Alaska Home Insurance Quotes: Fast Local Coverage Options

Getting Alaska home insurance quotes shouldn’t mean waiting weeks or dealing with generic national carriers that don’t understand your state’s specific risks. At Aurora National Insurance, we know that Alaska homeowners face distinct challenges-from extreme weather to remote locations and higher rebuild costs.

That’s why we’ve put together this guide to help you find fast, local coverage options tailored to your property.

Alaska’s Unique Home Insurance Challenges

Extreme Weather Patterns Drive Up Your Costs

Alaska’s extreme weather creates measurable risks that directly affect your home insurance quotes. According to Britannica, Alaska’s climate swings from summertime highs in the 90s to winter lows around minus 60 degrees. This temperature volatility causes specific damage patterns that standard homeowners policies in other states simply don’t account for.

Ice damming represents one of the most costly problems Alaska homeowners face. Ice buildup on roofs can force water under shingles and into the home, leading to damage that costs tens of thousands to repair. Winter freeze-thaw cycles also crack foundations and burst pipes-damage that occurs far more frequently in Alaska than in lower 48 states.

Wind damage from Alaska’s coastal storms and interior temperature swings damages roofs and siding at rates that push insurers to charge higher premiums to cover these predictable losses.

Remote Location Increases Replacement Costs Significantly

Alaska’s geographic isolation directly increases your replacement costs. Building materials, labor, and specialty contractors command premium prices because suppliers must ship everything north, adding weeks to delivery timelines and significant markups to invoices. When your roof needs replacement after a storm, contractors in Fairbanks or Juneau face supply-chain delays that contractors in Seattle don’t experience.

This reality means your home’s replacement cost value-the number that determines your dwelling coverage limit-must be higher in Alaska than it would be for an identical home in Oregon or Washington. Insurers factor in these higher rebuild expenses when calculating your quote. Alaska’s limited contractor availability in smaller communities means repair costs climb when demand spikes after widespread storms.

The Alaska Earthquake Center reports that earthquakes occur roughly every 15 minutes in Alaska, with historical magnitude 9.2 events like the 1964 Good Friday quake reshaping entire regions. While standard homeowners policies cover wind and storm damage, earthquake coverage isn’t included and must be added separately-another cost consideration for properties in seismically active areas.

Wildfire and Flood Risks Require Separate Coverage

Wildfires have grown more frequent across Alaska as climate patterns shift. NASA Earth Observatory data shows that rising temperatures extend fire seasons and increase wildfire risk across the state, yet standard homeowners policies treat wildfire damage inconsistently. Some carriers exclude it entirely; others cover it under the dwelling section. Your quote will reflect whether your property sits in a wildfire-prone zone, and homes in high-risk areas face steeper premiums or coverage restrictions.

Flood risk compounds this challenge because Alaska’s geography includes coastal properties, riverside homes, and areas vulnerable to glacial melt and ice-jam flooding. The National Flood Insurance Program and private flood insurance are not included in standard homeowners policies, meaning you must purchase flood coverage separately if you live in or near a flood zone. This adds another line item to your total insurance cost that homeowners in Arizona or Texas typically don’t face.

Understanding these unique insurance challenges helps you know exactly what coverage gaps exist in a standard policy-and that’s where the right quote comparison becomes essential.

How to Get Fast Home Insurance Quotes in Alaska

Online Quote Tools Deliver Instant Estimates

The fastest way to compare Alaska home insurance quotes starts online, where most carriers now offer instant estimates within minutes. Major insurers like State Farm, Allstate, and USAA provide quote tools that let you enter your home’s details and receive price comparisons without waiting for a callback. You control the pace and can compare multiple carriers in a single session.

Online quotes in Alaska often miss important local variables that affect your actual premium. A quote for an Anchorage home might differ significantly from a quote for a Fairbanks property, even if the homes are identical, because insurers weight climate risk, contractor availability, and supply-chain costs differently by region. When you use online tools, have your home’s year built, square footage, roof material, and dwelling coverage amount ready. The more accurate your information, the closer your quote will be to your actual premium.

One limitation stands out: online tools rarely account for Alaska-specific coverage gaps like flood or earthquake protection. You’ll need to manually add these endorsements and recalculate to see your true cost.

