Contractor General Liability Insurance: Covering Your Trade Skills

One accident on a job site can wipe out months of profit. That’s why contractor general liability insurance isn’t optional-it’s a business necessity.

At Aurora National Insurance, we’ve seen firsthand how the right coverage protects contractors from property damage claims, bodily injury lawsuits, and legal costs that could otherwise shut down operations. This guide walks you through what you actually need to know about selecting and securing the right protection for your trade.

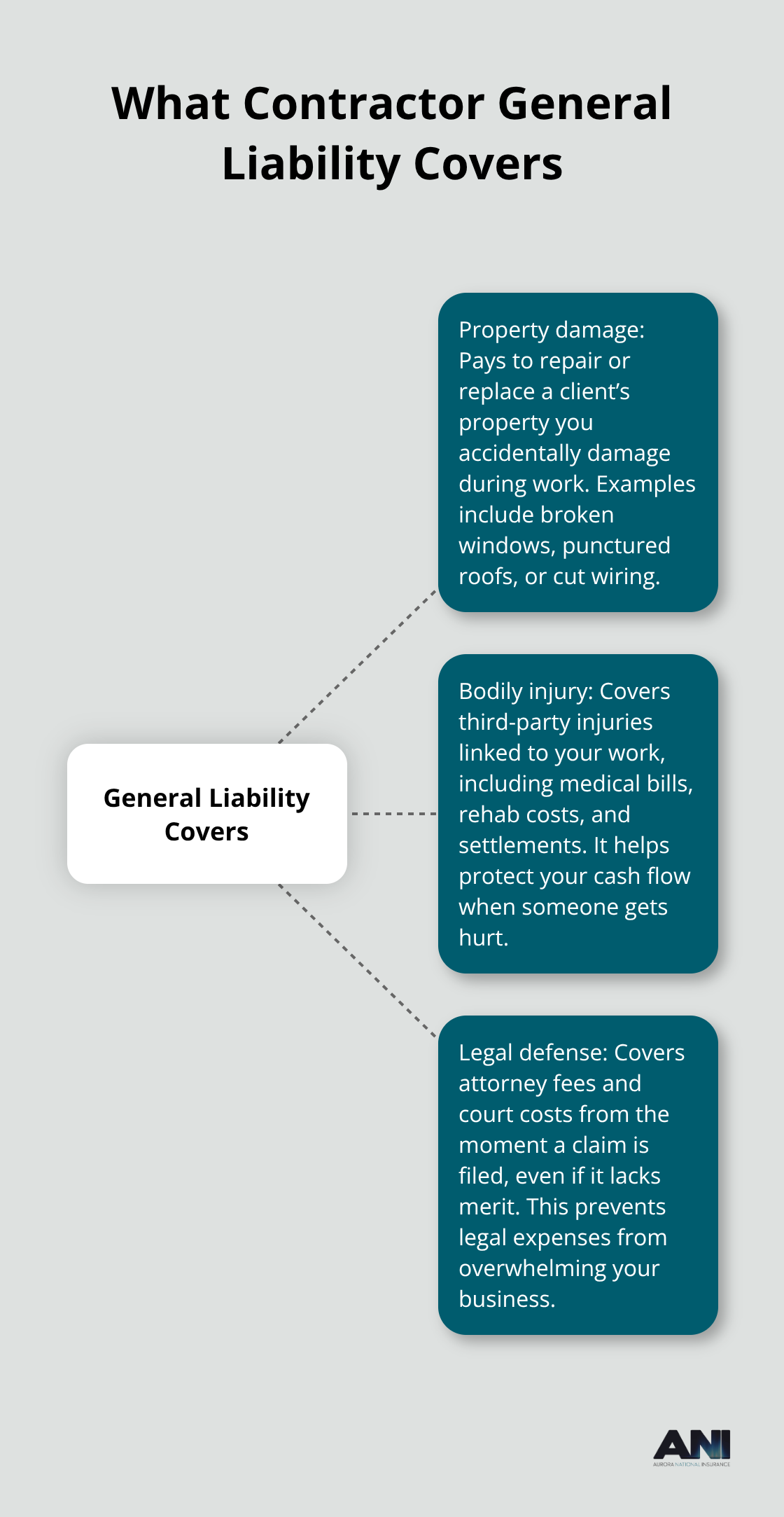

What Contractor General Liability Actually Covers

General liability insurance for contractors covers three categories of expenses that can devastate an unprepared business: property damage you cause during work, bodily injury claims from third parties, and the legal costs to defend yourself. When you damage a client’s property-whether that’s drywall, flooring, or plumbing fixtures-your policy pays for repairs or replacement. Bodily injury coverage steps in when someone gets hurt because of your work, handling medical bills, rehabilitation costs, and court settlements. Legal defense coverage covers attorney fees and court costs if a claim lands on your desk, which matters because construction litigation can easily exceed $50,000 in legal expenses alone before a verdict arrives.

Property Damage on Job Sites Requires Specific Attention

Property damage claims rank as the most common liability claims contractors face, yet many don’t understand what their policy actually covers. Your coverage pays when you accidentally damage a client’s belongings-a dropped tool through a window, a saw cutting through electrical wiring, or equipment that punctures a roof. The critical detail most contractors miss: your policy does not cover damage to your own tools and equipment. If your $3,000 drill gets stolen from a job site or your truck bed full of supplies gets damaged, that’s not covered under general liability. You need a separate tools and equipment floater or inland marine coverage for that protection. Completed operations coverage protects you if problems arise after a project finishes, like a plumbing repair that causes water damage weeks later.

Bodily Injury Claims and Legal Defense Work Together

When a subcontractor slips on your wet concrete, a homeowner’s guest trips over your extension cord, or a worker gets hit by equipment, bodily injury coverage activates. This coverage handles medical expenses, lost wages, pain and suffering claims, and settlements. Legal defense coverage runs separately and covers your attorney fees and court costs regardless of whether the claim has merit. This distinction matters because you’re protected from the moment someone files a claim, not just when you lose in court. Associated General Contractors of America guidelines recommend that commercial construction contracts require $1,000,000 per occurrence and $2,000,000 aggregate limits-far above typical state minimums ($50,000 to $300,000). Your client or project owner will likely demand these higher limits before they let you on site, which means understanding what limits you actually need before you bid is non-negotiable.

