General Liability Insurance Online: Quick Ways to Compare Quotes

General liability insurance protects your business from costly lawsuits and medical claims. Whether you’re a contractor, retailer, or service provider, this coverage is essential for managing financial risk.

Comparing general liability insurance online has never been faster. We at Aurora National Insurance help business owners find the right coverage at competitive rates by understanding what to look for when reviewing quotes.

What General Liability Insurance Actually Covers

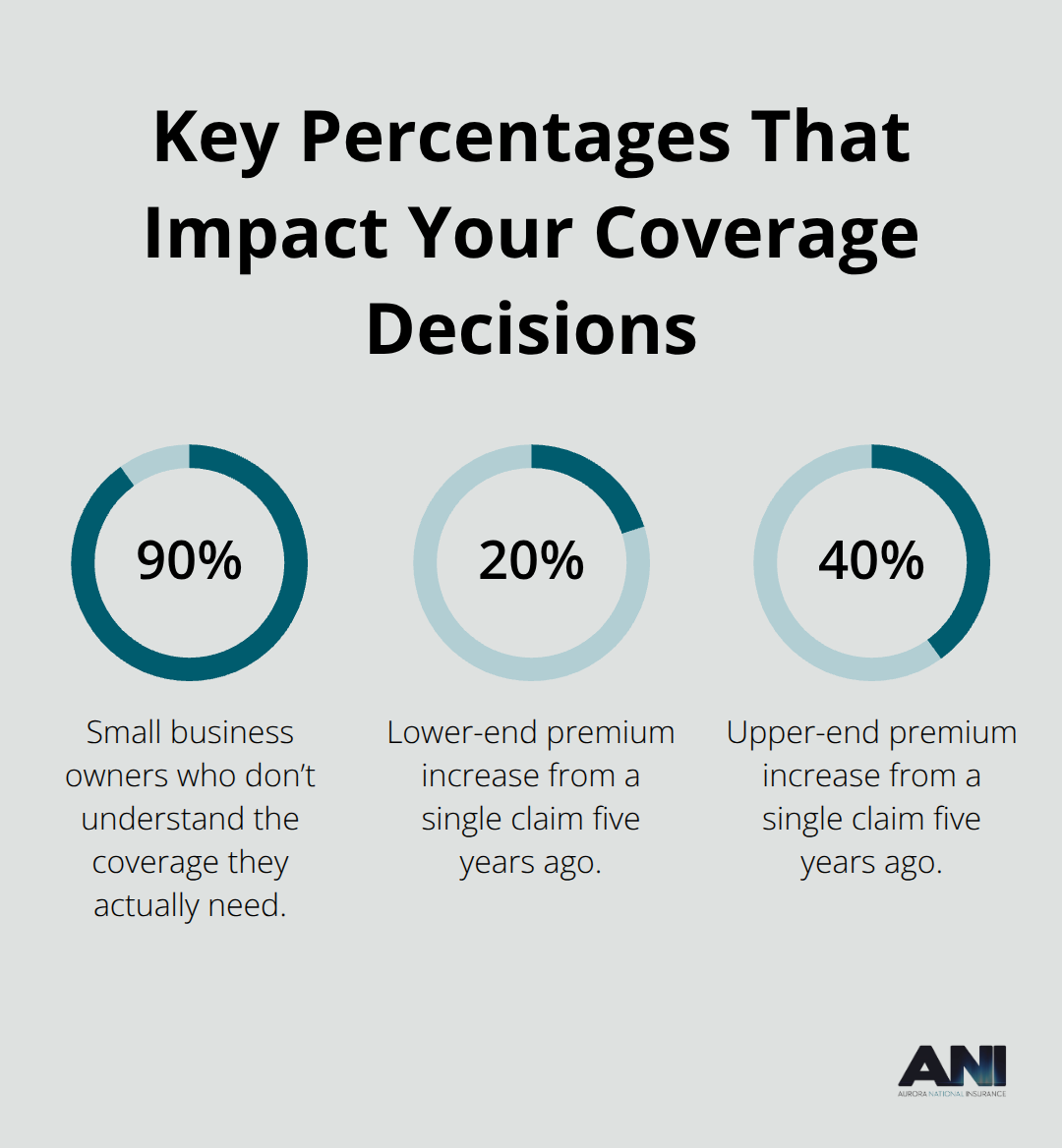

General liability insurance protects your business against third-party claims for bodily injuries and property damage that occur during normal operations. A customer slips on your wet floor, your equipment damages a client’s property, or someone claims your advertising misled them-general liability covers legal defense costs, medical bills, and settlements up to your policy limits. This protection matters in real situations; about 90% of small business owners don’t understand the coverage they actually need, which is why many end up underinsured or paying for unnecessary add-ons. The coverage includes third-party bodily injury, property damage liability, medical payments for minor injuries on your premises, and personal and advertising injury claims like defamation or trademark infringement. Most policies also cover your legal defense costs, which can exceed $100,000 for a single lawsuit, making this protection financially critical regardless of your business size.

Why Your Industry Determines Your Coverage Needs

Different business types face different risks, and your industry directly affects both what you need and what you’ll pay. Contractors face higher claims from job site accidents, while retail businesses worry more about customer slip-and-falls. IT consultants and service providers need professional liability coverage alongside general liability because they face different exposure-mistakes in their work cause financial harm rather than physical injuries. The Hartford, Acuity, and Liberty Mutual dominate coverage for construction contractors, while Chubb and Hiscox specialize in technology startups. Food and beverage businesses need liquor liability coverage and kitchen fire protection, making