Local Agents Identify Coverage Gaps Online Tools Miss

Working with a local Alaska agent offers something online quotes cannot: someone who understands why your ice dam risk in Fairbanks differs from coastal storm risk in Juneau, and how to position your coverage accordingly. An agent identifies coverage gaps that generic online quotes miss entirely, such as whether your home qualifies for lower rates based on roof upgrades or whether you’re underinsured for wildfire risk.

An agent also handles the back-and-forth with carriers when you need clarification on what’s covered, saving you hours of frustration. The trade-off is speed: a phone consultation takes longer than an online quote, but the result is far more precise. Local agents know exactly which carriers price competitively in different Alaska regions and which ones restrict coverage in high-risk zones.

Prepare Your Home Information in Advance

Before contacting an agent or submitting an online quote, gather your home’s year of construction, square footage, roof type, number of stories, any recent renovations, prior insurance claims, and your desired deductible. Having this information ready cuts quote time significantly and prevents the frustration of starting a quote, realizing you’re missing information, and having to restart.

If your home has high-value items like jewelry or art, mention those upfront so the agent can explain how scheduling or endorsements affect your quote and premium. This preparation step transforms the quoting process from a time-consuming back-and-forth into a streamlined conversation that produces accurate, actionable quotes.

With your quotes in hand and your home information organized, the next step involves understanding which coverage options actually protect your Alaska property against the specific risks you face.

Finding the Right Coverage for Your Alaska Home

Standard Homeowners Policy Components

A standard homeowners policy in Alaska covers six essential areas: dwelling, other structures, personal property, loss of use, personal liability, and medical payments to others. Your dwelling coverage pays to rebuild your home after a covered loss, and this number matters more in Alaska than anywhere else because replacement costs run significantly higher due to supply-chain expenses and contractor scarcity. If your home would cost $400,000 to rebuild and you only insure it for $300,000, you’ll absorb tens of thousands in losses when a major fire or storm hits.

Other structures coverage typically equals 10 percent of your dwelling limit, which works fine if you have a small shed but falls short if you own a detached garage or multiple outbuildings. Personal property coverage usually sits at 50 percent of dwelling coverage, meaning a $300,000 dwelling policy provides only $150,000 for your furniture, electronics, and clothing. That gap matters when you lose everything in a house fire.

Loss of use coverage pays for temporary housing if your home becomes uninhabitable after a covered loss, typically covering 20 percent of your dwelling limit. Personal liability protection starts at $100,000 on most policies, which protects you if someone is injured on your property and sues, though Alaska homeowners with significant assets should seriously consider raising this to $300,000 or $500,000.

