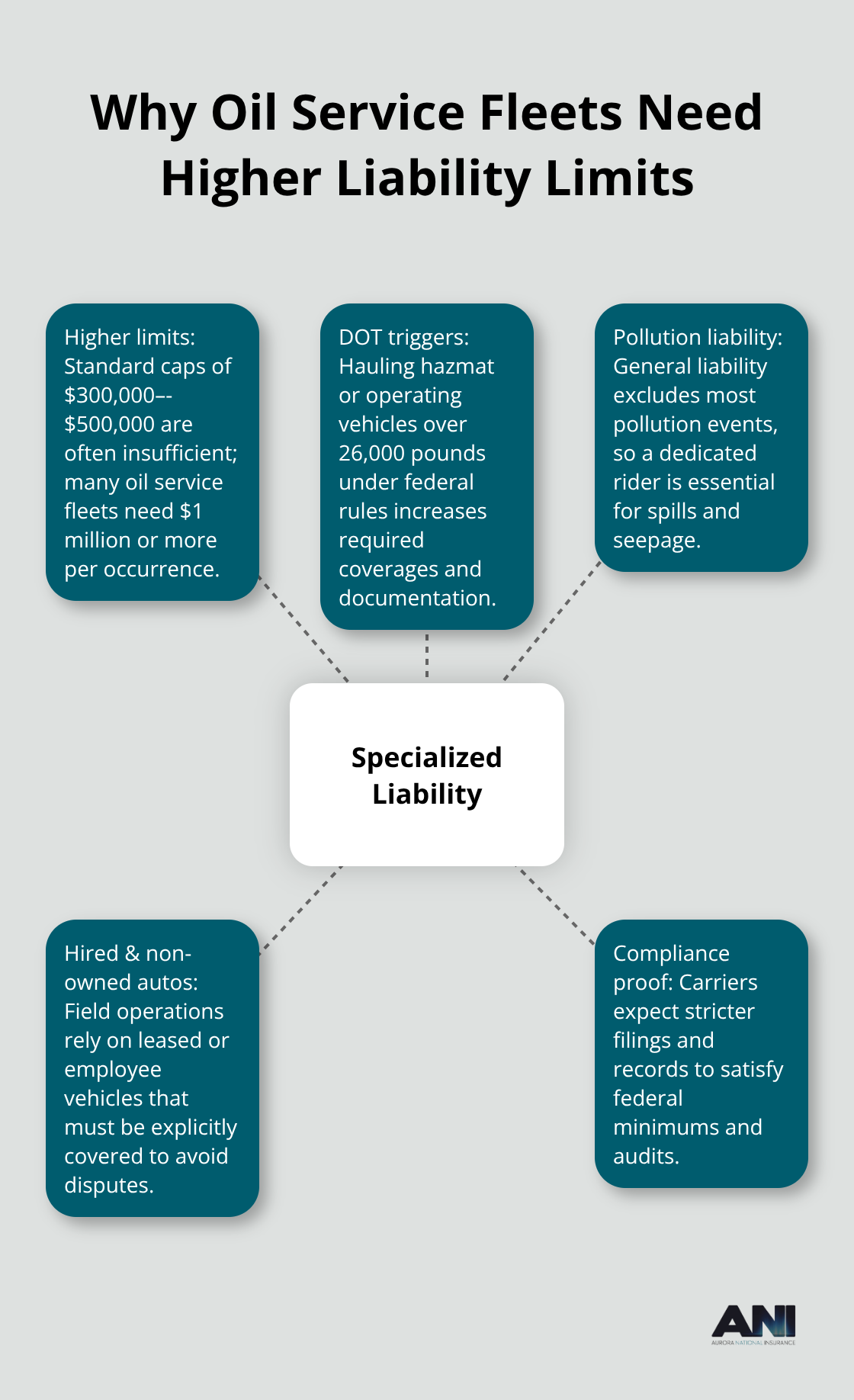

Why liability exposure in oil service work demands specialized limits

Oil service operations create liability exposures that multiply fast. Your workers service wells on customer property, operate heavy equipment near populated areas, and transport hazardous materials across state lines. A single incident-a worker injured on a well site, equipment damaging customer infrastructure, or a vehicle accident involving hazmat-can generate claims exceeding $1 million.

Standard commercial auto liability caps often max out at $300,000 to $500,000 per occurrence, leaving you exposed. Oil service vehicle insurance requires higher liability limits, typically $1 million or more per occurrence, to match the actual risk profile. Additionally, your drivers operate under federal Department of Transportation regulations if you transport hazmat or operate commercial vehicles over 26,000 pounds. These federal requirements often demand higher coverage minimums and stricter compliance documentation than state minimums.

Your policy must explicitly cover hired and non-owned vehicles too, since field operations often require leased equipment or employee personal vehicles used for business purposes. One accident involving a leased service truck can trigger coverage disputes that tank your business if your policy doesn’t explicitly address hired auto coverage. Understanding these gaps sets the stage for selecting the right coverage options that actually protect your operation.