their policies more complex than a typical service business. Your annual revenue and number of employees also matter; a one-person consulting firm with $200,000 in annual revenue faces different risk than a cleaning service with ten employees generating the same revenue. Understanding your specific industry risk prevents you from buying coverage you don’t need while identifying gaps that could bankrupt you.

Policy Limits Matter More Than Premium Price

Most small business owners focus on monthly cost when comparing quotes, but the actual limits determine whether your insurance protects you or leaves you exposed. General liability policies typically include a per-occurrence limit and an aggregate yearly limit. A $1 million aggregate limit with a $500,000 per-occurrence limit means you’re covered up to $500,000 for a single incident, but your total coverage for the entire year maxes out at $1 million. If you face two $600,000 claims, the first claim pays $500,000, the second pays $500,000 (because you still have $500,000 of your million-dollar aggregate), but you’re still $600,000 short on that second claim.

Typical monthly costs run about $45 for general liability according to real customer data, but premiums range from $250 to $3,000 annually depending on your limits and industry. Higher limits cost more but provide actual protection; umbrella insurance offers a cost-effective way to boost your coverage limits across multiple policies without duplicating basic coverage on every single policy.

How to Identify Coverage Gaps Before You Compare Quotes

Before you request quotes online, you need to know what your business actually exposes you to. A contractor working on residential properties faces different liability than a consultant working remotely. Your lease agreement, client contracts, or licensing requirements may mandate specific coverage limits that you can’t negotiate. Some industries require professional liability (errors and omissions) coverage by state law or contract, while others need it only if you want to win larger contracts. Identifying these requirements upfront saves you time when comparing quotes and prevents you from purchasing inadequate coverage. The next section walks you through the specific information you need to gather before requesting quotes online.