Contract Requirements Often Exceed State Minimums

Most contractors assume state licensing requirements set the bar for insurance coverage. That assumption costs money and creates risk. Your state may require minimal coverage-sometimes as low as $50,000-but your client’s contract demands $1,000,000 or more. Failing to meet contract requirements can block payment, trigger contract penalties, and damage your reputation with future clients. Project owners and lenders routinely require proof of coverage before work starts, making a certificate of insurance (COI) your ticket to the job. Understanding the gap between what your state requires and what your contracts demand determines whether you win bids or lose them to better-prepared competitors.

Common Claims That Cost Contractors Thousands

Third-Party Accidents on Job Sites

Third-party accidents happen constantly on job sites, and they cost money fast. A worker steps on loose scaffolding and breaks an ankle-medical bills, lost wages, and a potential lawsuit follow. A homeowner’s guest slips on freshly sealed concrete and hits their head-suddenly you face a settlement demand. These aren’t rare scenarios. Construction sites generate injury claims regularly, and without bodily injury coverage, you pay out of pocket. Your policy covers medical expenses and legal defense from the first incident report, which means you gain protection before a lawsuit even materializes.

Industry experts recommend substantial per occurrence limits for commercial work specifically because catastrophic injuries on job sites are real and expensive.

Property Damage During Active Work

Damage to client property during work creates the second category of claims contractors encounter constantly. You install new flooring and your nail gun fires through a water line behind the wall-that’s a repair bill plus water damage to cabinets and drywall. You remove old siding and your equipment punctures the client’s new deck railing. You run electrical work and accidentally cut through the homeowner’s fiber optic cable. These accidents happen to skilled contractors regularly because job sites are unpredictable. Your property damage coverage pays for repairs and replacement without touching your business bank account.

The detail that trips up contractors: this coverage applies only to client property, not your own tools or equipment. If your impact driver gets stolen from a locked truck or your ladder gets damaged on site, general liability doesn’t cover it-you need tools and equipment floaters for that protection.