Coverage Your Oil Service Fleet Actually Needs

Pollution Liability: The Non-Negotiable Coverage

Pollution liability stands apart as the coverage that separates oil service fleets from ordinary commercial operations. A single spill or leak exposure can exceed $500,000 in cleanup costs plus regulatory fines and third-party claims. Your policy must cover sudden and gradual pollution conditions, meaning both an immediate hazmat spill during transport and slow seepage from equipment mounted on your vehicles. General liability policies exclude most pollution-related incidents, leaving you personally liable for environmental cleanup.

When you select pollution coverage, verify the policy covers on-site and off-site pollution, transportation-related incidents, and employee error. This protection matters because your operations expose you to environmental liability that typical business vehicles never face.

Physical Damage and Equipment Protection

Physical damage coverage for your vehicles requires higher limits than typical commercial auto because your equipment value often exceeds the vehicle value itself. A completion fluid truck worth $80,000 with $150,000 in specialized equipment mounted on it needs coverage that reflects the $230,000 total asset at risk. Request separate equipment coverage riders that cover tools, pumps, meters, and other specialized gear independently from the vehicle itself. This prevents the insurer from offsetting equipment claims against vehicle damage limits.

Comprehensive and collision coverage should include hired and non-owned vehicle protection since your operations frequently involve leased service trucks or employee personal vehicles used for business. The Federal Motor Carrier Safety Administration requires hired auto coverage if your drivers operate leased commercial vehicles, and most states impose liability minimums between $750,000 and $1 million for hazmat transport.

Workers Compensation and Employee Injury Protection

Workers compensation and employee benefits form the second pillar because your workers face injury risks that stationary businesses never encounter. Oil field work generates significantly higher workers compensation claim frequency and severity than office-based operations, with the Occupational Safety and Health Administration reporting that extraction and service industries experience injury rates roughly three times higher than average. Your policy must cover employees working on customer property, in remote locations, and around hazardous materials.

Medical payments coverage should extend to third-party injuries on your job sites since your crews often work on customer wells where bystanders or customer employees could be injured by your operations. Uninsured and underinsured motorist coverage protects your drivers when they’re hit by someone lacking adequate insurance, a genuine risk when operating in rural areas where uninsured motorist rates exceed 20 percent in some states. Try minimum limits of $500,000 per person and $1 million per occurrence for UIM coverage on oil service fleets.

Roadside Assistance for Remote Operations

Roadside assistance riders prove practical for fleets operating remote well sites where commercial towing services charge $2,000 to $5,000 for long-distance recovery. This coverage typically costs $200 to $400 annually per vehicle and eliminates the negotiation stress during breakdowns in isolated locations where you have limited options. Your drivers benefit from immediate support when equipment fails far from urban service centers, reducing downtime and operational disruption.

With these core coverages in place, you can shift focus to the cost factors that actually move your premium needle and the strategies that reduce what you pay.

What Drives Your Oil Service Fleet Insurance Costs

Your oil service fleet premium reflects factors you control and factors you don’t, but the controllable ones matter far more than most operators realize. Vehicle age, driver records, and maintenance history form the foundation of how insurers price your coverage, yet most fleet managers focus on negotiating the premium rather than addressing the underlying risk factors that determine it.