How to Compare General Liability Quotes Online

Organize Your Business Information First

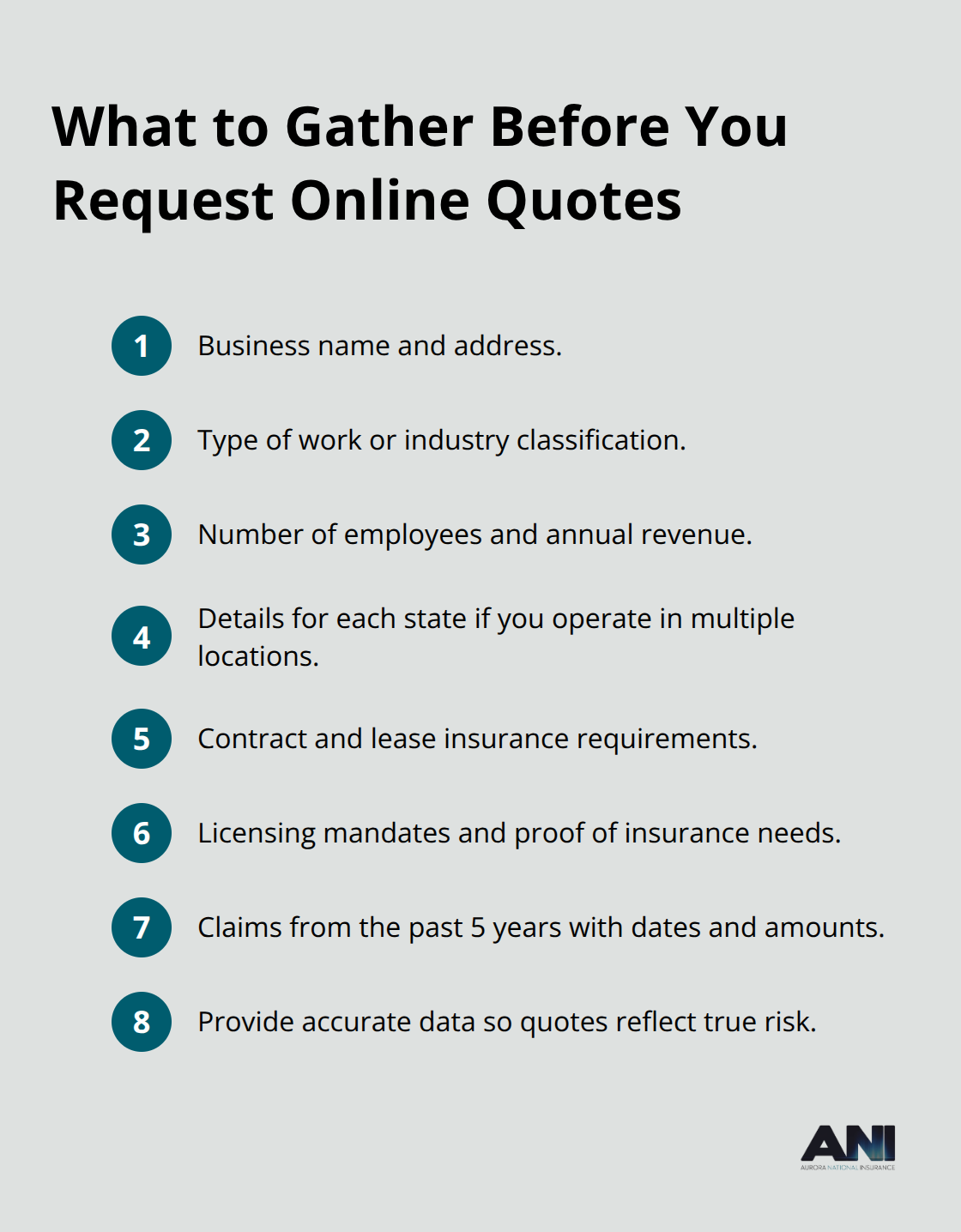

You need specific information before requesting quotes from any online platform. Collect your business name, address, type of work, number of employees, and annual revenue. Online quote platforms ask these questions upfront, and accuracy matters because incorrect information produces inaccurate quotes that won’t reflect your actual risk. If you operate in multiple states, gather details about each location since insurance availability and costs vary significantly by region due to local litigation costs and regulatory factors. Your existing contracts and lease agreements contain insurance requirements that you must document. Many commercial leases demand minimum coverage limits like $1 million in general liability, and client contracts may specify higher limits or additional coverages like professional liability. Licensing requirements also affect your coverage needs; some professions require proof of insurance before you can legally operate.

Document any claims or incidents from the past five years, including dates and settlement amounts if applicable. This information affects your premium more than most business owners realize.

Request Quotes from Multiple Carriers

When you request quotes from multiple carriers, you give them the same baseline information, which lets you compare their pricing and coverage options fairly rather than seeing quotes built on different assumptions about your business. The Hartford, Acuity, Chubb, Liberty Mutual, Travelers, and Hiscox all offer online quotes with varying specializations by industry. Most platforms allow you to submit one application and receive real-time quotes from several carriers, saving you hours of repetitive form-filling. This approach reveals how different insurers price your specific risk profile and what coverage options they emphasize for your industry.