Slip and Fall Incidents Beyond Your Control

Slip and fall incidents on your projects represent the third major claim type, and they’re expensive because liability protection extends beyond just your employees. A client walks through an active work zone and trips over a cable you left running across the floor. A delivery driver steps into an unmarked hole on a renovation site. A homeowner’s child steps on a nail you left on the porch. Your bodily injury coverage activates immediately, covering their medical treatment and any settlements.

The legal defense component matters here because slip and fall cases often involve witnesses, medical records, and disputed liability-attorney fees can accumulate quickly before trial. Having coverage means your insurer’s legal team handles the defense, not you managing depositions and court appearances while running your business. Understanding how these three claim types affect your bottom line shapes what coverage limits you actually need for your contracts and your peace of mind.

How to Match Coverage Limits to Your Real Contracts

Your Clients Set Your Insurance Requirements, Not Your State

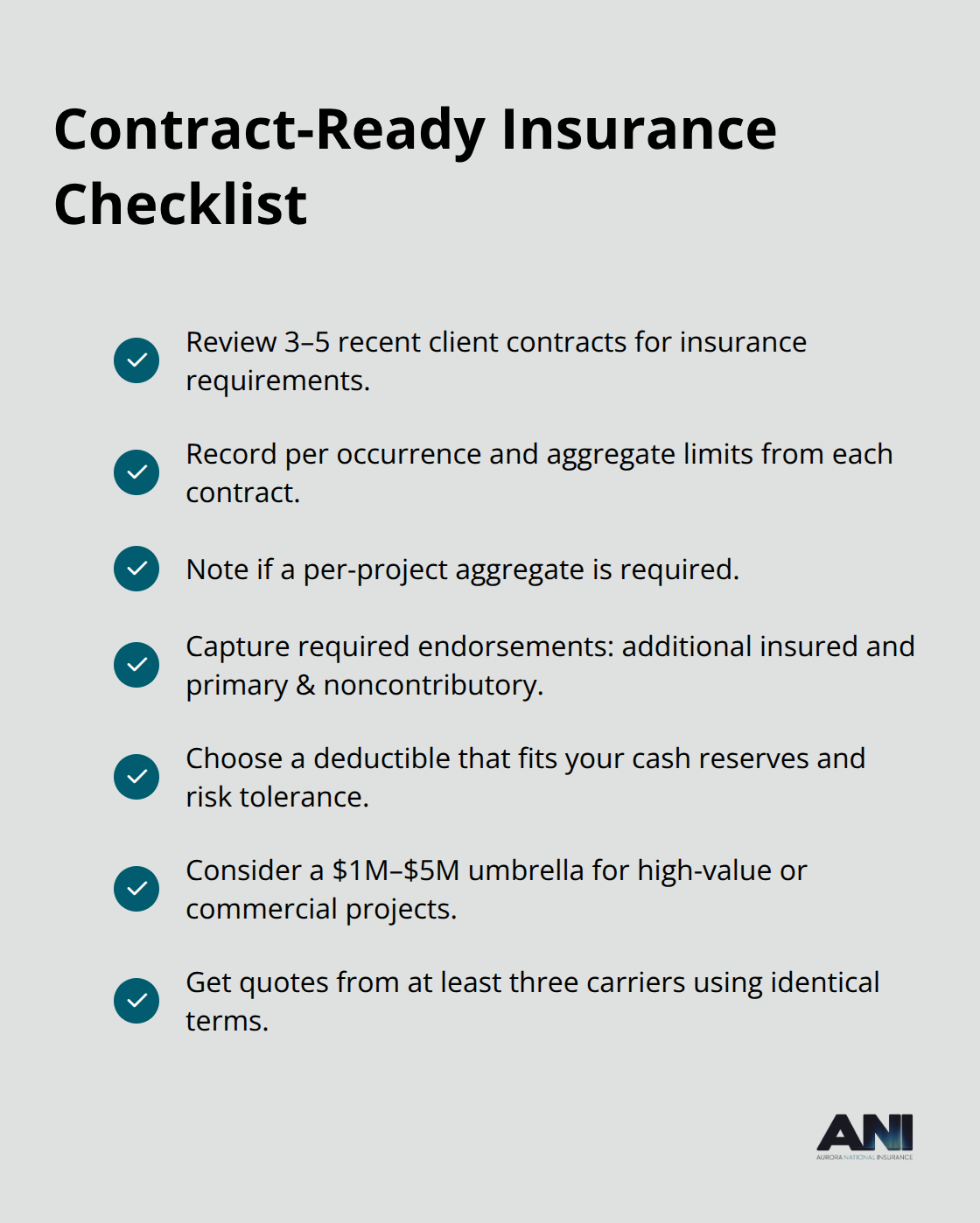

Your state licensing board does not set your insurance requirements-your clients do. This is the most important principle to understand before you spend a dollar on coverage. Associated General Contractors of America risk guidelines recommend $1,000,000 per occurrence and $2,000,000 aggregate limits for commercial construction contracts, and project owners routinely demand exactly these numbers or higher before allowing you on site. If you bid jobs with only $300,000 in coverage because that’s your state minimum, you will lose contracts to competitors who carry proper limits. Start by reviewing three to five of your actual client contracts and pull the insurance requirements from each one. Write down the specific per occurrence limits, aggregate limits, whether they demand per-project aggregates, and any endorsements like additional insured status or primary and noncontributory clauses. These are not theoretical numbers-they are the actual barriers between winning and losing work.

Deductibles Shape Your Monthly Cost and Financial Risk

Deductibles directly affect your out-of-pocket exposure and your premium cost, so this choice determines both your monthly payment and your financial risk. A $1,000,000 per occurrence policy with a $1,000 deductible typically costs around $824 annually according to The Hartford’s 2024 data, while raising that deductible to $2,500 or $5,000 reduces your premium but increases what you pay if a claim happens. Small contractors often select $1,000 deductibles because the premium difference is minimal and the protection feels worth it, while established contractors with stronger cash reserves sometimes move to $2,500 or $5,000 to lower annual costs. The math is straightforward: if you file a claim and your deductible is $5,000, you pay that amount before insurance activates.