Additional Coverage Options for Alaska Properties

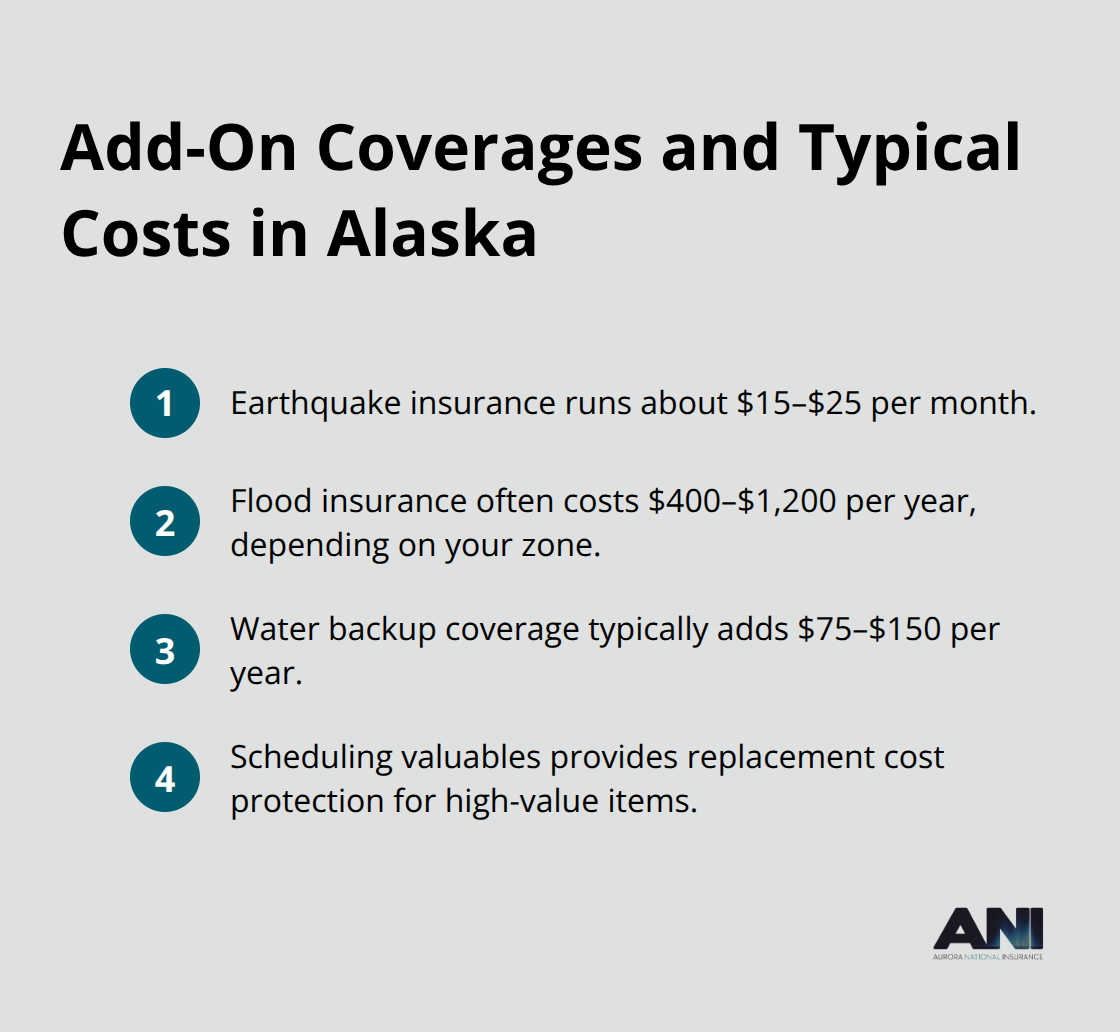

Alaska’s specific risks demand additional coverage that standard policies exclude entirely. Earthquake insurance costs roughly $15 to $25 per month but becomes essential given that the Alaska Earthquake Center documents earthquakes annually, including the magnitude 9.2 Good Friday quake of 1964. Flood insurance through the National Flood Insurance Program or private carriers costs between $400 and $1,200 annually depending on your flood zone, yet standard policies provide zero flood coverage.

Water backup coverage protects you when sump pumps fail or sewage backs up during heavy storms, typically adding $75 to $150 annually. If you own valuables like jewelry, cameras, or art, scheduling these items with appraisals provides replacement cost protection rather than the depreciated actual cash value most standard policies pay.

Comparing Quotes from Multiple Carriers

Comparing quotes from at least three carriers reveals dramatic price differences across Alaska. COUNTRY Financial averages $942 annually for $300,000 of dwelling coverage, while State Farm runs roughly $1,021 and Allstate approaches $1,525 for identical coverage in the same location. Rates shift dramatically by city: Anchorage averages $758 annually, Juneau $655, and Wasilla $708, yet Eagle reaches $1,538 for the same coverage amount.

When you receive quotes, verify that each one includes the same deductible, dwelling limit, and coverage options, because comparing a $500 deductible quote against a $1,000 deductible quote produces meaningless results. Bundling home and auto insurance typically saves 10 to 15 percent on your total premium, making it worth shopping both policies together rather than separately.

Final Thoughts

Alaska home insurance quotes reveal one consistent truth: your coverage needs differ fundamentally from homeowners in the lower 48 states. The extreme weather, remote location, higher replacement costs, and unique natural disaster risks demand a thoughtful approach to selecting both your coverage limits and your insurance partner. A $942 annual premium from one carrier versus $1,525 from another for identical coverage represents real money, yet the cheapest quote isn’t always the best choice if it leaves gaps in earthquake or flood protection.

Online quotes give you speed and broad price comparisons, while local agents provide the expertise to identify coverage gaps that generic quotes miss entirely. The most effective approach combines both: use online tools to establish baseline pricing, then consult with a local agent who understands Alaska’s specific risks and can explain why your Fairbanks home needs different protection than an identical home in Anchorage. We at Aurora National Insurance represent multiple top-rated carriers and combine instant online quotes with licensed agents who understand the real risks Alaska homeowners face.

Start by gathering your home information and requesting Alaska home insurance quotes from at least three carriers. Then contact a local agent to review those quotes and identify any coverage gaps. This two-step process takes a few hours but protects your home and your finances for years to come, and our team can help you navigate the options at competitive prices.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.