Focus on Limits and Deductibles, Not Just Price

Ignore the monthly premium price initially and focus on three things instead. First, verify the policy limits match what you actually need based on your contracts and industry standards. Second, check the deductible amount in each quote; higher deductibles lower your monthly cost but require paying more out of pocket when a claim occurs, so calculate which trade-off makes financial sense for your cash flow. Third, examine what’s actually included in each quote. Some platforms bundle general liability with commercial property coverage in a Business Owner’s Policy at around $83 monthly, while others quote standalone general liability at approximately $45 monthly. A BOP typically costs less than purchasing general liability and property insurance separately, but you only benefit from this discount if you need both coverages.

Compare Limits Across All Your Quotes

Compare the aggregate yearly limit and per-occurrence limit because aggregate limits define how much a policy will pay over the policy’s duration. Most general liability policies have durations of 6 months or 1 year. A $1 million aggregate limit with a $500,000 per-occurrence limit means you’re covered up to $500,000 for a single incident, but your total coverage for the entire year maxes out at $1 million. Most small businesses with fewer than five employees and revenue under $200,000 qualify for standard BOP pricing, making bundled coverage worth evaluating alongside standalone general liability options. Once you’ve narrowed your options based on limits and deductibles, you’re ready to examine what specific factors drive the premium differences between carriers.