Umbrella Coverage Protects Against Catastrophic Losses

Contractors working on high-value commercial projects frequently add umbrella liability coverage of $1,000,000 to $5,000,000 on top of their base general liability policy to handle catastrophic losses that exceed primary limits. This layered approach costs less than raising your primary limits alone and provides substantial protection without the premium shock of higher base coverage. Umbrella policies sit above your general liability, commercial auto, and workers’ compensation policies, activating only after those underlying limits are exhausted.

Compare Quotes from Multiple Carriers

Comparing quotes from multiple carriers is non-negotiable because rates vary significantly based on your trade type, project history, payroll size, and location. Request quotes from at least three carriers using identical coverage limits and deductibles from your contracts-same per occurrence limits, same deductibles, same endorsements. This apples-to-apples comparison reveals which carrier offers the best price for your specific risk profile. Some carriers specialize in certain trades and price them lower; an electrician might find better rates at one carrier while a roofing contractor gets the best deal elsewhere. Getting quotes takes 15 minutes online or a phone call with an agent, and the savings often exceed $200 to $500 annually just from shopping around.

Final Thoughts

Contractor general liability insurance protects your business from the financial devastation that follows a single accident on site. Without it, a property damage claim, bodily injury lawsuit, or legal defense bill drains months of profit and damages your reputation with future clients. The contractors who win bids and keep operations running understand what their contracts actually require and secure coverage that meets those demands before stepping on site.

Your state’s licensing requirements set a floor, not a ceiling-your clients set the real insurance bar. Most demand $1,000,000 per occurrence and $2,000,000 aggregate limits before allowing you to work, so starting with your actual contracts prevents costly gaps and ensures you bid competitively. Review three to five client agreements, extract the specific coverage limits and endorsements they require, and use those numbers when requesting quotes from carriers.

Comparing quotes from multiple carriers reveals where real savings happen, since rates vary significantly based on your trade type, project history, and location. The difference between insurers often exceeds $200 to $500 annually, and the process takes just 15 minutes online or a quick phone call. Get instant online quotes to connect with an agent who understands contractor general liability insurance inside and out.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.