How Vehicle Maintenance and Age Affect Your Premiums

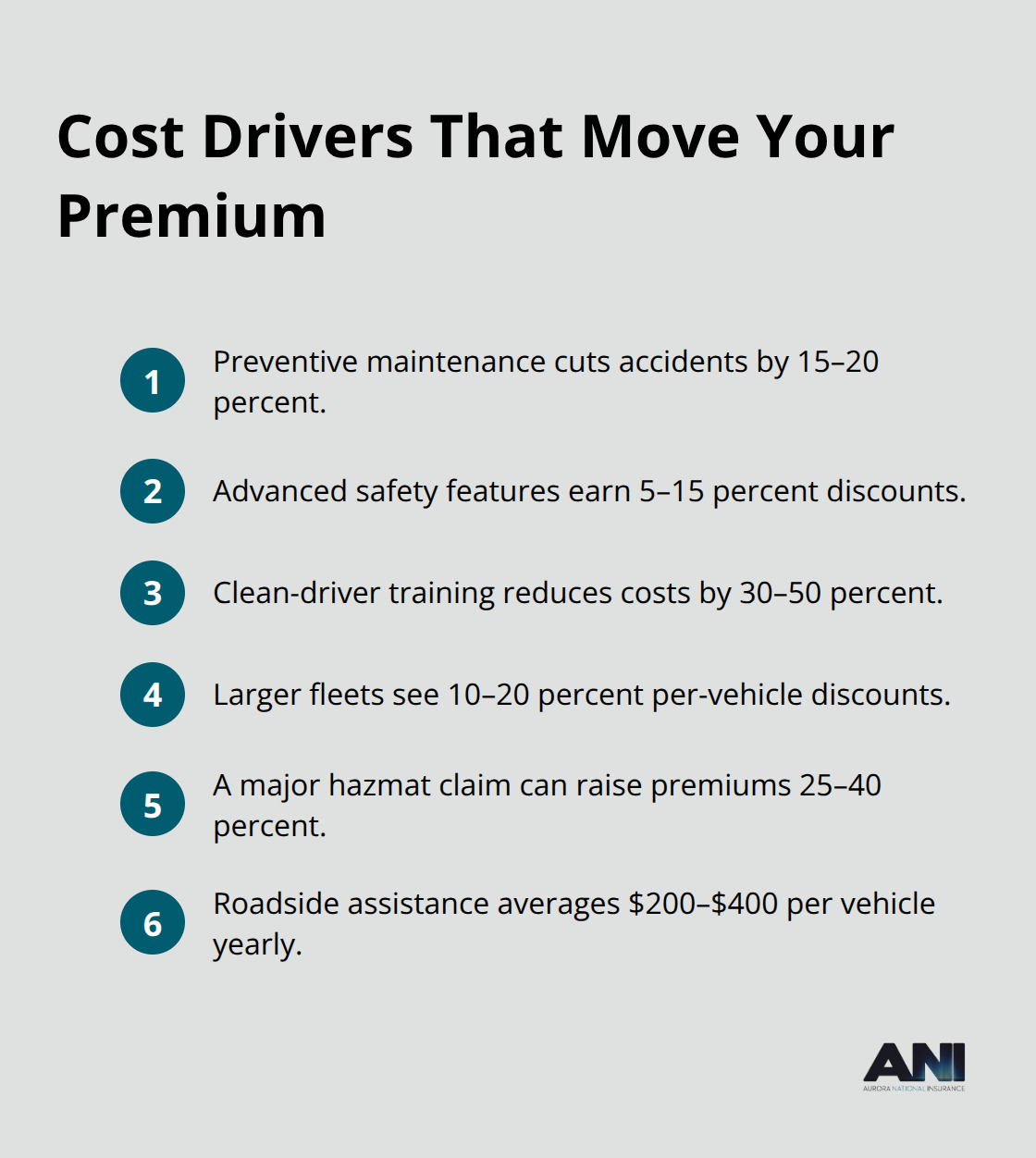

The Federal Motor Carrier Safety Administration data shows that fleets with documented preventive maintenance programs reduce accident frequency by 15 to 20 percent compared to fleets with reactive maintenance, which directly translates to lower premiums. A well-maintained truck with a clean service record costs substantially less to insure than an older vehicle with deferred repairs, even if both vehicles appear roadworthy. Insurers pull your maintenance records and driver histories during underwriting, so gaps in documentation or missed service intervals signal higher risk and trigger premium increases.

Your vehicles themselves matter significantly. Newer trucks with advanced safety features like automatic braking and lane-keeping systems qualify for carrier discounts ranging from 5 to 15 percent, while older vehicles without these systems face higher rates regardless of their actual condition.

Driver Training and Safety Records Impact Costs Most

Driver training and safety records dominate the controllable cost factors more than vehicle specifications. A driver with a clean record and documented safety training costs 30 to 50 percent less to insure than a driver with moving violations or prior accidents, making driver screening and ongoing training one of the highest-return investments you can make. Fleets that implement formal driver safety programs and require annual training see measurable reductions in claim frequency and premium costs over time.

Fleet Size and Claims History Shape Your Rate

Fleet size influences pricing significantly. Carriers typically reduce per-vehicle costs once you reach five or more vehicles under one policy, with some offering 10 to 20 percent discounts for larger fleets compared to single-vehicle policies. Your claims history determines whether you receive standard pricing or pay a substantial surcharge, and a single major claim involving hazmat spill cleanup or pollution liability can increase your renewal premiums by 25 to 40 percent for three to five years afterward.

Operating Territory and Multi-State Compliance

Your location and operating territory affect premiums substantially. Operating exclusively in Alaska costs less than cross-state operations that expose you to multiple jurisdictions and longer haul distances, since more miles driven means more exposure to accidents. If your fleet operates across Washington, Oregon, and Idaho, your premiums reflect that expanded territory and the regulatory complexity of multi-state compliance. Aurora National Insurance serves these primary markets and understands how regional operations influence your coverage needs and costs.

Final Thoughts

Oil service vehicle insurance protects your operation from exposures that standard commercial auto policies ignore. Specialized coverage for hazardous cargo, pollution liability, and equipment mounted on your vehicles addresses the real risks your fleet faces daily. Without tailored protection, a single incident involving hazmat spill cleanup, equipment damage, or third-party injury can devastate your business financially and operationally.

The cost factors we covered show that premiums reflect your actual risk profile. Driver training, vehicle maintenance, and safety records directly influence what you pay, meaning your operational decisions control a significant portion of your insurance expenses. A fleet with documented preventive maintenance and trained drivers costs substantially less to insure than one with reactive maintenance and inconsistent safety practices.

Your next step involves connecting with an insurance professional who understands oil service operations specifically. Generic insurance agents lack the expertise to identify coverage gaps or negotiate rates that reflect your actual risk management practices. Contact Aurora National Insurance for an instant online quote and let our licensed agents show you how proper oil service vehicle insurance reduces your risk and your costs across Alaska, Washington, Oregon, and Idaho.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.