What Drives Your General Liability Premium

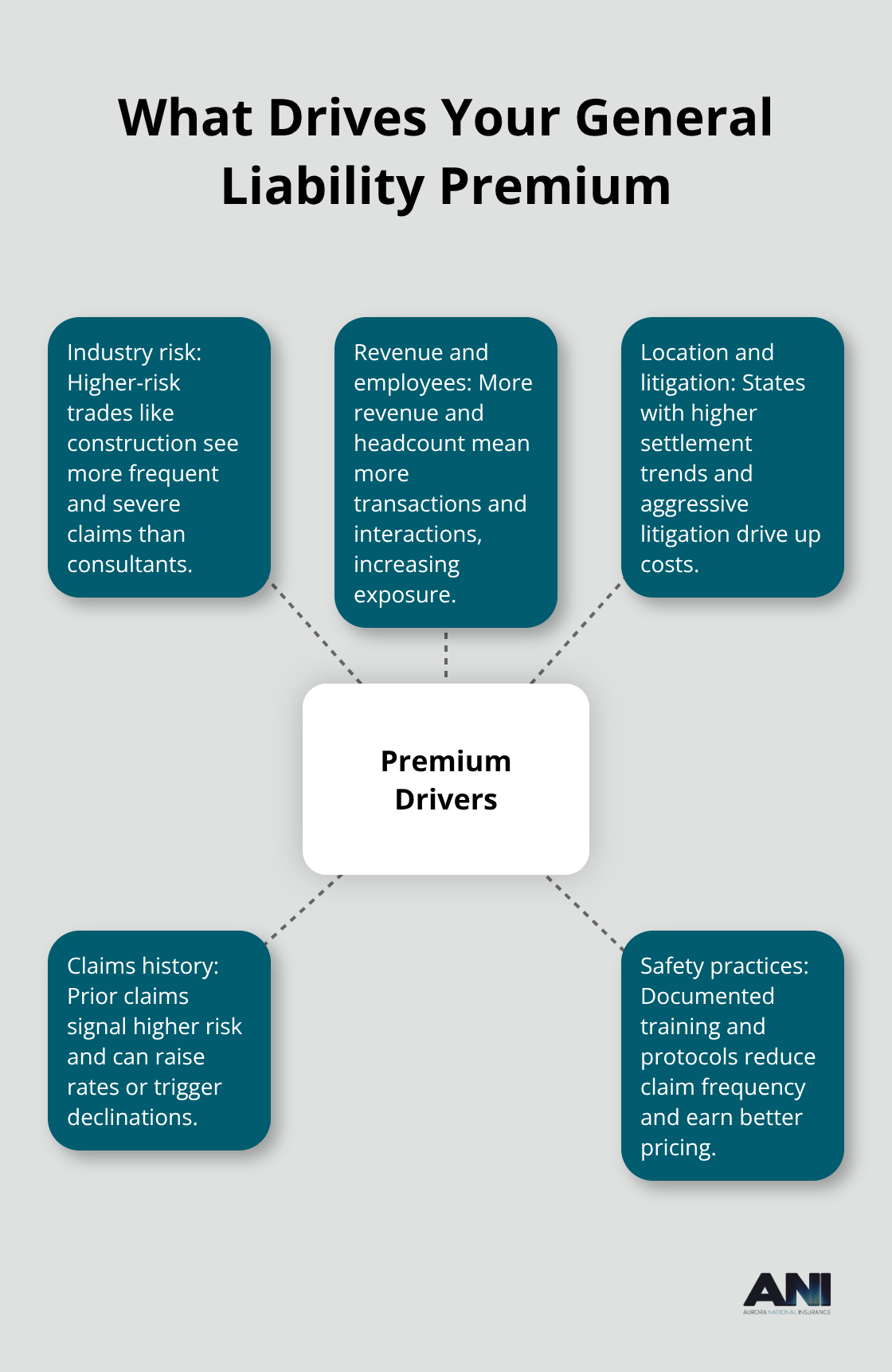

Your general liability premium isn’t arbitrary. Understanding what insurers actually measure helps you negotiate better rates or identify where you’re overpaying.

Industry risk shapes your quote first. Construction contractors pay more than consultants because job site accidents produce higher claims frequency and severity. The Hartford and Acuity specialize in construction because they’ve priced that risk accurately over decades, while IT service providers find better rates through Chubb or Hiscox because those carriers understand technology risk differently.

How Revenue and Employee Count Affect Your Cost

Your annual revenue and employee count directly correlate to premium because more employees mean more exposure to workplace injuries and customer interactions, while higher revenue suggests larger projects or more transactions where claims can occur. A one-person consulting firm generating $100,000 annually pays roughly $300 to $600 yearly for general liability, while a ten-person cleaning service with $500,000 in revenue pays $800 to $1,500 because the employee count multiplies risk exposure. Each additional employee increases your exposure to workplace injuries and customer interactions, which insurers track carefully when calculating your rate.

Location and State-Specific Litigation Costs

Location matters significantly because some states have aggressive litigation cultures that drive claim costs higher. Operating in California costs more than operating in Wyoming for identical coverage because California courts award larger settlements on average. Regional factors like local court precedents and jury tendencies influence what insurers expect to pay when claims occur in your area.

Claims History: The Factor You Control

Claims history is the factor you actually control, and it matters more than most business owners realize. A single claim from five years ago can increase your premium by 20 to 40 percent, while two claims might double your cost or get you declined entirely by certain carriers. Your track record directly influences whether insurers view you as a safe bet or a risky investment.

Safety Practices Lower Your Premium

Safety practices directly reduce claims because insurers recognize that documented safety protocols, employee training, and hazard prevention lower claim frequency. A contractor with documented daily safety briefings and equipment maintenance logs pays less than one without these practices even if both operate in the same market. Insurers reward businesses that take measurable steps to prevent accidents and injuries.

Prepare Your Information for Accurate Quotes

Before you request quotes, calculate your annual revenue accurately, count your actual employee headcount (including part-time workers), and gather documentation of any claims or incidents from the past five years with dates and settlement amounts. This information produces quotes that actually reflect your risk rather than generic estimates that you’ll need to correct later. Accurate information upfront saves time and ensures you compare quotes built on the same baseline assumptions about your business.

Final Thoughts

Comparing general liability insurance online puts you in control of your coverage decision. You now understand what to look for when reviewing quotes, how different factors affect your premium, and why policy limits matter more than the monthly price tag. Most small businesses obtain coverage within about 24 hours after submitting an application, and you can download certificates of insurance immediately after purchase when you need proof of coverage for contracts or leases.

Different insurers price your specific risk profile differently, and seeing how carriers emphasize coverage options for your industry reveals which one fits your business best. The speed of online quotes means you avoid waiting weeks for agent callbacks or spending hours on the phone explaining your business to multiple insurers. You control the timeline and make decisions based on actual data rather than pressure from a single agent.

We at Aurora National Insurance help business owners find the right coverage at competitive rates by representing multiple top-rated carriers. Our licensed agents understand local market conditions and answer questions about coverage options that generic online platforms cannot address. Get instant online quotes from Aurora National Insurance and let our team help you compare options from carriers that specialize in your industry.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.